Commonwealth of Australia Explanatory Memoranda Commonwealth of Australia Explanatory Memoranda

Commonwealth of Australia Explanatory Memoranda Commonwealth of Australia Explanatory Memoranda[Index] [Search] [Download] [Bill] [Help]

1998-1999-2000

THE PARLIAMENT OF THE COMMONWEALTH OF AUSTRALIA

HOUSE OF REPRESENTATIVES

NEW BUSINESS TAX SYSTEM (MISCELLANEOUS) BILL (No. 2) 2000

EXPLANATORY MEMORANDUM

(Circulated by authority of the

Treasurer, the Hon Peter

Costello, MP)

ISBN: 0642 431248

The following abbreviations and acronyms are used throughout this Explanatory Memorandum.

|

Abbreviation

|

Definition

|

|---|---|

|

A Platform for Consultation

|

Review of Business Taxation: A Platform for Consultation

|

|

A Tax System Redesigned

|

Review of Business Taxation: A Tax System Redesigned

|

|

ABN

|

Australian Business Number

|

|

AD/RLA

|

accident and disability/residual life assurance

|

|

ADF

|

approved deposit fund

|

|

ANTS

|

Government’s Tax Reform Document: Tax Reform: not a new tax, a new

tax system

|

|

ASIC

|

Australian Securities and Investments Commission

|

|

ATO

|

Australian Taxation Office

|

|

BAS

|

business activity statement

|

|

Capital Gains Tax Act

|

New Business Tax System (Capital Gains Tax) Act 1999

|

|

CFCs

|

controlled foreign companies

|

|

CGT

|

capital gains tax

|

|

COIN

|

Company and Superannuation Fund Instalment System

|

|

Commissioner

|

Commissioner of Taxation

|

|

CS/RA

|

complying superannuation/roll-over annuity

|

|

EIB

|

eligible insurance business

|

|

ETP

|

eligible termination payment

|

|

GAAR

|

general anti-avoidance rule

|

|

GDP

|

gross domestic product

|

|

GIC

|

general interest charge

|

|

Income Tax Rates Act No. 1

|

New Business Tax System (Income Tax Rates) Act (No. 1) 1999

|

|

Income Tax Rates Act No. 2

|

New Business Tax System (Income Tax Rates) Act (No. 2) 1999

|

|

Integrity and Other Measures Act

|

New Business Tax System (Integrity and Other Measures) Act

1999

|

|

ITAA 1936

|

Income Tax Assessment Act 1936

|

|

ITAA 1997

|

Income Tax Assessment Act 1997

|

|

Life Insurance Act

|

Life Insurance Act 1995

|

|

NBTS Miscellaneous Bill 1999

|

New Business Tax System (Miscellaneous) Bill 1999

|

|

NCS

|

non-complying superannuation

|

|

PAYG

|

Pay As You Go

|

|

PST

|

pooled superannuation trust

|

|

RBA

|

running balance account

|

|

RSA

|

retirement savings account

|

|

TAA 1953

|

Taxation Administration Act 1953

|

|

the Recommendations

|

Review of Business Taxation: A Tax System Redesigned

|

|

the Review

|

Review of Business Taxation

|

|

Transitional Provisions Act

|

Income Tax (Transitional Provisions) Act 1997

|

General outline and financial impact

Schedule 1 to this Bill introduces measures into the ITAA 1997 to prevent multiple recognition of losses of a company where:

• there has been a change in ownership or control in the company; or

• a liquidator has declared the company’s shares to be worthless.

Date of effect: The measures apply where substantial changes of ownership occur after 1 pm, by legal time in the Australian Capital Territory, on 11 November 1999.

Proposal announced: This proposal was announced in Treasurer’s Press Release No. 74 of 11 November 1999 (refer to attachment E).

Financial impact: The financial impact of this measure is included in the estimate for measures to prevent inter-entity loss multiplication. The financial impact of these measures is set out in the following table:

|

2000-2001

|

2001-2002

|

2002-2003

|

2003-2004

|

2004-2005

|

|

$15m

|

$20m

|

$25m

|

$20m

|

$25m

|

Compliance cost impact: There are compliance costs associated with determining the tax value adjustments to affected equity in debt interests. However, special relief is provided to minimise the costs associated with complying with this measure.

Schedule 1 to this Bill amends the ITAA 1997 to provide an appropriate link to the inter-entity loss measures by:

• amending the continuity of ownership test applying to company losses and bad debts; and

• aligning the application date of the unrealised loss measures (contained in the Integrity and Other Measures Act) with that of the inter-entity measures.

This Bill also makes technical amendments to measures dealing with the continuity of ownership test, unrealised losses, excess mining deductions and 13-month prepayments, all of which are contained in the Integrity and Other Measures Act.

Date of effect: Technical refinements to the continuity of ownership tests take effect for losses claimed in an income year ending after 21 September 1999. The other losses measures apply where substantial changes of ownership occur after 1pm by legal time in the Australian Capital Territory on 11 November 1999. Technical amendments to prepayments rules apply in relation to assessments for an income year ending after 21 September 1999. These amendments only apply to expenditure incurred by a taxpayer after 11.45 am, by legal time in the Australian Capital Territory, on 21 September 1999. The amendment relating to excess mining deductions applies to assessments for the 1999-2000 income year and later.

Proposal announced: The measures linked to the inter-entity measures were announced in Treasurer’s Press Release No. 74 of 11 November 1999 (refer to Attachment E). The technical refinements give effect to the measures announced in Treasurer’s Press Release No. 58 of 21 September 1999 (refer to Attachment Q).

Financial impact: The financial impact of this measure is included in the estimate for measures to prevent inter-entity loss multiplication.

Compliance cost impact: Reduced compliance costs are expected from linking the continuity of ownership test to the new inter-entity measure, as this will streamline the rules that apply to entities. Reduced compliance costs are also expected in relation to the unrealised loss measures from various rules providing compliance relief. The measures may increase record-keeping requirements regarding the direct and indirect ownership in a loss company.

Schedule 1 to this Bill makes amendments to the following provisions in the ITAA 1997:

• Subdivision 170-C, which prevents loss transfers between wholly-owned company groups from being duplicated (loss duplication measures); and

• Subdivision 170-D, which defers capital losses or deductions in certain cases (linked group transfer measures).

Date of effect: The amendments clarifying the application of Subdivision 170-C apply from 22 February 1999, the original application date of application of the loss transfer measure.

The amendments restricting cost base uplifts will apply from the date of introduction of this Bill.

Proposal announced: These amendments arise from the loss duplication and linked group transfer measures, announced in Treasurer’s Press Release No. 58 of 21 September 1999 (refer to Attachment Q).

Financial impact: The financial impact of this measure is included in the estimates reported under the following measures:

• preventing a deduction and a capital loss arising from a single economic loss; and

• transfer or creation of assets by companies that are members of linked groups;

dealt with in the Integrity and Other Measures Act.

Compliance cost impact: There are no additional compliance costs associated with amendments to these measures.

Schedule 2 to this Bill amends the ITAA 1936 and the ITAA 1997 to:

• broaden the tax base for life insurers by largely taxing the various businesses of life insurers on a comparable basis to those types of businesses generally; and

• broadly tax the current pension business of superannuation funds consistently with that of life insurers.

Proposal announced: This proposal was announced in Treasurer’s Press Release No. 58 of 21 September 1999 (refer to Attachment N).

Financial impact: The following financial impact includes the impact of Review proposals affecting policyholders, which will be included in a later Bill:

|

1999-2000

|

2000-2001

|

2001-2002

|

2002-2003

|

2003-2004

|

2004-2005

|

|

–$30m

|

$200m

|

$180m

|

$235m

|

$255m

|

$275m

|

Compliance cost impact: Broadening the tax base for life insurers should reduce ongoing compliance costs by increasing certainty and integrity of the tax base. However, there are some implementation and transitional costs that will arise.

Part 1 of Schedule 3 to this Bill amends the ITAA 1936 to make consequential amendments to the dividend imputation regime to provide for franking credits and debits to arise for:

• the payment and refund of income tax under the PAYG instalments system; and

• PAYG rate variation credits.

Proposal announced: This proposal has not previously been announced.

Financial impact: There is no financial impact arising from the introduction of these measures.

Compliance cost impact: If this measure has any impact on compliance costs, it will involve a small increase in those costs.

Part 2 of Schedule 3 to this Bill amends the dividend imputation system of the ITAA 1936 as it applies to life insurers so that:

• franking credits and debits arise in relation to tax paid on income actually allocated to shareholders; and

• the imputation system applies to virtual PSTs of life insurance companies.

Proposal announced: This proposal was announced in Treasurer’s Press Release No. 58 of 21 September 1999 (refer to Attachment O).

Financial impact: The financial impact of this measure is included in the overall estimates reported under the measure broadening the tax base for life insurers.

Compliance cost impact: This measure may impose some additional compliance costs on life insurers by requiring calculations that reflect the true underlying circumstances rather than applying an arbitrary rule. However, the application of accepted accounting practices will limit any additional complexity.

Part 3 of Schedule 3 to this Bill amends the ITAA 1936 to ensure that the reduction in the company tax rate from 36% to 34% is correctly reflected in the dividend imputation system in relation to:

• life insurance companies;

• PAYG instalments payable by early balancing companies; and

• estimated debit determinations.

Proposal announced: These measures have not been announced. However, they arise from the proposal to reduce the company tax rate from 36% to 34%. This was announced in Treasurer’s Press Release No. 58 of 21 September 1999 (refer to Attachment A).

Financial impact: The financial impact of this measure is included in the overall estimates reported under the measure reducing the company tax rate, dealt with in the Income Tax Rates Act No. 1.

Compliance cost impact: The amendments to the conversion of franking account provisions will cause a small, one-off cost for companies affected by the measure arising from implementing changes to their systems. However, the method adopted in the conversion of franking account provisions minimises ongoing compliance costs.

Part 4 of Schedule 3 to this Bill amends the franking credit trading provisions in Division 1A of Part IIIAA of ITAA 1936 to increase the threshold for the small shareholder exemption under the holding period rule from $2,000 to $5,000.

Date of effect: This change will apply to assessments for the 1999-2000 income year, and later income years.

Proposal announced: This proposal was announced in Treasurer’s Press Release No. 74 of 11 November 1999 (refer to Attachment F).

Financial impact: A minimal loss to revenue.

Compliance cost impact: There is expected to be a reduction in compliance costs mainly arising from individual taxpayers entitled to a franking rebate between $2,000 and $5,000 no longer having to consider the application of the 45 day rule.

Schedule 4 to this Bill amends the ITAA 1997 so that the cost-base adjustment that is made where a capital payment is received for a trust interest (CGT Event E4) reflects the CGT discount and CGT small business concessions.

Proposal announced: This measure was foreshadowed in the explanatory memorandum to the Capital Gains Tax Act, but was otherwise not announced.

Financial impact: The financial impact for these changes is included in the estimates reported under the measures providing small business relief dealt with in the Capital Gains Tax Act.

Compliance cost impact: None.

Schedule 5 to this Bill amends the scrip for scrip roll-over provisions in the ITAA 1997 by:

• clarifying the circumstances in which roll-over can be used;

• providing cost base rules for acquired equity; and

• limiting the availability of roll-over where both the original and acquiring entities are non-residents.

Date of effect: The amendments generally apply from 10 December 1999. The amendments affecting non-resident companies apply from 14 April 2000.

Proposal announced: This proposal has not previously been announced.

Financial impact: The financial impact for these changes is included in the estimates reported under the measures providing scrip for scrip roll-over dealt with in the Capital Gains Tax Act. The amendments in this Bill do not have any further revenue impacts. The changes to the cost base rules and the non-resident roll-over measure are revenue protection measures.

Schedule 7 to this Bill inserts rules in Part 2-10 of Schedule 1 to the TAA 1953 to support the integrity of the PAYG instalments regime. The rules penalise entities who obtain a tax benefit or tax benefits from a scheme to avoid, defer or reduce PAYG instalments. The rules do this by imposing a penalty by way of the GIC on twice the tax benefit or tax benefits arising from the scheme. The Bill also amends the object of the PAYG instalments regime to clarify the objects and purposes of that regime.

Financial impact: No gain to revenue. The amendments will protect the PAYG instalments base and prevent significant deferral of instalments.

Compliance cost impact: Taxpayers will need to be aware of how the measures operate. However, taxpayers who are not engaged in tax avoidance activities will not be affected by these measures.

Impact: The measures in this Bill are part of the Government’s broad ranging reforms which will give Australia a New Business Tax System. These reforms are based on the Recommendations of the Review that the Government established to consider reforms to Australia’s business tax system.

The New Business Tax System is designed to provide Australia with an internationally competitive business tax system that will create the environment for achieving higher economic growth, more jobs and improved savings, as well as providing a sustainable revenue base so that the Government can continue to deliver services for the community.

Main points:

• The potential compliance, administrative and economic impacts of the measures contained in this Bill have been carefully considered, by both the Review and the business sector. The Review focussed on the economy as a whole and concluded that there would be net gains to business, Government and the community as a whole from business tax reform.

• The measures in this Bill will reduce compliance costs as part of providing a more consistent and easily understood business tax system.

• Most of the measures in this Bill impact on a particular group of taxpayers (e.g. the life insurers imputation amendments will impact on life insurance companies) or taxpayers that undertake a particular transaction (e.g. technical amendments to the scrip for scrip roll-over provisions apply to companies involved in takeovers undertaken by way of a scheme of arrangement).

• Some of the measures have a wider impact (e.g. the measure amending the imputation system to take account of PAYG instalments will affect all entities who make instalments and have franking credits and debits arise under the imputation system).

• Most of the measures are expected to decrease compliance costs (e.g. increasing the threshold for the exemption from the franking credit trading rules). In many cases, the only increase in compliance costs is in the transition and implementation of the measure (e.g. broadening the tax base for life insurers).

• The administration costs of implementing the measures in this Bill are expected to be minimal.

Chapter

1

Inter-entity

loss multiplication

1.1 Schedule 1 to this Bill inserts new Subdivision 165-CD into the ITAA 1997. Subdivision 165-CD prevents the duplicate, or multiple, recognition of the realised and unrealised losses of a ‘loss company’ that has an ‘alteration’. An alteration is a change in the company’s ownership or control or a declaration by a liquidator that its shares are worthless.

1.2 Duplicate or multiple recognition of losses happens because the company’s losses are reflected in the values of interests (e.g. shares or debts) held directly, or indirectly, in it. Where the entity holding the interest is not an individual, this outcome is referred to below as inter-entity loss multiplication.

1.3 If a loss company has an alteration, the Subdivision prevents inter-entity loss multiplication by reducing tax attributes (reduced cost bases, costs, or deductions) for significant direct and indirect equity and debt interests in that company. Consistent with preventing inter-entity loss multiplication, the Subdivision actually calculates reductions based on the company’s losses, as discussed further at paragraphs 1.9 to 1.16.

1.4 The Subdivision applies to ‘inter-entity’ interests. ‘Inter-entity’ interests are interests held by entities in other entities. Inter-entity interests represent a significant source of loss multiplication, especially where there are tiers of entities, and entity interests, that reflect the losses of companies ‘downstream’ of them.

1.5 Interests held by, or solely on behalf of, individuals are not affected by this Subdivision. Also, interests held by certain entities are not subject to reduction under this Subdivision if there are no interests held by others in those entities on which the company’s losses can be duplicated. It will be difficult for entities with fixed interests to qualify for this exclusion, but most solvent superannuation funds and non-fixed trusts will be excluded from the Subdivision’s operation.

1.6 The Subdivision applies only to significant inter-entity interests. Broadly, a significant inter-entity equity interest is a 10% or greater interest (held directly or indirectly) in the loss company, and a significant inter-entity debt interest is a loan of $10,000 or more to the loss company, or to another entity with a significant interest in the loss company. A further requirement is that the entity must have a controlling stake (determined on an associate-inclusive basis) in the loss company.

1.7 Ordinarily, only interests held immediately before an alteration time are affected by the Subdivision. This means there is an impact on interests whose disposal triggers the alteration, as well as on interests held by entities ‘upstream’ or downstream’ of the entity that disposed of interests.

1.8 In limited circumstances, interests disposed of before an alteration time may also be affected. Broadly, interests disposed of within 12 months before an alteration time, or under an arrangement involving disposals at, or within 12 months of, that time, can be affected.

1.9 The amounts of reductions to the tax attributes of significant interests are based on realised and unrealised losses of the loss company. Calculating a company’s unused realised capital and tax (revenue) losses is generally straightforward. The calculation of unrealised losses on assets can be less straightforward and involves valuing assets. Relieving provisions are contained in the Subdivision to minimise the requirement to value assets.

1.10 This relief will limit the cost of complying with the Subdivision without significantly reducing its contribution to the integrity of the tax system. All entities can benefit from aspects of this relief, and in particular small business will benefit from most aspects of it.

1.11 To minimise the need to value assets to determine a company’s unrealised loss assets, assets acquired for less than $10,000 are disregarded, and, in most cases, items of plant can be valued at their tax written down values.

1.12 Companies and company groups in the small business sector (with net assets (on a related entity basis) of $5 million or less) are fully exempted from calculating unrealised losses.

1.13 In certain cases, companies without realised losses may not have to apply the Subdivision or calculate their unrealised losses if they would reasonably be expected to be in a ‘net unrealised gain’ position at an alteration time.

1.14 In addition, the Subdivision specifically authorises the Commissioner to provide valuation guidelines to further reduce compliance costs associated with calculating unrealised losses.

1.15 The Subdivision contains a formula to determine reductions to tax attributes based on the company’s realised and unrealised losses. This applies in straightforward cases. Another test applies in all other cases, or where the formula does not give a reasonable result.

1.16 In no case will an entity have to make a reduction that is unreasonable in the circumstances.

1.17 This Subdivision applies if a loss company undergoes an alteration after

1 pm, by legal time in the Australian Capital Territory, on 11 November 1999.

This measure was announced in Treasurer’s Press Release No. 74 of 1999 of

11 November 1999 (attachment E). The Subdivision prevents the obtaining of

deductions and capital losses (that duplicate the company’s losses) on

inter-entity interests from

11 November 1999.

1.18 Loss multiplication arises where the taxation system recognises a single economic loss more than once. Inter-entity loss multiplication can occur because losses of a company are reflected in the values of direct or indirect interests (e.g. shares and loans) in that company.

1.19 If entities are interposed between individual shareholders and a loss company, the company’s losses may be multiplied on the realisation of ‘inter-entity’ interests in the loss company. In A Tax System Redesigned, the Review recommended that the same business test be retained following a change in ownership of a loss company, subject to the removal of inter-entity loss multiplication. (Recommendation 6.9(b) on page 256 and discussion on page 257).

1.20 This Subdivision implements that recommendation by requiring appropriate reductions to the tax attributes of significant interests in a loss company that undergoes a change of ownership or control or when a liquidator declares that its shares are worthless.

1.21 This Subdivision balances integrity benefits (the prevention of inter-entity loss multiplication) with the need to contain compliance costs. Firstly, only entities with an (associate-inclusive) controlling stake in the loss company are affected, and they in turn must have a significant equity interest (10% or more) or significant debt interest ($10,000 or more). The Subdivision contains several other relieving provisions that help to contain compliance costs, especially in relation to the calculation of unrealised losses.

1.22 Subdivision 165-CD prevents inter-entity loss multiplication. This is the duplicate or multiple recognition of a company’s losses on the realisation of certain equity and debt interests held directly or indirectly in a loss company that has undergone an ‘alteration’.

1.23 An alteration involves a change in a company’s ownership or control or where a liquidator has declared its shares are worthless.

1.24 Usually, the Subdivision impacts only on interests held immediately before an alteration, but in certain cases can also apply to certain interests disposed of before that time.

1.25 The Subdivision applies only in respect of a change in a loss company’s ownership or control, or a liquidator’s declaration that its shares are worthless, where these events happen after 1 pm, by legal time in the Australian Capital Territory, on 11 November 1999.

1.26 Entities potentially required to make reductions under this Subdivision (‘affected entities’) are only those that have (alone or with associates) a controlling stake in the loss company. Also excluded are individuals, entities holding interests solely on behalf of individuals, or entities in which no other entity has held, or holds, an interest on which a capital loss or deduction might be claimed that duplicated, or duplicates, the loss company’s losses.

1.27 Affected entities may be required to reduce deductions and reduced cost bases in relation to significant interests they hold in the loss company.

1.28 A significant interest means at least a 10% (direct or indirect) inter-entity equity interest in the loss company or a debt of at least $10,000 owed directly by the loss company or by an entity with a significant interest in the loss company.

1.29 In general, reductions are required only for interests held directly or indirectly in the loss company immediately before an alteration time.

1.30 Reductions may also be required for relevant interests disposed of within 12 months before an alteration time; or where the deductions or capital losses would be realised more than 12 months before an alteration time but are part of an arrangement that also involved the disposal of interests at the alteration time or within 12 months of that time. This requirement for reductions ensures that the measures apply appropriately where an interest is disposed of in a number of stages.

1.31 For direct interests in loss companies which have only shares of one class and market value (and have not issued rights or options to acquire shares), or such shares and loans of only one type, a formula is provided to simplify the reductions. In other cases, or where the formula does not provide a reasonable outcome, the measures provide for appropriate reductions based on several factors. In no case will an entity be required to make a reduction that is unreasonable in the circumstances.

1.32 The amount of reduction is based on the total of the company’s realised and unrealised losses at the alteration time. However, it is recognised that not all of this amount will always be relevant in determining the reduction required to prevent inter-entity loss multiplication.

1.33 To assist taxpayers to comply with this measure, an obligation is placed

on any entity (other than an individual) that, in its own right, has a

controlling stake in the loss company, to provide information to its associates

that will assist them to make the reductions required. If more than one entity

has such a controlling stake (e.g. in a ‘chain’ of companies) the

entity in which no other entity (excluding individuals) has a controlling stake

(e.g. the ultimate parent) is obliged to provide the information. If the

ultimate parent is a non-resident, and there is a resident entity that would

have been required to provide the notice if the

non-resident parent had not

existed, the obligation will fall on the resident entity.

1.34 In some cases, the loss company itself may be required to provide information to holders of significant interests in it.

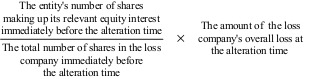

Diagram 1.1: Scheme of the Subdivision

No

No

1.35 There is no current law in relation to this measure.

1.36 The object of Subdivision 165-CD is to prevent the multiplication of a loss company’s realised and unrealised losses. The Subdivision is triggered where an alteration time occurs in respect of the company. This usually involves a change in the ownership or control of the loss company, but can also happen where a liquidator of the company declares its shares worthless, or if certain interests are disposed of before an actual alteration time.

1.37 The object of the Subdivision is achieved by requiring appropriate reductions to the values for tax purposes of certain interests (inter-entity interests) held by entities that have a controlling stake in the loss company. [Schedule 1, item 18, section 165-115J]

1.38 Multiplication of losses on inter-entity interests can occur because the company’s realised and unrealised losses are reflected in the values of interests (equity and debt) held directly or indirectly in the loss company.

1.39 This Subdivision only addresses the multiplication of losses by way of deductions or capital losses recognised in relation to these interests. It does not deal with reduced gains recognised on them because the company has made losses.

1.40 Thus, the basis for determining the quantum of reductions to reduced cost bases and deductions for interests in the loss company is the amount of realised and unrealised losses in the loss company. Unrealised gains in that company are not relevant because only ‘loss attributes’ (reduced cost bases and deductions) of interests in it are reduced or adjusted.

Example 1.1

X Co has a 100% shareholding in Y Co, having capitalised Y Co post-CGT with $10 million. X Co sells its shares to an independent buyer for $7 million. This triggers the operation of the Subdivision.

Y Co has a realised loss of $3 million (at the beginning of the income year in which the Subdivision is triggered), an unrealised loss of $1 million on one asset and an unrealised gain of $1 million on another.

The reduced cost base of X Co’s shares would be reduced by $4 million to $6 million. The cost base of $10 million is unaffected by the Subdivision so no capital gain or capital loss would be made on the sale.

If Y Co distributed the unrealised gain asset to X Co before the sale, and sold its shares for $6 million, the Subdivision would again prevent duplication of the company’s losses.

1.41 Although in general, unrealised gains are not taken into account in determining whether, and the extent to which, the Subdivision requires reductions to interests, this is subject to one exception made on compliance cost grounds.

1.42 If an alteration time occurs that is not a ‘changeover time’ for the purposes of the unrealised loss measures (Subdivision 165-CC), the company does not have any realised losses, and, if the alteration time had been a changeover time it would have been reasonable for the company to conclude that it would not have had an unrealised net loss at that time under section 165-115E, this will not be treated as an alteration time. [Schedule 1, item 18, subsection 165-115K(4)]

1.43 The effect of this is that the Subdivision will not apply. Companies with no realised losses, and no unrealised net loss at the alteration time will not be required to obtain valuations of their unrealised loss assets for the purpose of Subdivision 165-CD at a time when they are not required to do so under Subdivision 165-CC.

1.44 However, if the alteration time coincides with a changeover time, the company will have to obtain valuations of its unrealised loss assets. It already has to do this for Subdivision 165-CC purposes, so there are no additional compliance costs imposed by this requirement under this Subdivision.

1.45 Subdivision 165-CD does not require reductions to be made by individuals holding interests directly or indirectly in the loss company [Schedule 1, item 18, subsections 165-115X(5) and 165-115Y(6)]. Also excluded are interests held by trustees for individuals absolutely entitled as against them to the interests, and interests held on behalf of individuals by trustees in bankruptcy and by security holders [Schedule 1, item 18, subsections 165-115X(7) and 165-115Y(8)].

1.46 In the case of partnerships, the ‘fractional interest’ approach ensures that no special rule is required for CGT provisions where individuals hold interests in partnership in the loss company. However, for the revenue provisions, it is provided that no reduction is made under this Subdivision to interests held by a partnership of individuals. [Schedule 1, item 18, subsections 165-115X(6) and 165-115Y(7)]

1.47 It is appropriate that individuals can effectively realise the underlying net losses of the loss company by disposing of their interests in it. This is recognising only once that company’s underlying losses on an interest in the loss company. Following a change in ownership or control of the loss company, such losses may also be available to the loss company, but only if the same business test is satisfied.

1.48 Subdivision 165-CD limits multiplication of these losses by making reductions to the tax attributes of relevant ‘inter-entity’ interests in the loss company.

1.49 In addition to interests held effectively by individuals, it is appropriate to exclude certain other entities from having interests in relation to which Subdivision 165-CD may require reductions.

1.50 Such an entity is one for which no other entity (including an individual) has obtained, or can obtain, a capital loss or deduction for a direct or indirect equity or debt interest in it that reflects a loss of the underlying loss company [Schedule 1, item 18, subsections 165-115X(3) and (4) and 165-115Y(4) and (5)]. The purpose of describing an entity in this way is to ensure that no entity is excluded from having a relevant interest if there is any possibility that a loss can be duplicated on an interest in that entity.

1.51 This test potentially excludes most superannuation funds and discretionary trusts if neither a capital loss nor a deduction has been, or could be, available, in respect of an entity’s interest in the fund or trust.

1.52 However, if the superannuation fund or trust has borrowed (including a borrowing from an arm’s length borrower) the existence of a loan in respect of which a capital loss or deduction has been made or could be made by the lender that duplicates a loss of the loss company, will prevent the exclusion from applying.

1.53 The rationale for excluding most superannuation funds and discretionary trusts is that, without the exclusion, the effect of Subdivision 165-CD might be to prevent any recognition of a company’s loss in certain cases. For example, if a discretionary trust holds all the shares in a loss company, and it disposes of those shares to an unrelated party, Subdivision 165-CD could operate to prevent a capital loss or deduction arising on their disposal. If the company then fails the same business test, the loss would not be recognised in any way.

1.54 The Subdivision will not apply when calculating the attributable income of a CFC. [Schedule 1, item 67, proposed paragraph 427(ba) of the ITAA 1936]

1.55 The CFC measures prevent tax deferral by taxing Australian residents on their share of certain types of foreign source income accumulated offshore in a CFC (called attributable income). Broadly, the attributable income of a CFC is calculated as if it were a resident taxpayer. Subdivision 165-CD would therefore apply unless modifications are made to the calculation of attributable income.

1.56 In principle, the Subdivision should apply when calculating the attributable income of a CFC. Applying the measures to CFCs in the same way that they apply to residents would help ensure residents are not advantaged by accumulating amounts offshore in a CFC.

1.57 Subdivision 165-CD, however, would not mesh well in its current form with aspects of the CFC measures and could produce anomalous outcomes or uncertainty in the law. It will therefore not apply to CFCs at present. Its application to CFCs will be considered as part of the review of the CFC measures announced in the New Business Tax System: Stage 2 Response (Treasurer’s Press Release No. 74 of 11 November 1999). This will allow time to develop cohesive rules that are properly integrated with other measures.

1.58 In some situations the reductions are made as a result of the ‘disposal’ of equity or debt interests in a loss company. The Subdivision is not limited to situations where an entity ‘disposes’ of its interests to another person or entity (as understood in CGT event A1 (section 104-10)).

1.59 Subdivision 165-CD applies to a CGT event other than a disposal happening to a CGT asset in the same way as it applies to a disposal of a CGT asset [Schedule 1, item 18, subsection 165-115K(5)]. So, for example, a cancellation of shares would be covered by the Subdivision. The extension to CGT events other than a disposal also applies where the Subdivision refers to the disposal of assets by the loss company.

1.60 Where a CGT event other than CGT event A1 occurs (i.e. an event other than an actual disposal), a disposal is taken to have occurred for the purposes of Subdivision 165-CD at the time of the CGT event [Schedule 1, item 18, subsection 165-115K(5)]. For an actual disposal, the time of the disposal depends on whether the Subdivision refers to a CGT outcome (e.g. a capital loss) or to a revenue outcome (e.g. a deduction). In the first case, it is the time of the disposal under Parts 3-1 and 3-3 as applicable for CGT event A1 (e.g. the time of the contract of sale). In the second, it is the time of the disposal under the general law (e.g. the time of settlement on sale).

When does Subdivision 165-CD apply?

1.61 Subdivision 165-CD will apply if:

• a company has an alteration time;

• at the alteration time the company is a loss company; and

• one or more entities have relevant equity interests or relevant debt interests in the company immediately before the alteration time.

[Schedule 1, item 18, subsection 165-115K(1)]

1.62 By focussing on interests held immediately before the alteration time the Subdivision ensures that reductions are also made to the interests that trigger the alteration in ownership or control of the loss company. [Schedule 1, item 18, paragraph 165-115K(1)(c)]

1.63 Subdivision 165-CD may also apply to interests in the loss company that

an entity disposed of within a 12 month period before the alteration time, if

the entity had a significant equity or debt interest in the loss company

immediately before the alteration time, or would have had such an interest but

for certain disposals. [Schedule 1, item 18, section

165-115P]

1.64 The Subdivision may also apply to interests that are disposed of under an arrangement that commenced before the 12 month period (but not before the commencement time of the Subdivision) and involved the disposal of interests at the alteration time or within the 12 months before that time. [Schedule 1, item 18, section 165-115Q]

1.65 These provisions prevent an entity disposing of, or recognising losses on, interests in more than one transaction to maximise loss multiplication and prevent the ordinary application of the Subdivision.

1.66 Subdivision 165-CD may also apply to interests that are trading stock of the entity immediately before an alteration time but not where deductions or reductions in value were recognised in an income year ending more than 12 months before the alteration time. [Schedule 1, item 18, subsections 165-115ZA(5) and (6)]

1.67 An alteration time for a company is usually one where, broadly, there is a failure of the same persons to maintain a majority interest in the voting power, rights to dividends, and rights to capital in the loss company. [Schedule 1, item 18, section 165-115L].

Change of ownership

1.68 The new tests (discussed in Chapter 2) for determining whether there has been a continuity of ownership are used in Subdivision 165-CD. The changes in the continuity of ownership are measured by reference to a time that cannot be earlier than 1.00 pm by legal time in the Australian Capital Territory, on 11 November 1999. The special tracing rules for listed public companies are used in the usual way. The ‘saving provision’ which refers to circumstances where less than 50% of the loss company’s losses have been duplicated, does not generally apply for the purposes of applying Subdivision 165-CD.

1.69 However, the ‘saving provision’ that applies where the same persons have maintained a majority interest in the voting power, rights to dividends and rights to capital though they hold that interest in a different form, and less than 50% of the loss company’s unrealised net loss has been duplicated, has a particular application in this Subdivision.

1.70 If a company:

• has an alteration time which is not a changeover time under Subdivision 165-CC (e.g. where the saving provision applied);

• has no realised tax losses or net capital losses; and

• can reasonably conclude that the total unrealised gains on CGT assets it owns would be greater than or equal to the total unrealised losses on its CGT assets,

the alteration time is taken not to have occurred. This results in the Subdivision not applying in relation to the company at that time [Schedule 1, item 18, subsection 165-115K(4)]. This operates as a compliance cost saving measure, because companies will not have to obtain valuations of assets in these circumstances.

Change of control

1.71 An alteration time for a company may also happen where there is a change in its control. [Schedule 1, item 18, section 165-115M] Changes in control are measured by reference to a time that cannot be earlier than 1 pm by legal time in the Australian Capital Territory, on 11 November 1999.

Declaration by a liquidator – CGT event G3 triggered

1.72 An alteration time for a company is also taken to include a situation where a liquidator of a company makes a declaration and shareholders can obtain capital losses in respect of their shares before the company is dissolved and the shares are cancelled. [Schedule 1, item 18, section 165-115N]

1.73 Were CGT event G3 not to trigger the application of Subdivision 165-CD, liquidators’ declarations could be used to bypass the anti-loss multiplication reductions the Subdivision is designed to achieve.

What is a ‘notional alteration time’ for a company?

1.74 A company has a notional alteration time if:

• it is a loss company at an alteration time;

• an entity has a relevant equity or debt interest in the company immediately before the alteration time (or would have had a relevant equity or debt interest if it had not disposed of equity or debt at any previous notional alteration times);

• the entity disposed of a direct or indirect equity or debt interest in the company in the 12 month period before the alteration time, or disposed of equity or debt outside the 12 month period as part of an arrangement under which equity or debt was also disposed of within the 12 month period or at the alteration time; and

• immediately before the disposal the equity or debt had been part of a relevant equity or debt interest (or part of an interest that would have been a relevant equity or debt interest if other equity or debt had not been disposed of at any previous notional alteration times) held by the entity in the loss company.

[Schedule 1, item 18, subsections 165-115P(1) and 165-115Q(1)]

1.75 An ‘arrangement’ for these purposes would not include the normal repayment of a debt consistent with its terms of issue. A notional alteration time [Schedule 1, item 18, subsections 165-115P(3) and 115Q(3)] is also not an alteration time for the purposes of these sections [Schedule 1, item 18, paragraphs 165-115P(1)(a) or 165-115Q(1)(a)] so the 12 month period is not successively activated.

1.76 There is no notional alteration time if the disposal was before 1 pm, legal time in the Australian Capital Territory, on 11 November 1999. [Schedule 1, item 18, paragraphs 165-115P(1)(b) and 165-115Q(1)(b)]

1.77 Where the requirements in paragraph 1.76 are met the company’s notional alteration time is taken to be immediately before the disposal of the equity or debt [Schedule 1, item 18, subsections 165-115P(3) and 165-115Q(3)]. The equity and debt disposed of are taken to be relevant equity and debt interests of the entity immediately before the notional alteration time [Schedule 1, item 18, subsections 165-115P(4) and 165-115Q(4)]. Subdivision 165-CD then operates as it would for any other alteration time in relation to those specified equity and debt interests.

1.78 Importantly, all other equity and debt interests held by the entity in the loss company at the notional alteration time are taken not to be relevant debt or equity interests [Schedule 1, item 18, subsections 165-115P(4) and 165-115Q(4)]. This ensures that the Subdivision only affects the equity and debt disposed of. The relevant equity and debt interests of other entities will not be affected by the notional alteration time [Schedule 1, item 18, subsections 165-115P(5) and 165-115Q(5)].

1.79 When Subdivision 165-CD applies to the loss company at a future alteration time, a notional alteration time is taken not to have occurred [Schedule 1, item 18, subsections 165-115P(6) and 165-115Q(6)]. This ensures that the reductions made to the values for tax purposes of relevant equity and debt interests held at the actual alteration time are not affected by any reductions made because of the notional alteration time.

1.80 The purpose of these provisions is to prevent an entity maximising loss multiplication or preventing the application of the Subdivision by disposing of debt and equity interests in a series of steps involving an arrangement, or within a short period of time. This could occur, for example, if an entity acquires 100% of the relevant equity interests in a company before the company starts making losses. Without these provisions the entity could sell 49% of its equity in the loss company just before selling the remaining 51% and Subdivision 165-CD would not apply to the disposal of the first 49%.

1.81 These rules do not have a purpose test or a tax avoidance motive test. They operate automatically if the disposals occur within a 12 month period or under an arrangement. An arrangement is as defined by section 995-1 to be any arrangement, agreement, understanding, promise or undertaking, whether express or implied, and whether or not enforceable (or intended to be enforceable) by legal proceedings. What constitutes an arrangement in a particular situation will be a question of fact in that case.

1.82 A loss company is a company which has realised losses or unrealised losses at the alteration time. Different rules exist to determine whether a company is a loss company at the first or only alteration time in an income year, and for a second or later alteration time in the same year. [Schedule 1, item 18, sections 165-115R and 165-115S]

1.83 A company must be a loss company at the alteration time for the Subdivision to apply.

Rules for determining whether a company is a loss company at the first or only alteration time in an income year

1.84 The Subdivision contains rules about when a company is a loss company at the first or only alteration time in an income year [Schedule 1, item 18, section 165-115R]. It also provides the method for calculating the loss company’s overall loss at the alteration time. The overall loss is taken into account in making reductions under the Subdivision.

1.85 For the purpose of determining whether a company is a loss company it is assumed that a notional income year starts at the beginning of the income year in which the alteration occurs and ends at the alteration time. [Schedule 1, item 18, subsection 165-115R(2)]

Example 1.2

Company A changes ownership on 1 May 2000. To determine whether A is a loss company, section 165-115R is applied on the basis that the period from the beginning of Company A’s income year up to the alteration time, 1 May 2000, is an income year.

1.86 A company will be a loss company at an alteration time where at least one of the following is satisfied at that time:

• it has an undeducted tax loss or undeducted tax losses at the beginning of the notional income year for one or more earlier income years;

• it has an unapplied net capital loss or unapplied net capital losses at the beginning of the notional income year for one or more earlier income years;

• it has a tax loss for the income year;

• it has a net capital loss for the income year; or

• at the alteration time the company has an adjusted unrealised loss (see paragraphs 1.110 to 1.116).

[Schedule 1, item 18, subsection 165-115R(3)]

1.87 Subdivision 165-B is used to calculate whether a company has a tax loss for the notional income year. It is applied on the basis that there are no full year deductions or full year amounts, and that subsection 165-45(4) is not relevant. Subdivision 165-CB is applied similarly for net capital losses.

1.88 A tax loss that is undeducted or a net capital loss that is unapplied is disregarded if it was used in determining whether the company was a loss company in an earlier income year [Schedule 1, item 18, paragraph 165-115R(4)(a)]. This rule prevents the double counting of such losses.

1.89 Subdivision 170-D is also disregarded in determining whether the company is a loss company [Schedule 1, item 18, paragraph 165-115R(4)(b)]. This ensures that losses deferred under Subdivision 170-D are taken into account at an alteration time. It is appropriate to recognise such deferred amounts because they can be multiplied on the realisation of inter-entity interests.

Rules for determining whether a company is a loss company at a second or later alteration time in an income year

1.90 If there has been a previous alteration time in the same income year, it is assumed that the period from immediately after the last alteration time to the current alteration time is an income year. [Schedule 1, item 18, subsection 115-165S(2)]

Example 1.3

On 1 May 2000 (the first alteration time) Company A undergoes a change in ownership.

On 31 May 2000 Company A’s ownership changes again (the second alteration time). The income year for the purpose of determining whether it is a loss company at the second alteration time will be from 1 May 2000 (immediately after the previous alteration) until 31 May 2000.

1.91 A company will be a loss company at the second or subsequent alteration time where one of the following is satisfied:

• it has a tax loss for the income year;

• it has a net capital loss for the income year; or

• at the alteration time the company has an adjusted unrealised loss.

[Schedule 1, item 18, subsection 165-115S(3)]

1.92 Subdivision 170-D is disregarded in determining whether the company is a loss company at the second or subsequent alteration time for an income year. [Schedule 1, item 18, paragraph 165-115S(4)]

1.93 The overall loss for a loss company at the alteration time is the sum of the amounts of losses taken into account when determining that the company is a loss company [Schedule 1, item 18, subsections 165-115R(5) and 165-115S(5)]. The overall loss is the maximum amount in respect of which reductions are made to prevent multiplication of the company’s losses on the disposal of inter-entity interests in the loss company.

1.94 The overall loss generally includes the amount of realised losses of the loss company at the alteration time. It also includes an amount (adjusted unrealised loss) to reflect the company’s unrealised losses at that time.

1.95 The amounts reflected in the overall loss can be multiplied on the disposal of inter-entity interests. This occurs where the market values of inter-entity interests are reduced because of the losses in the company. Disposals of these interests can effectively realise the underlying losses of the loss company.

Example 1.4

Hold Co owns all the shares in Sub Co, which it bought for $400,000. On 30 April 2000 (an alteration time) Hold Co sells the shares for their current market value, $100,000. At that date Sub Co has an unapplied net capital loss of $200,000 and an undeducted tax loss of $100,000.

Sub Co is a loss company at the alteration time. Its overall loss is $300,000.

To ensure that Sub Co’s losses are not multiplied when Hold Co sells the shares, the reduced cost bases of Hold Co’s shares are reduced by $300,000 (the overall loss in Sub Co) to $100,000. Hold Co makes no capital loss or capital gain from the shares.

1.96 Certain losses, or parts of losses, are to be disregarded when considering whether a company is a loss company, and working out the amount of the company’s overall loss. Losses are to be disregarded to the extent that they are not an outlay or loss of the economic resources of the company. [Schedule 1, item 18, subsections 165-115R(6) and 165-115S(6)]

1.97 Any part of a loss that is not an outlay or loss of the economic resources of a company does not decrease the market value of the company. An example is a tax deduction for an amount not actually expended by the company (e.g. the additional 25% tax deduction provided for certain Research and Development expenditure). Losses for tax purposes arising from such deductions cannot be multiplied when interests in the company are disposed of. It follows that they should not be included in the overall loss figure on which anti-multiplication reductions are based.

1.98 It is specifically provided that a non-economic loss will include depreciation on an item of plant to the extent that tax recognition of the outlay (via depreciation deductions) happens in advance of economic depreciation or depletion of the plant. These ‘timing differences’ for plant are to be calculated on an asset by asset basis. It is not necessary to track reversals of the difference.

1.99 Certain realised losses in a loss company’s overall loss may also be reduced if a notional revenue loss, notional capital loss or trading stock decrease in respect of an asset was taken into account in determining whether the company was a loss company at an earlier alteration time, and the realised loss reflects these amounts [Schedule 1, item 18, section 165-115T]. The realised loss is reduced by these amounts. This prevents double counting of the same underlying loss.

1.100 No reduction in the overall loss is required if the company did not have an adjusted unrealised loss at an earlier alteration time, or if a notional revenue loss, notional capital loss or trading stock decrease was disregarded at the earlier alteration time under the measures for reducing compliance costs (see paragraphs 1.108, 1.109 and 1.116).

1.101 A realised loss for this purpose is a tax or net capital loss for the income year or an earlier income year. Notional revenue losses, notional capital losses and trading stock decreases are calculated in working out any adjusted unrealised loss. (Paragraphs 1.102 to 1.116 explain ‘notional revenue loss’, ‘notional capital loss’, ‘trading stock decrease’ and ‘adjusted unrealised loss’).

Example 1.5

In the 2000-2001 income year Manufacturing Co has 2 alteration times. Two assets held by the company have unrealised losses at the first alteration time. In the period between the first and second alteration times these assets are sold. In determining Manufacturing Co’s overall loss at the second alteration time, realised losses must be reduced to take account of the notional losses for these assets which were taken into account at the earlier alteration time.

|

|

Alteration time 1

|

Alteration time 2

|

|

Asset 1

|

Notional revenue loss $300,000.

|

Realised tax loss $200,000.

|

|

Asset 2

|

Notional capital loss $400,000.

|

Realised net capital loss $500,000.

|

The realised loss ($200,000 tax loss) relating to Asset 1 is reduced to nil because it is less than the notional loss.

The realised loss on Asset 2 (that constituted the $500,000 net capital loss) is reduced by an amount equal to the notional loss ($400,000).

Example 1.6

At the first alteration time on 3 January 2001, Prosper Co has a $200,000 undeducted tax loss, which it incurred in 1998. It also has an adjusted unrealised loss of $50,000 consisting of a notional revenue loss on an asset, ‘A’, that it owns.

At this first alteration time, Prosper Co is a loss company, having an overall loss of $250,000.

Asset A increases in value and on 1 May 2001 Prosper Co sells it and incurs a loss of only $30,000.

Prosper Co has a second alteration time on 31 May 2001. It has a tax loss of $100,000 for the notional income year to 31 May 2001. The tax loss includes the $30,000 loss realised on asset A and $10,000 representing the benefit of a tax incentive.

At this second alteration time in the same income year, Prosper Co has an overall loss of $60,000. This is calculated by reducing the $100,000 tax loss by the realised loss on asset A ($30,000) and by the $10,000 tax incentive, which is not a loss of the company’s economic resources.

1.102 A notional loss is the loss on a CGT asset that a company would make if it disposed of that asset at an alteration time for its market value. It measures any unrealised fall in the value of a CGT asset that the company still owns. A notional loss can be of a revenue or capital nature. [Schedule 1, item 18, subsection 165-115V(8)]

1.103 Notional losses must be calculated to decide whether a company has an adjusted unrealised loss at an alteration time. This is taken into account in determining whether a company is a loss company and the amount of the overall loss.

1.104 The method of calculating notional losses is, for practical purposes, the same as it is in the unrealised loss provisions [Schedule 1, item 18, section 165-115F of Subdivision 165-CC]. Provision is made for the Commissioner to give guidance or provide advice about valuing assets, with the object of reducing the costs of complying with Subdivision 165-CD. Matters covered in the Commissioner’s advice could include the grouping of assets for the purpose of valuation [Schedule 1, item 18, subsection 165-115V(8)].

1.105 A different way of calculating an ‘unrealised loss’ on an item of trading stock is required because of the tax accounting used for trading stock generally.

1.152 A trading stock decrease is the extent to which (if any) the market value of an item immediately before an alteration time is less than

• its value (under subsection 70-40(1)) at the start of the income year in which the alteration time occurred; or,

• its cost of acquisition if the item was acquired during the income year.

1.107 If there was an earlier alteration time (or earlier alteration times) in that year, the trading stock decrease is the extent to which (if any) the market value of an item immediately before the alteration time is less than its market value immediately before the latest of the previous alteration times; or if the item was acquired after the latest alteration time, is less than its cost of acquisition. [Schedule 1, item 18, subsection 165-115W(1)] There is also a double counting rule so that the same trading stock decrease is not taken into account more that once.

1.108 For working out both notional losses and trading stock decreases, there are measures to reduce companies’ compliance costs. A notional loss or a trading stock decrease on a CGT asset is disregarded if the loss company acquired the CGT asset for less than $10,000. [Schedule 1, item 18, sections 165-115V(2) and 165-115W(2)]

1.109 A further saving on valuation costs is available on items of plant (not including a building or structure) costing $10,000 or more, but less than $1 million, for which the loss company can claim deductions for depreciation. Providing the loss company can reasonably conclude that the market value of the item of plant would not be less than 80% of its written down value for tax purposes at the alteration time, the company may use the written down value to calculate any notional loss for that plant. [Schedule 1, item 18, subsections 165-115V(6) and (7)]

1.110 In broad terms, the adjusted unrealised loss is the sum of the notional losses on a loss company’s CGT assets (other than trading stock) and any decreases in value of items of the loss company’s trading stock [Schedule 1, item 18, subsection 165-115U(1)]. If unrealised losses and trading stock decreases were not recognised as part of a loss company’s overall loss, loss multiplication could occur to the extent of these losses when inter-entity interests in the company are realised.

1.111 The method statement [Schedule 1, item 18, section 165-115U] for working out whether a loss company has an adjusted unrealised loss at an alteration time adopts a different treatment of trading stock from the corresponding method statement in the unrealised loss measures [Section 165-115E of Subdivision 165-CC]. This is because the method used in the unrealised loss measures does not give appropriate results where more than one alteration time occurs. A different methodology is adopted generally to measure decreases in the value of trading stock for calculating an adjusted unrealised loss for a company.

1.112 To calculate the adjusted unrealised loss the company must first work out the notional revenue loss or notional capital loss (if any) on each CGT asset, other than trading stock, owned at the alteration time. To the extent that this reflects an amount already taken into account at an earlier alteration time, it is not counted again.

1.113 The company must also work out, in respect of each CGT asset that is trading stock of the company, any decrease in value of the asset since the start of the income year in which the alteration time occurs, or since the date of its acquisition if later; or in the case of a second or subsequent alteration time in the same year, any decrease in value of the asset since the previous alteration time, or since the date of its acquisition if later. [Schedule 1, item 18, subsection 165-115U(1), step 1]

1.114 The sum of the company’s notional revenue losses and notional capital losses is its nominal unrealised loss at that alteration time. [Schedule 1, item 18, subsection 165-115U(1), step 2]

1.115 The sum of the decreases in value of items of the company’s trading stock is the loss company’s overall trading stock decrease. The sum of the nominal unrealised loss (if any) and the overall trading stock decrease (if any) is the company’s adjusted unrealised loss at the relevant alteration time. [Schedule 1, item 18, subsection 165-115U(1), steps 3 and 4]

Example 1.7

Mineral Co had alteration times in each of three consecutive income years. During these years Mineral Co held a number of CGT assets. Unrealised losses on assets 1 and 2 are determined under the CGT provisions while asset 3 is subject to the revenue provisions.

Mineral Co needs to work out its adjusted unrealised loss at each of the alteration times. The assets had the following attributes at the alteration times.

[CB = cost base; RCB = reduced cost base; MV = market value]

|

|

1st alteration time

|

2nd alteration time

|

3rd alteration time

|

|---|---|---|---|

|

Asset 1 (CGT only)

|

CB/RCB: $300,000

MV: $200,000

|

CB/RCB: $300,000

MV: $100,000

|

CB/RCB: $300,000

MV: $20,000

|

|

Asset 2 (CGT only)

|

CB/RCB: $600,000

MV: $550,000

|

CB/RCB: $600,000

MV: $700,000

|

CB/RCB:$600,000

MV: $500,000

|

|

Asset 3

(Revenue asset)

|

Cost: $1,000,000

MV: $980,000

|

Cost: $1,000,000

MV: $980,000

|

Cost: $1,000,000

MV: $1,050,000

|

|

Trading stock item 1

|

Opening value:

$900,000

MV: $500,000

|

Opening value (based on previous closing value):

$500,000

MV: $300,000

|

Opening value (based on previous closing value):

$300,000

MV: $150,000

|

|

Trading stock item 2

|

Opening value:

$1,500,000

MV: $1,000,000

|

Opening value (based on previous closing value):

$1,500,000

MV: $1,200,000

|

Opening value (based on previous closing value):

$1,500,000

MV: $500,000

|

|

Trading stock item 3

|

Opening value:

$600,000

MV: $800,000

|

Opening value (based on previous closing value):

$600,000

MV: $550,000

|

Opening value (based on previous closing value):

$600,000

MV: $400,000

|

Sections 165-115U, 165-115V and 165-115W would apply in the following way to determine Mineral Co’s adjusted unrealised loss at each of the alteration times.

|

|

1st alteration time

|

2nd alteration time

|

3rd alteration time

|

|

Asset 1 (CGT only)

|

Notional capital loss: $100,000

|

Notional capital loss: $100,000

($200,000 – $100,000)

|

Notional capital loss: $80,000

($280,000 –$200,000)

|

|

Asset 2 (CGT only)

|

Notional capital loss: $50,000

|

No notional capital loss.

|

Notional capital loss: $50,000

($100,000 – $50,000)

|

|

Asset 3

(Revenue asset)

|

Notional revenue loss: $20,000

|

No notional revenue loss.

|

No notional revenue loss.

|

|

Trading stock item 1

|

Trading stock decrease:

$400,000

|

Trading stock decrease:

$200,000

|

Trading stock decrease:

$150,000

|

|

Trading stock item 2

|

Trading stock decrease:

$500,000

|

No trading stock decrease: nil

($300,000 – $500,000)

|

Trading stock decrease:

$500,000

($1,000,000 – $500,000)

|

|

Trading stock item 3

|

No trading stock decrease.

|

Trading stock decrease: $50,000

|

Trading stock decrease:

$150,000

($200,000 –$50,000)

|

|

|

1st alteration time

|

2nd alteration time

|

3rd alteration time

|

|

Nominal unrealised loss

|

$170,000

|

$100,000

|

$130,000

|

|

Overall trading stock decrease

|

$900,000

|

$250,000

|

$800,000

|

|

Adjusted unrealised loss

|

$1,070,000

|

$350,000

|

$930,000

|

1.116 A loss company is taken not to have an adjusted unrealised loss if it meets the maximum net asset value test (section 152-15); that is, if the net value of its CGT assets, together with the net value of the CGT assets of any connected entities, is $5 million or less. For this purpose the Subdivision adopts the meaning of ‘connected entity’ used in section 152-30 (in the CGT small business relief provisions). For entities with net assets less than this threshold, any reductions are based on the loss company’s realised losses only. [Schedule 1, item 18, subsection 165-115U(2)]

1.117 Reductions are made under Subdivision 165-CD to the values for tax purposes of interests that are part of a relevant equity interest or a relevant debt interest in the loss company.

1.118 In broad terms a relevant equity or debt interest is present where an entity or an entity and its associates have a controlling stake in the loss company and the entity has a minimum equity or debt interest in the loss company. [Schedule 1, item 18, sections 165-115X and 165-115Y]

1.119 Adopting a test which requires an entity to have not only a minimum interest but also a controlling stake ensures that the entity will not have to adjust an interest in a loss company which the entity or the entity and its associates do not control.

1.120 In the Treasurer’s Press Release No. 74 (Attachment E) of 11 November 1999 it was announced that the inter-entity measures would apply to equity interests of at least 10% in the loss company and to all debt interests in the loss company.

1.121 Significant concerns were raised about this approach. Compliance costs and other difficulties associated with the proposal were put forward. The position of entities with minority interests in the loss company was of particular concern. Many such entities may have limited access to information relevant to the application of these measures. This could put them at a disadvantage compared to majority holders.

1.122 As a result of these concerns the measures now apply as described above. The significant change is that an entity must have a controlling stake in the loss company before reductions can be made to the tax values of its interests in the company. This overcomes many of the concerns raised.

1.123 The test for a ‘controlling stake’ in a company is based on the ‘linked group’ test found in section 170-260 of Subdivision 170-D. An entity will have a controlling stake in a loss company if the entity or the entity and its associates have a greater than 50% stake in the voting power, rights to dividends, or rights to distributions of capital of the loss company. Control can be direct or indirect through one or more interposed entities. [Schedule 1, item 18, subsection 165-115Z(1)]

1.124 If an entity has a controlling stake in a loss company in its own right, associates of that entity will also have a controlling stake in the loss company irrespective of whether they independently have such a stake.

1.125 ‘Associate’ is defined in section 318 of the ITAA 1936. An individual may be an associate in applying the controlling stake test, although the interests of individuals are not adjusted under this Subdivision.

1.126 To prevent double counting, where an entity has an indirect interest in the loss company through an associate which has a direct interest, only the direct interests are to be counted. [Schedule 1, item 18, subsection 165-115Z(2)]

Example 1.8

Company A and its associate Company B have a 70% controlling stake in Company C. Company A has both a direct and an indirect interest in Company C.

To prevent double counting interests in Company C only direct interests are counted. Company A’s indirect interest in Company C, through its shareholding in Company B, is disregarded.

1.127 An entity will have a relevant equity interest at a time if the entity has at that time:

• a controlling stake in a loss company; and

• equity that gives (directly, or indirectly through one or more interposed entities):

− control of, or the ability to control 10% or more of the voting power in the loss company; or

− the right to receive 10% or more either of any dividends or of any distributions of capital that the loss company may pay.

[Schedule 1, item 18, paragraphs 165-115X(1)(a) and (b)]

1.128 The equity must be either:

• an interest in the loss company, including a share or shares, or an option or right to acquire a share or shares, in the loss company, or

• an interest, including an option or right to acquire an interest, in another entity which has a relevant equity interest or relevant debt interest in the loss company.

[Schedule 1, item 18, paragraph 165-115X(1)(c)]

1.129 Subdivision 165-CD is intended to apply to both direct and indirect equity interests in the loss company. An equity interest for these purposes includes membership interests in entities (e.g. shares or units or interests in fixed trusts) and is extended to include options or rights to acquire such interests.

1.130 The entity’s relevant equity interest in the loss company at a particular time is made up of this equity or equities. [Schedule 1, item 18, subsection 165-115X(2)]

1.131 A special rule exists to allow the relevant equity interests of some entities (‘the subject entity’) to be taken not to be relevant equity interests [Schedule 1, item 18, subsection 165-115X(3)]. Certain trusts and superannuation funds will be covered by this rule.

1.132 The exception will apply where, at the relevant time, no entity (including an individual) with an interest held directly or indirectly in a potentially affected entity could obtain a capital loss or deduction reflecting any part of the loss company’s overall loss, and no entity (whether still holding an interest in the potentially affected entity or not at the relevant time), has obtained or becomes entitled to such a capital loss or deduction in respect of an interest in the entity. [Schedule 1, item 18, section 165-115X(3) and (4)]

1.133 If the potentially affected entity can show that no one has obtained or become entitled to a capital loss or deduction that reflects any part of the loss company’s overall loss, and no one could make a capital loss or deduction at a later time that reflects it, then that entity will not have a relevant equity interest.

1.134 In relation to the obtaining of a capital loss or a deduction at a later time, it will be enough if the potentially affected entity can show that, for example, the market values of the interests unrealised immediately before the relevant time have never been impacted by the company’s losses. For example, a fully secured bank loan owed by the entity, with a market value not less than its face value at the relevant time, may be shown not to have been affected by a company’s losses.

1.135 Most potentially affected entities would find it difficult to show that no interest held directly or indirectly in them (at any time) has duplicated, or is capable of duplicating, at any time, the company’s losses. However, it is expected that this would be feasible for solvent superannuation funds and non-fixed trusts, and for similar entities without realisable fixed interests.

1.136 A relevant debt interest exists at a time if an entity has a controlling stake in the loss company and the entity:

• is owed a debt of $10,000 or more, or a number of debts some of which are $10,000 or more by the loss company; or

• is owed a debt of $10,000 or more, or a number of debts some of which are $10,000 or more by a debtor entity (not the loss company), and the debtor entity has a relevant equity or debt interest in the loss company.

[Schedule 1, item 18, subsections 165-115Y(1) and 165-115Y(2)]

1.137 The total of the debt or debts of $10,000 or more makes up the entity’s relevant debt interest in the loss company. [Schedule 1, item 18, subsection 165-115Y(3)]

1.138 A special rule also exists to allow the relevant debt interests in a loss company held by certain entities to be taken not to be relevant debt interests [Schedule 1, item 18, subsection 165-115Y(4)and (5)]. The rule operates in the same way as it does for relevant equity interests (see paragraphs 1.131 to 1.135).

Example 1.9

Company A owns 60% of Company D (a loss company). Company A also owns 20% of Company B and 80% of Company C. Company C has a $20,000 loan outstanding to Company B and Company D has a $20,000 loan outstanding to Company C. Company B is not an associate of Company A or Company C.

Company A’s shares in Company D are part of a relevant equity interest. This is because Company A has a controlling stake in Company D and the right to more than 10% of any dividends or distributions of capital from Company D.

Company C’s loan of $20,000 to Company D is a relevant debt interest. This is because the debt is greater than $10,000 and Company C has a controlling stake in Company D (because it is an associate of Company A).

Company B does not have a relevant equity or debt interest in Company D. It does not have a controlling stake in Company D (not being an associate of Company A or Company C).

Company A’s shares in Company C are part of a relevant equity interest. This is because Company A has a controlling stake in Company D and the right to more than 10% of any dividends or distributions of capital by Company D. Company A also has a direct interest in Company C which has a relevant debt interest in Company D.

1.139 Having determined that an affected entity has a relevant equity interest or relevant debt interest (or both) in a loss company that has had an alteration, it is necessary to determine what reductions to the values for tax purposes of those interests are appropriate to prevent loss multiplication.

1.140 What kinds of reductions are required, and when they are required, is set out in one section [Schedule 1, item 18, section 165-115ZA]. The methods for calculating the actual reduction amounts are set out in the following section [Schedule 1, item 18, section 165-115ZB].

1.141 Reductions are to be made to:

• the reduced cost bases of equity or debt acquired after 19 September 1985 [Schedule 1, item 18, subsection 165-115ZA(3)];

• deductions the entity is entitled to in respect of the disposal of equity or debt which is not trading stock of the entity [Schedule 1, item 18, subsection 165-115ZB(4)].