University of Western Sydney Law Review

|

|

Home

| Databases

| WorldLII

| Search

| Feedback

University of Western Sydney Law Review |

|

MARINA NEHME*

A ‘court-enforceable undertaking’ is a sanction available to an increasing number of Australian regulators. In 1993, after the enactment of s 87B into the Trade Practices Act 1974 (Cth), the Australian Competition and Consumer Commission (‘the ACCC’) became the first regulator to have and use such a sanction. Due to the apparent success of the use of enforceable undertakings by the ACCC[1], other regulators at both federal and state levels have lobbied successfully for the introduction of the sanction into their own regulatory systems.[2]

Similar provisions to s 87B were first enacted into the Australian Securities and Investments Commission Act 2001 (Cth) (‘the ASIC Act’). Sections 93A and 93AA of the ASIC Act gave the Australian Securities and Investments Commission (‘ASIC’) the power to accept enforceable undertakings. The provisions of s 87B of the Trade Practices Act and of ss 93A and 93AA of the ASIC Act are drafted in very similar terms.

An enforceable undertaking can be described as a promise enforceable in court.[3] It takes the form of a settlement in which the alleged offender (who may be called ‘the promisor’) and the regulator, ASIC, start its negotiation in relation to the alleged breach. The statute[4] allows the regulator wide latitude to negotiate and accept outcomes similar to those remedies available to the Court in many respects, and also remedies not normally within the Court’s power, as long as the undertaking is accepted ‘in connection with a matter in relation to which’ the regulator has a power or function.[5] Further, the statute may allow the Court to make orders to enforce an undertaking that would ordinarily not be within its power to make.[6]

This article is divided into four parts. The first part considers the origins of the sanction of enforceable undertakings. The second part observes ASIC’s policy in relation to enforceable undertakings and the circumstances under which enforceable undertakings are accepted. The third part examines the promises given in an enforceable undertaking. The last part takes into account ASIC’s strategy in relation to the enforcement of enforceable undertakings.

ASIC was given the power to accept enforceable undertakings in July 1998 by the Financial Sector Reform (Amendments and Transitional Provisions) Act 1998 (Cth).[7] Item 11 of this Act allowed ASIC to accept a written undertaking, which may be enforced by a court where the court finds that the undertaking has been breached. The Explanatory Memorandum noted that, under s 93A, ASIC will be given the power to accept a written undertaking without first having to go to court.[8] As a consequence of the passage of the Financial Sector Reform (Amendments and Transitional Provisions) Bill 1998 (Cth), the provisions related to enforceable undertakings are today contained in ss 93AA (generally) and 93A (in relation to registered managed investment schemes) of the ASIC Act.[9] With some minor variations, these two sections are similar in content to s 87B of the Trade Practices Act. Such a similarity between the provisions of enforceable undertaking in the ASIC Act and the Trade Practices Act is understandable since it is because of the apparent successful use of enforceable undertaking by the ACCC that ASIC was given this power. The ACCC after all was the first regulator that had such a sanction at its disposal.

The enforceable undertaking’s provisions were introduced in the Trade Practices Act in 1993. Prior to this date, it was quite common for the ACCC to decide not to take tough enforcement action against possible regulatory breaches, on the basis that it could achieve acceptable compliance with potential offenders through administrative resolution. Administrative resolutions are basically the equivalent of a settlement. They may include accepting assurances from the alleged offender to stop the conduct or otherwise modify their commercial practices to ensure compliance with the law. However, such resolutions lacked formal legal enforceability and it was doubtful whether they were legally enforceable.

As a result, the Griffith and Cooney Committees recommended that the ACCC should be given statutory powers to accept undertakings which are legally enforceable. Accordingly, the enforceable undertaking provisions were introduced to the system to legitimate and formalize the negotiated agreements entered into between the ACCC and alleged offenders.[10]

The then chairman of the ACCC, Alan Fels, strongly supported the provision as a regulatory tool stating that ‘legally enforceable undertakings … (have) made the Act both more effective and helped avoid court procedures’.[11] The ACCC’s power to accept an enforceable undertaking appears broadly defined. Section 87B(1) of the Trade Practices Act states:

The Commission may accept a written undertaking given by a person for the purposes of this section in connection with a matter in relation to which the Commission has a power or function under this Act (other than Part X).

As shown in Diagram 1, s 87B constitutes a form of intermediate sanction. It provides a more formal and more powerful deterrent than simple administrative resolution in seeking compliance, but avoids the legal and financial severity and the publicity associated with protracted litigation.[12]

Administrative resolution

Enforceable undertaking

Litigation

Diagram 1: From a lesser sanction to a harsher one

Accordingly, enforceable undertakings can be viewed today as a new form of alternative dispute resolution. This sanction will allow regulators to solve alleged breaches of the law without remedying to court action. However, the statutes also give the undertaking an edge over other form of settlement because it allows the regulatory agency to enforce the undertaking in court in case of non-compliance with terms of the undertaking.

Practice Note 69 (‘PN 69’) sets out ASIC’s views on the policy, interpretation and operation of ss 93A and 93AA of the ASIC Act. However, in March 2007, PN 69 was replaced by a new guideline, Enforceable Undertakings: an ASIC Guide. The new guideline takes into consideration PN 69 and builds on it by responding to the questions and problems that were raised when dealing with entering into undertakings in the past. The guide is divided into four sections. Section 1 covers what is an undertaking. Section 2 explains the circumstance under which ASIC will accept an undertaking. Section 3 notes the acceptable and unacceptable terminology in the enforceable undertakings. Section 4 explains what happens if an undertaking is breached.

Enforceable undertakings are commonly used by companies and individuals as a way to avoid unnecessary litigation. However, certain commentators expressed concerns that the use of enforceable undertakings may lead to the decriminalisation of serious offences.[13] Such concern is not justified. It is true that an enforceable undertaking is an administrative sanction and its use may open the way for the corporate regulator to move from criminality to softer sanctions. But an enforceable undertaking is one of a number of sanctions available to ASIC and it is up to the corporate regulator to decide which remedy should be used by applying, for example, Braithwaite’s pyramid of enforcement.

A. The Pyramid of enforcement

Strategic regulation theory advocates that regulators have available and employ a mix of enforcement strategies and sanctions. Having a number of sanctions available allows the regulator to react in a manner proportionate to the committed offence. Compliance is most likely when all an agency’s enforcement tools are used in an appropriate and commensurate way. The width of the enforcement pyramid ideally represents the quantum of actions taken (or the proportion of the regulated entities who will comply) using the different tools. Braithwaite and Ayres describe such a pyramid in their book, Responsive Regulation: Transcending the Deregulatory Debate.[14]

As depicted in Diagram 2, the base of the pyramid represents the attempts to coax compliance by persuasion, education, self and co-regulatory strategies, and the warning that actions might be taken if the violation continues. Moving up the pyramid, the next stage of enforcement is the acceptance by the regulator of administrative resolutions, then an enforceable undertaking. If this fails to secure compliance, civil penalties will come into play followed by criminal prosecution. If these methods do not work to secure compliance, the regulator might suspend temporarily the offender’s license to operate. If all fails, permanent revocation of the license is the last step taken by the agency. This escalation of sanctions is sketched in the form of a pyramid.[15]

.

Criminal penalty

Civil penalty

Enforceable undertaking

Persuasion/warning letter/education …

License suspension

License revocation

Diagram 2: Enforcement pyramid[16]

In summary, the basic idea of responsive regulation is that governments should respond to the conduct of those they seek to regulate in deciding whether a more or less interventionist approach is needed, and ensure the regulators have an appropriate range of sanctions at their disposal. Regulators should operate on the basis that it is better to start with dialogue and then employ sanctions higher up the pyramid as the conduct goes up in severity. Furthermore, an application of the pyramid allows the regulator to use its full arsenal in appropriate cases.

B. ASIC and the enforcement pyramid

ASIC seem to be applying this pyramid of enforcement when deciding on the sanction it is going to use when faced with a breach of the law. The corporate regulator is aware of the danger of heavily relying on enforceable undertakings because a heavy reliance on this sanction (if it is not accompanied by the use of the regulator’s other sanctions) may lead to creation of a perception that the corporate regulator is soft and unwilling to use all arsenal that are at its disposal. This is also confirmed in ASIC’s annual reports. Annual Report 2000-2001 notes that enforceable undertakings were used to target lesser alleged breaches.[17] ASIC’s Annual Report 2001-2002 states that criminal prosecution remains a central and successful weapon, alongside civil action to reduce damage to investors and consumers.[18] ASIC’s annual reports also attest that the number of criminal actions taken against corporate offender has not diminished over the years.

Furthermore, ASIC is clear about the policy it uses when dealing with enforceable undertakings. The regulator will not enter into an undertaking that does not offer a more effective regulatory outcome than other penalties.[19] For example, in the enforceable undertaking entered into with Multiplex Ltd, ASIC stated that:

In considering whether to accept this enforceable undertaking ASIC has taken into account that the undertaking would provide a more appropriate regulatory outcome than a civil penalty proceeding. [20]

It is also important to note that on certain occasion ASIC does not just accept an enforceable undertaking. An enforceable undertaking may be the result of court actions that ASIC has started in the past. In ASC v Nomura International Plc (includes summary) [1998] 1570 FCA, the Federal Court made declarations that Nomura, in closing out its arbitrage position on 29 March 1996, had contravened ss 995, 998 and 1260 of the Corporations Law and s 52 of the Trade Practices Act 1974 (Cth). This judgment was followed by an acceptance of an enforceable undertaking. In the undertaking, Nomura promised ASIC not to engage in the contravening action in the future. The undertaking was in no way contradictory to the judgment.[21] Such undertakings may be very beneficial because an enforceable undertaking can include promises that may not be ordered by the court and accordingly may deal with areas that the court did not cover.[22] Accordingly, when the regulator accepts an enforceable undertaking, it is not showing its weakness. On the contrary, it illustrates the fact that it is using its full arsenal by applying the pyramid of enforcement. If a breach may be remedied effectively through an enforceable undertaking, then the regulator will decide on this sanction. If this is not the case, then ASIC may use other remedies that are at its disposal.

C. Criteria considered when accepting an undertaking

Four critical considerations are taken into consideration when determining if the regulator should accept an undertaking:

• What is the position of the consumers and investors whose interests have been, or may have been, harmed by the suspected conduct? For example, when ASIC accepted the undertaking with Multiplex, it ensured the protection of the investors who might have been affected by the alleged offence. Multiplex Ltd undertook to pay an amount up to $32 million in total to settle claims of ultimate beneficial owners in respect of particular Multiplex stapled securities.

• What is the effect of the enforceable undertaking on the regulated population as a whole?

• What is the effect of the enforceable undertaking on the regulated person’s future conduct? Will it deter the alleged offender from future breaches of the law?

• How will the community benefit from entering into an undertaking? A number of promisors have agreed to implement community services projects as part of their undertaking. For example, ASIC believed that Michael Anthony Casey allegedly failed to act efficiently in the performance of his duties as a holder of a dealer’s license. In 1999, he entered into an undertaking with ASIC in which he agreed to refrain from acting as a representative of a dealer or investment advisor for two months and to fulfil some educational requirements. He also promised to cooperate with ASIC and the Australian Securities Exchange in the preparation and presentation of seminars in Sydney and Melbourne that would be open to all designated trading representatives. The presentations and seminars were to consider issues of law, practice and procedure relevant to acting as a designed trading representative. [23]

In accordance with its guidance, ASIC will consider the following factors before entering into an undertaking:

• Was the alleged breach of the law inadvertent? In a number of undertakings, ASIC acknowledges that the breach was inadvertent.

• Was the alleged breach a result of the conduct of one or more individual officers or employees of the company?

• What is the level of experience and seniority of the alleged offender?

• Has the alleged offender co-operated with ASIC? Most of the undertakings accepted by ASIC include a clause that acknowledges the fact that the promisor co-operated with ASIC.

• Is the alleged offender prepared to publicly acknowledge ASIC’s concerns in relation to the conduct? The enforceable undertakings usually have a clause stating that the promisor acknowledges ASIC’s concern. Such a clause is not an admission of liability.

• Will it achieve an effective outcome?

• Is the person likely to comply with the enforceable undertaking? This is an important requirement since ASIC does not usually monitor closely the undertakings. The corporate regulator will leave it to the promisor, or to an independent expert hired by the promisor, to monitor its compliance with the undertaking. There is a high reliance on self-regulation. Accordingly, if the alleged offender does not have a good record of compliance with the law, ASIC will not enter into an undertaking with that person because a breach of an undertaking by itself is not an offence. However, this has not stopped ASIC from entering into undertakings with repeat offenders. For instance, ASIC accepted an undertaking from Cash Now Pty Ltd and John Anthony Falting in relation to breaches of the fundraising provisions of the Corporations Act 2001 (Cth). ASIC entered into the undertaking on 20 April 2006 with these parties, even though the promisors were repeat offenders (in October 2003 they were involved in breaches of the fundraising provisions but they stopped their conduct after they were contacted by ASIC in relation to the matter).[24]

The ASIC guide notes that ASIC will not accept an enforceable undertaking in relation to a matter that has been referred to a specialist body for determination or resolution.

However, is there a specific category that ASIC targets when accepting an enforceable undertaking?

The process of entering into an enforceable undertaking may be initiated by a company, an individual or a responsible entity, or as a result of a discussion with ASIC. However, ASIC cannot compel a person to enter into an enforceable undertaking. Similarly, a person cannot oblige ASIC to accept an enforceable undertaking.[25]

When looking at ASIC’s register of enforceable undertakings, it becomes apparent that the majority of those that gave enforceable undertakings were companies. This trend is normal because we are in a society where corporations are an essential part of our existence and the influence of such organisations is felt more and more every day. As a result, the best way to deal with these entities is by negotiating with them.[26]

As for the individuals that accepted the enforceable undertakings, in 1998 ASIC seemed to target company directors who had breached their directors’ duties. But with every year, there seems to be a slide in the number of directors targeted for enforceable undertakings. ASIC seems to be targeting another category instead: individuals dealing with securities and investment advice. From 1999 to 2006, this was the dominant group of individuals who give enforceable undertakings.[27] Most of the offences allegedly committed by the individuals were in relation to breaches of their duties as securities dealers or investment advisers. However, from January 2007 to June 2007, the three individuals who entered into enforceable undertakings with ASIC did not deal with securities and investment advice. One was a liquidator while the other two were auditors, and the undertakings were in relation to breaches of their respective duties.

When looking at the register of enforceable undertakings, it becomes obvious that from 1998 until June 2007, most of the companies who gave enforceable undertakings were involved in financial services. As a consequence, we can say that ASIC seems willing to give enforceable undertakings to people in that field. It is also important to note that companies of all shapes and sizes have entered into undertakings with ASIC. Listed companies, unlisted public companies, and proprietary companies have all entered into undertakings with ASIC. Accordingly, undertakings can be seen as a sanction that can be adapted to any type of alleged offender, be it a company or an individual.[28] A few examples of frequent alleged offences that were subject to undertakings are the following:

• operating and managing an investment scheme without a licence;

• carrying on a business of securities or investment advice without a licence;

• managing an unregistered investment scheme;

• concerns related to compliance;

• carrying on a business as an insurance company without a licence;

• misleading statements in prospectuses; and

• lack of disclosure.

However, from January 2007 to June 2007, ASIC only accepted an enforceable undertaking from one company. The enforceable undertaking was in relation to financial services.[29]

Some enforceable undertakings have been given by corporations and individuals at the same time. Usually, in this case, the individuals are the directors of the companies giving the enforceable undertakings. The individuals will usually agree to ensure that the company will comply with the undertaking. If that does not happen, then the individual and the company will find themselves in breach of the undertaking. The risk that they will be held liable for the breach is an incentive for directors to ensure the compliance of their company with the terms of the undertakings.[30]

It is important to remember that the alleged offences that may lead to an enforceable undertaking can cover wide areas of the law. In ASIC v Edwards,[31] the court pointed out the wide import of the words ’in connection with’ that are present in s 93AA of the ASIC Act. This means that ASIC may accept an undertaking in relation to any breach of the law as long as the breach is in connection with ASIC’s powers. Furthermore, the expression ‘in connection with’ was given a wide scope of operation by Kitto J in Berry v Federal Commissioner of Taxation, as requiring ‘a substantial relation, in a practical business sense’[32]. The test does not necessarily require an immediate causal relationship.[33]

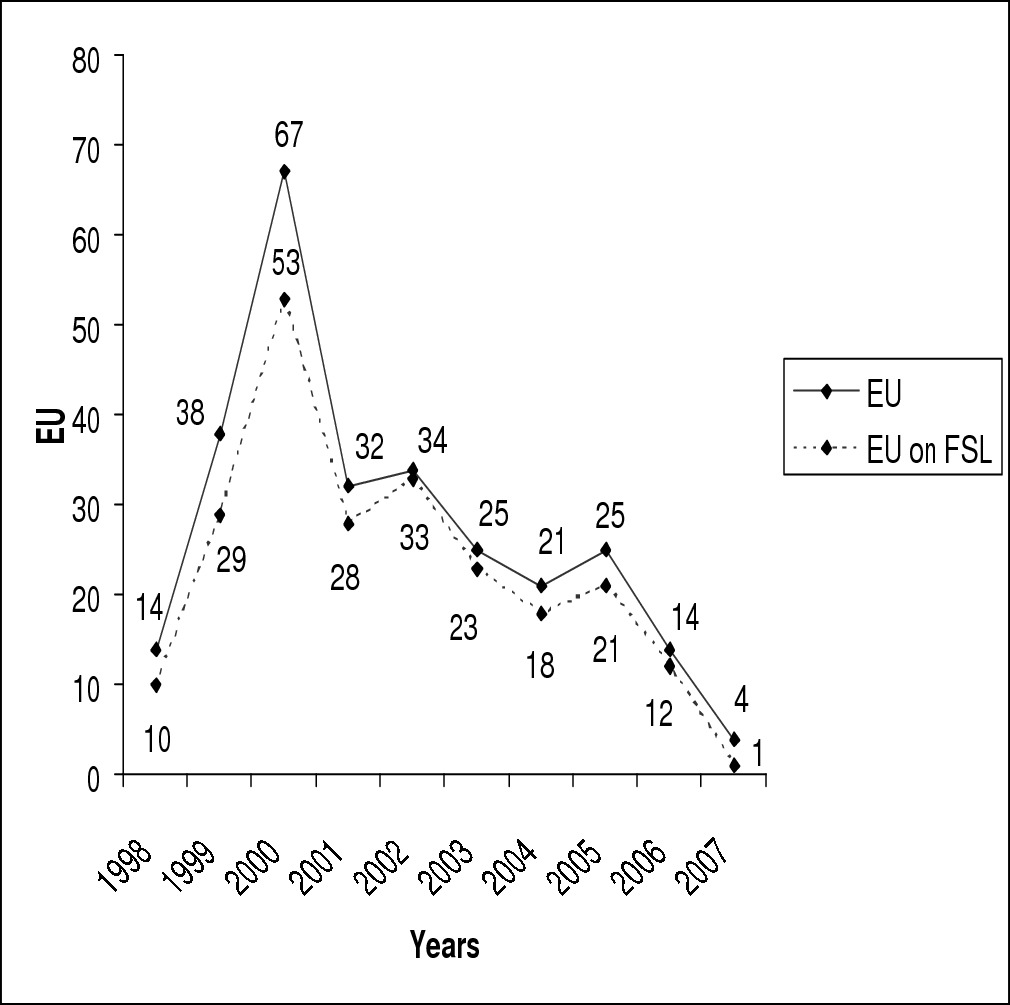

Even though the regulator can enter into an undertaking in different areas, an overview of enforceable undertakings shows that ASIC has been using enforceable undertaking in relation to alleged breaches of financial services law. This is shown in Diagram 3.

Diagram 3: Enforceable undertakings and financial service law[34]

Diagram 3 illustrates the fact that most of the enforceable undertakings that were accepted by ASIC were in the area of financial services. Out of 274 undertakings accepted by ASIC, 228 are in relation to alleged breaches that deal with financial services. This trend seems to continue today. In the year 2006, for example, 12 out of the 14 undertakings were in relation to alleged breaches of financial services provisions.

V. PROMISES GIVEN IN AN ENFORCEABLE UNDERTAKING

The content of each undertaking depends on the gravity of the alleged offence. The most common promises included in an undertaking are the following: [35]

• stop committing the alleged offence;

• put a compliance program in place;

• agree to a voluntary self-ban;

• fulfil certain educational requirements;

• compensate affected parties;

• be involved in community services; and

• disclose the undertaking to a certain category of people.

Other promises, like deregistering a company and suspending or revoking a license, may also form part of an undertaking. However, they are used considerably less often then the promises mentioned above, and are not discussed in this article.

ASIC and the alleged offender may negotiate which one of these promises may be included in an enforceable undertaking. However, the advantage of an enforceable undertaking over court action is that the enforceable undertaking may contain promises that are beyond the court’s power. Mansfield J noted that the power of a statutory authority empowered by such a provision to accept an enforceable undertaking is more comprehensive than that of a court, which is subject to certain restraints.[36]

Accordingly, it may be argued that enforceable undertakings may enable parties to reach a more flexible and arguably appropriate resolution than court order because ss 93A(1) and 93AA(1) of the ASIC Act gives wider power to ASIC to accept court enforceable undertakings than the court when it directly accepts undertakings or makes orders.[37] There is some judicial support of this latitude. In Medibank Private Ltd v Cassidy,[38] the court has held that it cannot order compensation for non-parties to a proceeding. However, a number of undertakings are often accepted by ASIC in order to provide refunds or compensation since one of the aims of enforceable undertaking is corrective action. As an enforceable undertaking is not confined to what a court might ordinarily order, such a sanction may also remedy legislative ‘gaps’.

Furthermore, through these promises ASIC hopes to achieve the following goals: [39]

• protecting the public to ensure general and personal deterrence;

• implementing preventive measures to prevent future breaches, for example by using compliance or educational programs; and

• implementing corrective measures such as compensation or corrective advertisement.

Through the promises mentioned above, ASIC has large latitude to achieve these outcomes. The seven main promises mentioned above interact when dealing with certain alleged offences. Diagram 4 is the author’s graphical expression of this interaction.

Ban

.

Compensation

Education

Stop offending behaviour

Community Services

Compliance

Disclosure

Diagram 4: The interaction of the different promises in undertakings

In theory, promises, such as stopping the alleged breach of the law and imposing a voluntary ban on the promisor, are aimed at protection of the public. These promises ensure protection by deterring the promisor from committing the alleged breach again. They also influence outsiders, who will think twice before committing similar breaches, knowing that ASIC will take action against them. The goals of the promises, such as the implementation of a compliance program and the push for education, are the prevention of future breaches of the law. The promisor will be aware of the law and will implement safeguards for the prevention of similar breaches. The aim of disclosure, compensation and community services is to correct the damage that the alleged offender caused.

One prominent example that illustrates these aims is the case of Multiplex Ltd. ASIC was concerned that Multiplex had breached the continuous disclosure rules. As a consequence of ASIC’s inquiry into the matter, Multiplex entered into an enforceable undertaking with ASIC, in which it promised to compensate the investors for their loss and to engage an external consultant to reduce the possibility of a similar breach from occurring.[40] In this example, the enforceable undertaking protected the public through a quick resolution of the problem. It also had a preventive effect by ensuring that Multiplex’s compliance program improved, thus guarding against future breaches. Additionally, the enforceable undertaking dealt with the results of the alleged breach by forcing Multiplex to pay $32 million to people affected by the alleged breach.

In another example, ASIC was concerned that Mortgage and General Financial Services Pty Ltd was selling products in contravention of its licence restrictions. Additionally, the regulator believed that this licensed securities dealer was contravening its obligations as a securities dealer by failing to properly train and supervise the representatives involved in selling certain financial products. An enforceable undertaking was entered into in which Mortgage and General Financial Services Pty Ltd undertook to stop the sale of the product and to send letters to clients notifying them of the enforceable undertaking and of their rights to rescind their agreement with the promisor if they wish to do so. The company also promised to ensure that licence conditions were complied with through the establishment and implementation of certain compliance measures. It also undertook to ensure that its representatives completed the necessary training.[41] In this case, it can be seen that the public was protected through ASIC’s action since the organisation stopped the breach. ASIC took corrective action to fix the consequences of the alleged breach by ensuring that the promisor publicised its action to the clients and by informing the clients of their rights. Finally, the undertaking prevented future breaches of the licence conditions from occurring through the establishment of compliance measures and staff training.

Another example where the goals of an enforceable undertaking were achieved is the enforceable undertaking given by Robert Hugh Iddon to ASIC. In this case, ASIC suspected that Iddon was promoting investment schemes that were not registered under the Corporations Act and that he did not hold a licence to deal in securities or to provide investment advice. As a result of such alleged action, ASIC entered into an enforceable undertaking with Iddon in which he undertook to stop his conduct, inform his clients about the content of the enforceable undertaking, and advise the clients of their rights to receive a refund. Additionally, Iddon promised not to deal with investment advice until he had been issued a licence.[42] Thus, the enforceable undertaking protected the public by stopping the alleged breach from occurring. The undertaking also led to the rectification of the consequences of the alleged breaches through the disclosure of the undertaking to the affected clients and through the offering of a refund to those people. Such an undertaking may have resulted in the return of more than $90,000 to investors. Additionally, this undertaking prevented future breaches through the promise not to deal with securities or investment advice without a licence.

VI. CONSEQUENCE OF A BREACH OF AN ENFORCEABLE UNDERTAKING

One of the characteristics of an enforceable undertaking is the possibility for the regulator to enforce the undertaking in court in case of non-compliance with the terms of the undertaking. Weinberg J noted that a breach of an undertaking ‘is a matter that will be viewed with the utmost seriousness’.[43] Furthermore, if the court finds that the enforceable undertaking has been breached, the court may make any order it sees fit to stop the breach of the undertaking and the law. The statute[44] has given the courts great latitude in relation to this matter.

However, it is important to note that, when ASIC discovers that an enforceable undertaking has been contravened, it will not go directly to the court to enforce the undertaking using ss 93A(4) and 93AA(4) of the ASIC Act. Rather, if an undertaking is not complied with, ASIC usually enters into negotiations with the alleged offender. If the consultations fail, ASIC then commences an action in court. For instance, Perpetual Plantations of Australia Pty Ltd entered into an undertaking with ASIC on 10 February 2003. The company allegedly operated unregistered managed investment schemes. It promised in the undertaking to stop operating an unregistered scheme. The company also agreed to take all necessary actions to enable it to change its type from a proprietary company to a public company.[45]

But it failed to comply with the terms of the initial undertaking. Accordingly, the company proposed to ASIC to wind up all its unregistered schemes in May 2005. ASIC agreed to this proposal.[46]

In case the promisor breaches the undertaking, ASIC sometimes encloses another promise within the first undertaking. ASIC may state that if the alleged offender does not comply with the undertaking, more drastic undertakings will come into play. For example, on 22 June 2000, Neil John White and Glen Rainer Meuwissen gave ASIC an undertaking in relation to their alleged breaches of the duties of a representative of a securities dealer. In it, they promised to put in place a compliance program and to disclose the undertaking to their clients. However, ASIC added an extra clause to the undertaking stating that if the undertaking were breached in the future, both promisors would agree to a voluntary ban from dealing with securities or investment advice.[47]

It can be clearly seen that in this case there was an escalation in the gravity of the additional promise. ASIC started with a relatively light undertaking (implementing a compliance program). But if there was a breach of this promise, it was willing to move toward the tougher sanction of a voluntary ban. If the breach persisted, then ASIC could go to court. Such an escalation is illustrated by Diagram 5.

Court action

In case of breach of the undertaking: warning and new negotiation. The action here might lead to deregistration or suspension of license.

Acceptance of an enforceable undertaking by the regulators

Diagram 5: Steps taken when an enforceable undertaking is breached[48]

The fact that an enforceable undertaking can be enforced in court is a significant feature of this sanction. It provides a strong incentive for alleged offenders to comply with the undertakings they give. They will be aware that if they do not comply, they may end up in court. Such an outcome will not appeal to them on the assumption that they accepted the enforceable undertaking to escape litigation in the first place. Furthermore, an application of the pyramid illustrates the fact that the regulator is willing to use all the sanctions that are at its disposal.

An enforceable undertaking is one of the many types of ammunition available to the corporate regulator. Through settlement, it allows ASIC and the alleged offender to reach plausible outcomes to deal with alleged breaches of the law. Even though the corporate regulator has used this sanction mostly in the area of financial services, the enforceable undertaking may be accepted in different situations. It is a very versatile sanction.

An enforceable undertaking is a great remedy available to the regulator because it allows it to reach the following goals: protection of the public, prevention of future breaches and corrective measures are usually achieved through an enforceable undertaking, as shown by the examples discussed in this article. Accordingly, it may result in a better outcome than other sanctions at the regulator’s disposal. Furthermore, an enforceable undertaking has a better outcome than a mere settlement because it is enforceable in court. If the promisor fails to comply with an enforceable undertaking, the regulator may remedy such a breach by enforcing the undertaking in court. In short, an enforceable undertaking may be seen as a new form of settlement that ensures compliance with the law without a need for court involvement.

[1] The ACCC accepted over 800 enforceable undertakings from 1993 to 2006.

[2] Christine Parker, ‘Restorative justice in business regulation? The Australian Competition and Consumer Commission’s use of enforceable undertakings’ (2004) 67(2) Modern Law Review 209-246; Marina Nehme ‘Enforceable Undertakings in Australia and Beyond’ (2005) 18 Australian Journal of Corporate Law 68-87. Most of the occupational health and safety regulators today have the sanction of enforceable undertakings at their disposal.

[3] Australian Securities and Investments Commission Act 2001 (Cth) ss 93AA, 93A.

[4] Ibid.

[5] Australian Securities and Investments Commission Act 2001 (Cth) ss 93AA(1), 93A(1).

[6] Australian Securities and Investments Commission Act 2001 (Cth) ss 93AA(4)(a), (d), and 93A(4)(a), (d).

[7] Financial Sector Reform (Amendments and Transitional Provisions) Act 1998 (Cth), amending of the Australian Securities Commission Act 1989 (Cth), Item 11.

[8] Explanatory Memorandum, Financial Sector Reform (Amendments and Transitional Provisions) Bill 1998 (Cth).

[9] Australian Securities and Investments Commission Act 2001 (Cth) s 93AA, 93A.

[10] House of Representatives Committee on Legal and Constitutional Affairs, Parliament of Australia, Mergers, Monopolies and Acquisitions - Adequacy of Existing Legislative Controls (1991) Recommendation 19; House of Representatives Committee on Legal and Constitutional Affairs, Parliament of Australia, Mergers, Takeovers and Monopolies: Profiting from Competition (1989) Recommendation 9.

[11] Bills Digest No 164 1999-2000 Aviation Legislation Amendment Bill (No 2) 2000, <http://www.aph.gov.au/Library/Pubs/bd/1999-2000/2000bd164.htm> at 30 December 2004.

[12] Christine Parker, ‘Arm-Twisting, Auditing and Accountability: What regulators and compliance professionals should know about the use of enforceable undertakings to promote compliance’ (Presentation to the Compliance Institute, Melbourne, 28 May 2003) <http://www.cccp.anu.edu.au/Parker_ACI_2805031.pdf> at 31 December 2004.

[13] Neil Andrews, ’If the Dog Catches the Mice: The Civil settlement of Criminal Conduct under the Corporations Act and the Australian Securities and Investments Act’ (2003) 15 Australian Journal of Corporate Law 137, 154.

[14] Ian Ayres and John Braithwaite, Responsive Regulation (1992) 35-36.

[15] Each regulator has a different ‘pyramid’ that will apply depending on the range of sanctions that is available to the regulator, e.g. not all agencies have license suspension as a power or function.

[16] This pyramid is based on Braithwaite and Ayres’ pyramid of enforcement.

[17] ASIC, Annual Report 2000-2001, 27.

[18] Ibid 24.

[19] ASIC, Enforceable Undertakings, an ASIC Guide (March 2007) [3.8] <www.asic.gov .au> at 26 April 2007.

[20] ASIC, Enforceable Undertaking: Multiplex Limited, Document No 017029205 (20 December 2006).

[21] ASIC, Enforceable Undertaking: Nomura International PLC, Document No 008547314 (16 February 1999).

[22] This will discussed in more detail in the paragraph entitled ‘Promises Given in an Enforceable Undertaking’.

[23] ASIC, Enforceable Undertaking: Michael Anthony Casey, Document No 008547357 (9 July 1999).

[24] ASIC, Enforceable Undertaking: Cash Now Pty Ltd and John Anthony Falting, Document No 017029196 (20 April 2006).

[25] Ibid.

[26] ASIC, Enforceable Undertakings Register <http://www.asic.gov.au> at 30 June 2007. There are 274 undertakings listed in the register of enforceable undertakings.

[27] Ibid.

[28] Ibid.

[29] ASIC, Enforceable Undertaking: First Capital Financial Planning, Document No 017029207 (11 May 2007).

[30] ASIC, Enforceable Undertakings Register <http://www.asic.gov.au> at 3 May 2007.

[31] Australian Securities and Investments Commission v Edwards [2004] NSWSC 1044; (2004) 51 ACSR 320, 324.

[32] [1953] HCA 70; (1953) 89 CLR 653, 658-659

[33] Our Town FM Pty Ltd v Australian Broadcasting Tribunal [1987] FCA 301; (1987) 16 FCR 465, 479-480 (Wilcox J).

[34] ASIC, Enforceable Undertakings Register, <www.asic.gov.au> at 12 August 2007. For the purpose of this figure only, enforceable undertaking is abbreviated to EU.

[35] ASIC, Enforceable Undertakings Register <http:// www.asic.gov.au> at 7 January 2005.

[36] Australian Competition and Consumer Commission v Woolworths (South Australia) Pty Ltd [2003] FCA 530; (2003) 198 ALR 417, 433. It is important to note that due to the similarity between s 87B of the Trade Practices Act and ss 93A and 93AA of the ASIC Act, the court’s judgments in relation to these sections are regularly cross referenced.

[37] Parker, above n 12, 15-19.

[38] Medibank Private Ltd v Cassidy [2002] FCAFC 290; (2002) 124 FCR 40.

[39] Australian Law Reform Commission, Compliance with the Trade Practices Act 1974, Report No 68 (1994) 38. It is important to remember that enforceable undertaking is an administrative sanction and its goals and aims are not to punish the promisors.

[40] ASIC, Enforceable Undertaking: Multiplex Limited, Document No 017029205 (20 December 2006).

[41] ASIC, Enforceable Undertaking: Mortgage and General Financial Services Pty Ltd, Document No 01702960 (17 October 2002).

[42] ASIC, Enforceable Undertaking: Robert Hugh Iddon, Document No 008 547 513 (27 April 2001).

[43] Australian Competition and Consumer Commission v Alinta 2000 Ltd [2007] FCA 1362, [3].

[44] Australian Securities and Investments Commission Act 2001 (Cth), ss 93AA(4), 93A(4).

[45] ASIC, Enforceable undertaking: Perpetual Plantations of Australia, Dee Dee Fleming (formerly Margaret Dianne Fleming) and Donald Brownlie Fleming, Document Nos 017029077, 017029078, 017029079 (10 February 2003).

[46] ASIC, ‘South Australian pistachio plantation scheme to be wound up’ (Press release, 23 December 2004) <http://www.asic.gov.au/asic/ASIC_PUB.NSF/byid/B8B19F36ADCB3091CA256F720082AD52?opendocument> accessed 6 May 2005.

[47] ASIC, Enforceable Undertaking: Neil John White and Glen Rainer Meuwissen, Document No 008547449 (22 June 2000).

[48] This pyramid is based on Braithwaite and Ayres’ pyramid of enforcement. This author has modified it by adding enforceable undertakings to the mix of sanctions available to the regulators. Ayres and Braithwaite, above n 14, 35-36.

AustLII:

Copyright Policy

|

Disclaimers

|

Privacy Policy

|

Feedback

URL: http://www.austlii.edu.au/au/journals/UWSLawRw/2007/4.html