|

|

Home

| Databases

| WorldLII

| Search

| Feedback

Precedent (Australian Lawyers Alliance) |

THE MORTGAGE DEBT TIMEBOMB

By Josh Mennen

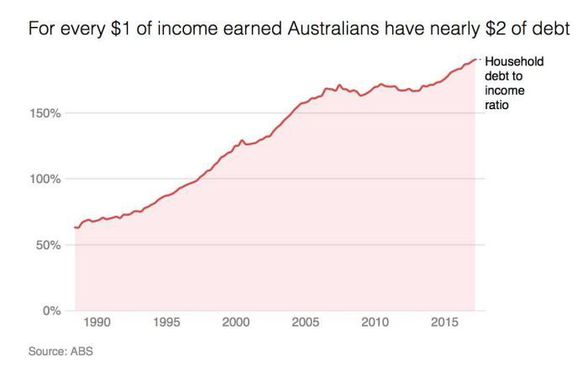

A decade of soaring property growth, generous tax incentives for property investors and record low interest rates has resulted in Australian households being among the most indebted in the world.

A recent Australian Bureau of Statistics (ABS) report into household debt found that in 2015-16, 29 per cent of households were classified as ‘over-indebted’, defined as having debt three times or more than disposable income, or debt equal to 75 or more of the value of their assets. The average home loans for over-indebted households were over four times the size of home loans held by other households carrying debt ($286,400 compared with $59,500).[1]

Many property investors have successfully managed their repayment obligations while riding the property wave. But the wave is due to crash soon, and it’s not going to be pretty.

Property growth can no longer be presumed, with the formerly surging Sydney market beginning to plateau and even dip, while interest rates can only increase. Many would-be real estate entrepreneurs are starting to feel the strain of so much debt, and distress sales are on the rise.[2]

A combination of banks’ relaxed lending standards and brokers’ involvement in loan sales has resulted in widespread debt over-commitment that threatens the stability of the broader economy: a survey of more than 900 home loans conducted by investment bank UBS[3] found that around $500 billion worth of outstanding home loans are based on incorrect statements about incomes, assets, existing debts and/or expenses. This means that 18 per cent of all outstanding Australian credit is based on inaccurate information, often caused by poor advice or misrepresentations by a mortgage broker eager to generate a sale commission. A staggering 30 per cent of loans surveyed had been issued based on understated living costs and around 15 per cent on other, understated debts or overstated income.

Until recently, this problem had been contained, as investors who defaulted on their mortgages were often fortunate enough to sell the investment property at a gain or at least break even, clearing the mortgage without too much pain.

However, if interest rates rise by 1 per cent, more than 40 per cent of homes would be in mortgage stress (for context, a 4 per cent increase above current rates would bring interest rates roughly in line with the average over the past two decades).[4] This will further drive up distress sales in a stagnant or contracting market and may leave thousands of property investors in financial ruin, staring at the prospect of bankruptcy.

INTEREST-ONLY LOANS

If that analysis wasn’t sobering enough, add to the equation the fact that a huge proportion of mortgage loans issued over the past decade were ‘interest-only loans’. These loans have an initial period (usually five years) where only the interest on the loan is repaid. However, after the interest-only period ends and the principal is also paid down, the loan repayments can increase between 30 and 60 per cent.

A review of home loans with an interest-only period conducted by the Australian Securities and Investments Commission (ASIC)[5] found that:

• in the March 2015 quarter, interest-only home lending had increased almost 20 per cent from the previous year, and made up around 42 per cent of all new home loans issued in that quarter;

• the average value of interest-only home loan amounts is substantially higher than that of principal-and-interest home loans for both owner-occupiers and investors. That’s because of the lower initial repayment figure under this type of loan and the effect of ‘present bias’ (where people focus on present costs and features over future costs and features); and

• mortgage brokers may be incentivised to recommend an interest-only home loan, as the principal will not initially be paid down and the trail commission will be paid for a number of years on a higher balance.

It has also been reported that up to one-third of borrowers with interest-only loans may not realise they have them.[6]

LEGAL PROTECTIONS

In addition to any common law claims in contract and tort, consumers who slide into unmanageable mortgage debt may have a cause of action against their lender or broker under the National Consumer Credit Protection Act 2009 (Cth) (NCCP Act) incorporating the National Credit Code (NCC). These federal statutory protections were put in place following the Global Financial Crisis, and sit beside the Australian Consumer Law (ACL) to make up the central consumer protection legislation applying to credit.

Although this statutory regime appears to have been unsuccessful in deterring imprudent lending practices, it will no doubt have much work to do as economic conditions turn and over-committed borrowers’ losses crystallise.

The NCCP Act and NCC apply only to ‘consumer’ credit, which includes loans taken for property investment.[7] They do not cover business loans.[8] Business loans may be covered by the Code of Banking Practice (if the lender subscribes), common law or possibly the ACL.

NCCP Act – Responsible Lending

Section 128 of the NCCP Act provides that a lender must not enter into a credit contract with a consumer, unless it has, within 90 days of entering into the contract:

• made an assessment as to whether the contract will be unsuitable for the consumer;[9]

• made reasonable inquiries about the consumer’s requirements and objectives in relation to the credit contract;[10]

• made reasonable inquiries about the consumer’s financial situation;[11]

• taken reasonable steps to verify the consumer’s financial situation;[12]

• made any inquiries prescribed by the regulations including making reasonable inquiries about the maximum credit limit that a consumer requires;[13] and

• taken any steps prescribed by the regulations to verify any matter prescribed by the regulations.

Section 131 provides that the licensee ‘must assess’ the credit contract as unsuitable for the consumer if, at the time of assessment, it is likely that:

• the consumer will be unable to comply with their financial obligations under the contract or could comply with those obligations only with substantial hardship; or

• the contract will not meet the consumer’s requirements or objectives.[14]

Pursuant to s131(3), it is presumed that the consumer will be under substantial hardship if they can only comply with their financial obligations under the contract by selling their principal place of residence, unless the contrary is proved.

Section 131(4) sets out the only information to be taken into account for the purposes of s131(2) which includes (a) the information about the consumer’s financial situation, requirements or obligations and (b) the information the licensee had reason to believe was true or would have had reason to believe was true if the licensee had made the inquiries or sought verification under s130.[15]

Consumers are entitled to copies of the assessment before and after entering into the credit contract.[16]

A lender is prohibited from entering into an unsuitable contract with a consumer.[17] Section 132(2) confirms that a credit contract will be unsuitable on the same bases as s131, and in determining whether the credit contract is unsuitable under s133(2), the only information to be taken into account is the same as under s131(2).[18] Section 133(3) contains the same presumption as s131(3).

The so far scarce case law suggests that perfunctory inquiries are likely to be insufficient, and that further inquiries might be needed if the consumer provided inconsistent or contradictory information.[19]

In ASIC v The Cash Store,[20] Davies J explained that the obligations under s128 of the NCCP Act required ‘a sufficient understanding of the person’s income and expenditure’, and that this required, at a minimum, inquiries about the consumers’ income and living expenses which is likely to include reference to rent/mortgage payments, and grocery, utility and other expenses, and other debt.[21]

In ASIC v Australia and New Zealand Banking Group,[22] ANZ admitted contraventions of the NCCP Act by failing to take reasonable steps to verify the consumer’s financial situation.[23] This included reasons it had to doubt the reliability of information received from the brokers who procured the loans.

ASIC has taken the view that the obligations to make inquiries and take steps to verify information are scalable obligations; that is, what a lender needs to do to meet the obligations in relation to a particular consumer will vary depending on a variety of circumstances, such as whether the customer is a new or existing customer and the potential impact on the consumer of an unsuitable contract.[24]

The fact that a mortgage broker has made a preliminary assessment in relation to a consumer does not relieve the lender of its obligation to make its own assessment. This position has been confirmed in two recent cases where the lender’s reliance on the broker’s assessment was not sufficient, confirming lenders’ direct responsibilities to assess customers’ suitability themselves.[25]

ASIC’s Regulatory Guide for credit licensees suggests that an assessment of whether the proposed credit contract could cause substantial hardship to the consumer should take into account:

• what surplus the consumer has after covering their ongoing expenses and the payments required under the new contract;

• the source of the consumer’s income, and the consistency and reliability of that income;

• whether the consumer’s expenses are higher than average;

• the consumer’s other debt repayment and other financial commitments; and

• whether an asset will be needed to be sold to make the repayments.[26]

NCCP Act remedies

Sections 128, 130, 131, 132 and 133 of the NCCP Act are civil penalty provisions.[27]

Pursuant to s178, the court may order the defendant to compensate the plaintiff for loss or damages suffered by the plaintiff if:

• the defendant has contravened a civil penalty provision or committed an offence against the NCCP Act (other than the Consumer Credit Code); and

• the loss or damage resulted from the contravention or commission of the offence.

The court may only make an order for compensation pursuant to s178 if the plaintiff applies within six years of the day the cause of action that relates to the contravention or commission of the offence accrued. This may, in effect, mean that by the time a potential plaintiff is struggling financially, aware of the losses he/she has suffered, or realised that they were the victim of poor lending practices, the timeframe for commencing court proceedings will already have expired. This anomaly has the potential to thwart consumers’ access to justice, particularly those who were sold interest-only loans which tip them into hardship years only after the contract is entered into.

NCC – Unjust lending

Section 76 of the NCC contains a power for courts to ‘reopen’ an unjust credit transaction. This provision is modelled on the Contracts Review Act 1980 (NSW).

The NCC does not define ‘unjust’ but states that the court must have regard to ‘the public interest and to all the circumstances of the case’.[28] Matters that may be relevant are broadly defined, but include considerations consistent with assessing unconscionable conduct under the ASIC Act 2001 (Cth), including the consequences of non-compliance with the contract, the relative bargaining positions of the parties including any vulnerability of the consumer and whether unfair tactics or pressure was used.

As with the prohibition on unconscionable conduct in the ACL, courts have declined to provide a narrow or precise definition of what amounts to an unjust transaction, preferring a case-by-case approach that focuses on the words of the section. In most cases, contracts have been set aside on the basis of a combination of concerns about the process by which the contract was made and the substantive unfairness of the terms.[29]

Where a court reopens a transaction as unjust, it may make a range of orders giving relief to the consumer affected, including setting aside or revising the underlying contract.[30]

The time limit in an unjust contract application to court is two years from when the contract ends.[31]

EXPENSE BENCHMARKING TOOLS

On 1 March 2017, ASIC commenced Federal Court proceedings against Westpac Banking Corporation (Westpac) alleging contraventions of the NCCP Act by Westpac’s alleged failure to properly assess whether consumers could meet their repayments before entering into home loan contracts between December 2011 and March 2015.[32] Specifically, ASIC alleges that Westpac:

• used a benchmark tool instead of the actual expenses declared by consumers in assessing their ability to repay the loan;

• approved loans where a proper assessment of a consumer's ability to repay the loan would have shown a monthly deficit; and

• for home loans with an interest-only period, Westpac failed to have regard to the higher repayments at the end of the interest-only period when assessing a consumer’s ability to repay.

In what will likely be a bellwether case in respect to the appropriateness of benchmarking tools – which are widely used by lenders to determine a consumer’s living expenses – ASIC is asking the court to declare that Westpac breached the NCCP Act and is therefore seeking that a pecuniary penalty be imposed on it.

THE BANKRUPTCY PARADOX

In circumstances where a consumer becomes bankrupt due to debt over-commitment, their cause of action against their lender including under the NCCP Act will vest in their trustee in bankruptcy pursuant to s116 of the Bankruptcy Act 1966 (Cth). This is the case even in circumstances where the defendant in any such action is listed as a creditor. This places the trustee in an invidious situation, as it has an obligation to administer the estate in the interests of the creditors, as well as the bankrupt.[33]

This means that the irresponsible lender may have an interest in the cause of action against itself which it may use to influence the determinations of the trustee in bankruptcy, including whether the cause of action should be pursued or assigned.

For this reason it’s important that consumers do all they can to mitigate their losses early to try to avoid bankruptcy and retain their ability to exercise their legal rights.

THE ROYAL COMMISSION INTO MISCONDUCT IN THE BANKING, SUPERANNUATION AND FINANCIAL SERVICES INDUSTRY

At the time of writing this article, Commissioner Hayne QC is hearing evidence regarding the extent of lending misconduct. His mandate is to decide whether changes to the legal framework are necessary to minimise the likelihood of misconduct by lenders and brokers in future.

The lenders’ approach has been predictable – a gloss of mea culpa for past mistakes, often blaming ‘rogues’ or ‘bad apples’, while denying any ongoing systemic problem or culpability at senior management level.

But the Commissioner is digging deeper: After just two days of substantive hearings, the big banks have admitted to refunding almost $250 million to about 540,000 home loan customers since July 2010, including in cases of fraudulent documentation and breaches of responsible lending laws.[34]

The National Australia Bank (NAB) has also admitted that white envelopes stuffed with money were passed across tellers’ counters to bribe bankers into giving out fraudulent home loans in connection with its ‘introducer scheme’ which generated $24 billion in NAB home loans between 2013 and 2016.[35]

At this rate, there is no telling how deep this rabbit hole will go, or how bad the fallout will be when (not if) the current market conditions deteriorate.

Josh Mennen is a Principal Lawyer at Maurice Blackburn, Sydney. He specialises in financial services disputes including superannuation and insurance claims, financial advice and responsible lending disputes. He has acted for hundreds of victims of negligent financial planning and stockbroking advice. PHONE (02) 8267 0977 EMAIL JMennen@mauriceblackburn.com.au.

[1] Australian Bureau of Statistics, Household debt and over-indebtedness in Australia (October 2017) <http://www.abs.gov.au/ausstats/abs@.nsf/Lookup/by%20Subject/6523.0~2015-16~Feature%20Article~Household%20Debt%20and%20Over-indebtedness%20(Feature%20Article)~101> .

[2] D Hughes, ‘Record numbers under mortgage stress’, Financial Review (online), 1 May 2017, <http://www.afr.com/personal-finance/record-numbers-under-mortgage-stress-20170501-gvw2vt> .

[3] J Mott, R Bentvelzen and G Tharenou, ‘Australian Banking Sector Update, UBS Evidence Lab – $500 billion in “Liar Loans”?’ UBS, September 2017, <https://webcache.googleusercontent.com/search?q=cache:PhkZ9vGUMU0J:https://thejollyswagmen.com/s/UBS-LIAR-LOANS.pdf+&cd=9&hl=en&ct=clnk&gl=au>.

[4] I Ting, R Liu and N Scott, ‘Mortgage stress hotspots revealed’, ABC News (online), 21 August 2017, <http://www.abc.net.au/news/2017-08-21/how-interest-rate-rises-could-affect-home-loan-stress/8798274> .

[5] ASIC Report 445 – Review of interest-only home loans (August 2015).

[6] M Janda, ‘Interest-only home loans a ticking time-bomb, warns UBS’, ABC News (online), 4 October 2017, <http://www.abc.net.au/news/2017-10-04/consumers-unaware-they-have-interest-only-home-loans/9014448> .

[7] National Credit Code, ss5(1), (3) (NCC).

[8] Ibid, s5(1).

[9] National Consumer Credit Protection Act 2009 (Cth), s129 (NCCP Act).

[10] Ibid, s130(1)(a).

[11] Ibid, s130(1)(b).

[12] Ibid, s130(1)(c).

[13] Ibid, s130(1)(d) and National Consumer Credit Protection Regulations 2010.

[14] Ibid, s131(2).

[15] Ibid, s131(4).

[16] Ibid, s132.

[17] Ibid, s133(1).

[18] Ibid, s133(4).

[19] Australian Securities and Investments Commission v The Cash Store Pty Ltd (in liquidation) [2014] FCA 926 [28] (‘ASIC v The Cash Store’); see also N J Howell, ‘Small amount credit contracts and payday loans: The complementarity of price regulation and responsible lending regulation’, Alternative Law Journal 174, Vol. 41(3), 2016, 177. See also ASIC reg 209.51.

[21] ASIC v The Cash Store [2014] FCA 926 [43] and [52]; see also Commonwealth, Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry, Background Paper 4: Everyday Consumer Credit Overview of Australian Law Regulating Consumer Home Loans, Credit Cards and Car Loans (March 2018) (‘Royal Commission Background Paper’).

[23] ASIC v ANZ [2018] FCA 155, [32].

[24] Factors that, in ASIC’s view, will impact on the scope of the obligations in any particular instance are contained in ASIC reg 209 Credit licensing: responsible lending conduct (2014) [19].

[25] ASIC v The Cash Store [2014] FCA 926 [68]; see also Australian Securities and Investments Commission v Channic Pty Ltd (No. 4) [2016] FCA 1174 [1804]; see also above note 21, Royal Commission Background Paper.

[26] ASIC Regulatory Guide 209, Credit licensing: responsible lending conduct (2014), [99].

[27] NCCP Act, s5.

[28] NCC, s76(2).

[29] See above note 21, Royal Commission Background Paper, citing Permanent Mortgages Pty Ltd v Cook [2006] NSWSC 1104; [2006] ASC 155-082. Also J M Paterson, ‘Unconscionable Bargains in Equity and Under Statute’, Journal of Equity, Vol. 9, 188-213.

[30] NCC, s77.

[31] Ibid, s80.

[32] ASIC, ‘ASIC commences civil penalty proceedings against Westpac for breaching home-loan responsible lending laws’ (Media Release, 1 March 2017) <http://asic.gov.au/about-asic/media-centre/find-a-media-release/2017-releases/17-048mr-asic-commences-civil-penalty-proceedings-against-westpac-for-breaching-home-loan-responsible-lending-laws/> .

[33] Doolan v Dare [2004] FCA 682 (27 May 2004).

[34] ‘Banking royal commission: banks refund nearly half a billion’, The Australian Business Review (online), 14 March 2018, <https://www.theaustralian.com.au/business/banking-royal-commission/banking-royal-commission-banks-refund-nearly-half-a-billion/news-story/43fd1478ca1234e608e227e08422e733>.

[35] B Butler, ‘Envelopes “stuffed with cash” to bribe tellers for home loans’, The Australian Business Review (online), 13 March 2018, <https://www.theaustralian.com.au/business/banking-royal-commission/envelopes-stuffed-with-cash-to-bribe-tellers-for-home-loans/news-story/c8486901a2616ec678d3d130afb4d362>.

AustLII:

Copyright Policy

|

Disclaimers

|

Privacy Policy

|

Feedback

URL: http://www.austlii.edu.au/au/journals/PrecedentAULA/2018/32.html