Commonwealth of Australia Explanatory Memoranda Commonwealth of Australia Explanatory Memoranda

Commonwealth of Australia Explanatory Memoranda Commonwealth of Australia Explanatory Memoranda[Index] [Search] [Download] [Bill] [Help]

2002

THE PARLIAMENT OF THE COMMONWEALTH OF AUSTRALIA

HOUSE OF REPRESENTATIVES

NEW BUSINESS TAX SYSTEM (CONSOLIDATION, VALUE SHIFTING, DEMERGERS AND OTHER MEASURES) BILL 2002

EXPLANATORY MEMORANDUM

(Circulated by authority of the

Treasurer, the Hon Peter

Costello, MP)

Table of contents

The following abbreviations and acronyms are used throughout this explanatory memorandum.

|

Abbreviation

|

Definition

|

|---|---|

|

A Platform for Consultation

|

Review of Business Taxation: A Platform for Consultation

|

|

A Tax System Redesigned

|

Review of Business Taxation: A Tax System Redesigned

|

|

ATO

|

Australian Taxation Office

|

|

AVM

|

adjustable value method

|

|

CFC

|

controlled foreign company

|

|

CGT

|

capital gains tax

|

|

Commissioner

|

Commissioner of Taxation

|

|

Consolidation Bill

|

New Business Tax System (Consolidation) Bill (No. 1) 2002

|

|

DVS

|

direct value shifting

|

|

FDT

|

franking deficit tax

|

|

FIF

|

foreign investment fund

|

|

FLP

|

foreign life assurance policy

|

|

GST

|

goods and services tax

|

|

GVSR

|

general value shifting regime

|

|

Imputation Bill

|

New Business Tax System (Imputation) Bill 2002

|

|

IT(TP) Act 1997

|

Income Tax (Transitional Provisions) Act 1997

|

|

ITAA 1936

|

Income Tax Assessment Act 1936

|

|

ITAA 1997

|

Income Tax Assessment Act 1997

|

|

IVS

|

indirect value shifting

|

|

MEC

|

multiple entry consolidated

|

|

SAP

|

substituted accounting period

|

|

STS

|

simplified tax system

|

|

TAA 1953

|

Taxation Administration Act 1953

|

General outline and financial impact

The consolidation measure represents a significant change to the taxation of corporate groups. Due to its magnitude, the measure is being enacted progressively via a series of bills. Schedule 1 of the Consolidation Bill introduced on 16 May 2002 contained most of the key elements of the measure. Those key elements are supplemented by the amendments to the consolidation measure contained in this bill which include:

• transitional cost setting rules for the first years of the measure;

• modifications to the general cost setting rules where an existing group forms a consolidated group;

• the treatment of attribution accounts held in relation to interests in foreign entities;

• the transfer and pooling of foreign tax credits; and

• a number of technical amendments and refinements to the Consolidation Bill introduced on 16 May 2002 to address issues raised through consultation.

Date of effect: The consolidation measure will allow wholly-owned entity groups to choose to consolidate under this regime from 1 July 2002. The existing grouping provisions will continue to operate in parallel with the consolidation regime until 1 July 2003, subject to special rules applying to consolidated groups with a head company that has a SAP. In general, such SAP groups will retain access to grouping provisions until the date of consolidation, provided that the head company chooses to consolidate from the first day of their next income year, commencing after 1 July 2003.

Proposal announced: The proposals were announced in Treasurer’s Press Release No. 58 of 21 September 1999. The consolidation elements in this bill were foreshadowed in Minister for Revenue and Assistant Treasurer’s Press Release No. C59/02 of 16 May 2002.

Financial impact: The consolidation measure is expected to cost approximately $1 billion over the forward estimate period as follows:

|

2001-2002

|

2002-2003

|

2003-2004

|

2004-2005

|

2005-2006

|

|

nil

|

$180 million

|

$370 million

|

$335 million

|

$280 million

|

Further explanation of this impact was provided in the explanatory memorandum to the Consolidation Bill introduced on 16 May 2002.

Compliance cost impact: The amendments in this bill are integral to the consolidation measure which is expected to reduce ongoing compliance costs by ensuring that:

• intra-group transactions are ignored for taxation purposes, so that taxation and accounting treatments are more closely aligned;

• administrative requirements, such as multiple tax returns and multiple franking account, losses, foreign tax credit and PAYG obligations are reduced; and

• integrity measures aimed at preventing loss duplication, value shifting or the avoidance or deferral of capital gains within groups do not apply within a consolidated group.

The consolidation regime will necessitate some initial up-front costs for groups as they familiarise themselves with the new law, update software and notify the ATO of a choice to consolidate. Large corporate groups may incur greater start-up costs in determining the market values of group assets. These costs will be alleviated by a transitional measure under which the group can elect (prior to 1 July 2003) to bring assets into the group at their existing cost bases. Groups that form after the transitional period may use the market value guidelines developed by the ATO to minimise compliance costs.

Impact: Medium to high.

Main points:

• The consolidation provisions included in this bill supplement those contained in the Consolidation Bill introduced on 16 May 2002. Further provisions are scheduled for introduction later this year.

• The impacts of the consolidation measure, which will allow wholly-owned entity groups to choose to consolidate from 1 July 2002, were fully explained in Chapter 14 of the explanatory memorandum to the Consolidation Bill introduced on 16 May 2002.

This bill also provides consequential amendments to the provisions currently referred to in the taxation laws as the ‘exempting and former exempting company provisions’. The Imputation Bill introduced into Parliament core rules for the new simplified imputation system. As a result of the introduction of that bill, certain consequential amendments are required to other areas of the imputation system not covered by those rules, including the exempting and former exempting company provisions. This bill makes those amendments.

Date of effect: Broadly speaking, the measure applies from 1 July 2002.

Proposal announced: The amendments are consequential to the Government’s decision to implement the simplified dividend imputation proposal. This proposal was announced in Treasurer’s Press Release No. 58 of 21 September 1999 as a component of the unified entity regime. On 14 May 2002, the Minister for Revenue and Assistant Treasurer announced in Press Release No. C57/02, the Government’s program for delivering the next stage of business tax reform measures. In that press release, the Minister confirmed that the simplified imputation system will commence on 1 July 2002.

Financial impact: The new imputation system will have no revenue impact.

Compliance cost impact: The new imputation system is designed to reduce compliance costs incurred by business by providing for simpler processes and increased flexibility.

This bill introduces a general value shifting regime (GVSR). The regime applies mainly to interests in companies and trusts that are not consolidated, but meet control or common ownership tests. The GVSR replaces the share value shifting and asset stripping rules currently in the income tax law.

Entities dealing at arm’s length or on market value terms are generally excluded from the GVSR.

This bill also makes amendments to the loss integrity measure to allow the optional use of global asset valuations for calculating unrealised gains and unrealised losses in Subdivisions 165-CC and 165-CD.

A special value shifting rule is introduced into Subdivision 165-CD to maintain its integrity where global valuations are used.

Date of effect: The GVSR applies to value shifts that happen on or after 1 July 2002, unless they happen under an arrangement or scheme entered into before 27 June 2002.

The loss integrity change to allow global asset valuation applies to calculations for changeover times and alteration times from 11 November 1999. The global valuation approach is optional and will not disadvantage taxpayers in terms of the current law. A transitional rule will ensure that the new value shifting rule in Subdivision 165-CD cannot disadvantage taxpayers in respect of alteration times that happen before Royal Assent.

Proposal announced: The GVSR proposal was announced in Treasurer’s Press Release No. 58 of 21 September 1999 (Attachment K), with further details announced in Treasurer’s Press Release No. 16 of 22 March 2001. The proposal in this bill was further foreshadowed in the Minister for Revenue and Assistant Treasurer’s Press Release No. C57/02 of 14 May 2002.

The loss integrity change to allow global asset valuation has not been previously announced.

Financial impact: The gain to revenue for the GVSR is estimated to be:

|

2002-2003

|

2003-2004

|

2004-2005

|

2005-2006

|

|

nil

|

$150 million

|

$160 million

|

$170 million

|

The loss integrity change to allow global asset valuation is not expected to have any significant impact on revenue.

Compliance cost impact: A small to moderate increase in compliance costs for the GVSR is expected for most taxpayers affected by the measure, at least initially. In general, the de minimis rules and safe-harbours will assist in keeping compliance costs down.

In some instances the low value transaction exclusions and safe-harbours in the new law will mean a reduction in compliance costs for some taxpayers as compared with the existing law. Also, those entities that consolidate will not be subject to the GVSR.

In particular cases, the loss integrity changes to allow global asset valuation are expected to result in a significant reduction in compliance costs.

Impact: The GVSR implements a generalised regime to replace the current value shifting rules which are deficient in many respects. The GVSR will apply to a wider range of entities, as well as to a wider range of transactions. In some instances the exclusions for low value transactions and safe-harbours will mean that taxpayers affected by the current rules will not be affected by the GVSR.

The loss integrity change to allow global asset valuation is expected to have a significant impact in reducing compliance costs in particular cases as the savings in valuation costs if assets are valued together rather than individually. The special value shifting rule required to preserve the integrity of Subdivision 165-CD may result in a small increase in compliance costs. This is because of the need to identify the removal of value from the company by particular means (e.g. certain distributions or transfers of assets to associates at undervalue). The net reduction in compliance costs is expected to be significant. The global valuation approach will also assist cost setting under the consolidation rules where affected entities have been subject to the loss integrity measures.

Main points:

There are taxpayers not subject to the current value shifting rules that will be subject to the GVSR:

• Controllers and associates that hold equity or loan interests in controlled trusts will be subject to the direct value shifting rules – however the ‘interests’ of mere objects in discretionary trusts are not subject to value shifting adjustments.

• Controllers and associates that hold equity or loan interests in controlled companies or trusts that are not covered by the asset stripping rules in the current law.

• Common owners that hold interests in closely-held companies or trusts that satisfy common ownership tests with other closely held companies or trusts.

• In some cases involving closely-held entities, persons with interests in entities who do not form part of a control or common ownership framework that actively participate in a value shifting scheme.

• Taxpayers who create rights over assets at less than market value in favour of their associates, and then sell the assets (or replacement assets) at reduced values for losses.

Taxpayers affected by the rules will need to make appropriate adjustments to account for the effect of value shifting transactions on the values of their assets to ensure that inappropriate gains and losses do not arise on the realisation of those assets. There may be some changes in the behaviour of entities subject to the GVSR who may choose to deal at arm’s length, at market value, or within safe-harbours provided, to avoid the need to make adjustments.

Some taxpayers affected by the current value shifting rules will not be subject to the GVSR:

• Interest holders affected by an indirect value shift that can satisfy the CGT small business taxpayer $5 million net asset test or that are eligible to participate in the STS.

• Entities with interests in consolidated group members whose values for tax purposes are reconstructed under consolidation rules.

• No adjustments will be required for interest holders affected by small value shifts.

• On a practical level, many of the new rules are loss-focused and adjustments will only be required if an interest is realised at a loss.

• A choice will be available to use global asset valuations for calculating unrealised losses in Subdivision 165-CD. This will enable compliance costs, especially valuation costs, to be lowered in circumstances where individual asset valuations are difficult or costly to perform. The approach will be optional and individual asset valuations may continue to be done if required.

• The choice will be available for alteration times happening from 11 November 1999, thereby allowing maximum compliance cost savings vis-à-vis the individual asset approach contained in the current law.

• A specific value shifting rule will, on an ongoing basis, preserve the integrity of Subdivision 165-CD even though some unrealised gain in value may be included in a global asset valuation at an alteration time. There will be some compliance costs involved in determining whether an adjustment is required if an interest in the company is later sold at a loss. However, in net terms, the reduction in valuation is expected to exceed by a considerable margin, in most cases, any additional costs of the value shifting rule.

• The value shifting rule will have a transitional application for alteration times that happen before this bill receives Royal Assent. Broadly, there will be no requirement specifically to examine whether value has been removed from the company after the alteration time. Any method by which a reasonable conclusion may be drawn that the later realised loss on the interest does not, or could not, duplicate an unrealised loss on an asset at the alteration time, will be sufficient to avoid an adjustment.

Schedule 16 to this bill inserts into the ITAA 1997 and the ITAA 1936:

• a CGT roll-over and a dividend exemption for owners in the head entity of a demerger group; and

• a CGT exemption for the members of a demerger group,

where a demerger group divests itself of at least 80% of its interests in a demerger subsidiary to the interest owners of the head entity.

Date of effect: 1 July 2002.

Proposal announced: Treasurer’s Press Release No. 16 of 22 March 2001. Further details were announced in Minister for Revenue and Assistant Treasurer’s Press Release No. C40/02 of 6 May 2002.

Financial impact: Unquantifiable. Details of the financial impacts are included in the table (under Revenue costs) in the regulation impact statement which appears in Chapter 16.

Compliance cost impact: Details of the compliance cost impacts are included in the regulation impact statement which appears in Chapter 16.

Amendments to this measure are required to deal with its interaction with other tax regimes and to address issues raised during consultation. These amendments are planned to be introduced at the earliest opportunity.

Impact: Low to medium.

Main points:

• The initial and ongoing compliance costs that may be incurred depend on the structure of the demerger group.

• The measure has the support of industry who have been consulted on the detail of the measure.

• The net benefit of this measure is to remove the taxation impediments to business reorganisations by way of a demerger and to ensure that the taxation consequences for owners does not unnecessarily drive the choice of structure in which business should operate.

Chapter

1

Cost

setting rules – formation and transition

1.1 This chapter explains the modifications and changes to the cost setting rules that were introduced in the Consolidation Bill introduced on 16 May 2002. Those rules were explained in Chapters 2 and 5 of the accompanying explanatory memorandum. The amendments explained in this chapter are contained in Schedules 2 to 4 and 7 to this bill.

1.2 The cost setting rules deal with the alignment of the cost of the assets of an entity that becomes a subsidiary member of a consolidated group with the group’s cost for acquiring the entity. In addition, when an entity ceases to be a subsidiary member of a consolidated group, the group is recognised as having a cost for membership interests in the subsidiary that is equal to its tax cost for the net assets of that entity.

1.3 This chapter explains the rules for:

• changes to the cost setting rules that were introduced in the Consolidation Bill introduced on 16 May 2002;

• the formation of a consolidated group; and

• transitional provisions that apply to:

− consolidated groups that form, with effect, before 1 July 2004; and

− all consolidated groups.

All references to sections and divisions are references to sections and Divisions of the ITAA 1997 unless otherwise stated.

1.4 The treatment of assets of entities joining a consolidated group is based on the asset-based model discussed in A Platform for Consultation and recommended by A Tax System Redesigned.

1.5 This model dispenses entirely with income tax recognition of separate entities within a consolidated group. It treats a consolidated group’s cost of acquiring a subsidiary entity as the cost to the group of acquiring the assets of that entity. A group’s cost of acquiring an entity includes the liabilities of the entity that become liabilities of the group. This cost also includes the liabilities that the acquired entity owes to existing members of the acquiring consolidated group.

1.6 A consolidated group’s cost for membership interests in a subsidiary member when it leaves a consolidated group is determined based on the cost to the group for the net assets of the subsidiary.

1.7 This treatment of the acquisition and disposal of subsidiary entities by a consolidated group prevents the double taxation of gains and duplication of losses arising within the group and allows for assets to be transferred between members of the group without requiring cost base adjustments to address value shifting.

1.8 On formation of a consolidated group it is recognised that modifications are required to the rules for the basic case of a single entity joining an existing consolidated group. These modifications take into account that there may be more than one entity becoming a subsidiary member at the same time.

1.9 The asset-based model discussed in A Platform for Consultation and recommended by A Tax System Redesigned also recognised the need for special rules to apply on transition to the consolidation rules. In particular, a transitional option should be available for a group consolidating during the transitional period to elect in relation to certain subsidiary members to retain the existing asset tax costs (rather than applying the cost setting rules). This transitional option thereby removes the need for consolidated groups to re-value assets as required under the ongoing tax cost setting rules.

1.10 Transitional rules are also required to ensure that the transitional provisions of the uniform capital allowance system continue to apply to consolidated groups.

1.11 The new law explained in this chapter is discussed under the following topics:

• changes to the cost setting rules that were introduced in the Consolidation Bill introduced on 16 May 2002; and

• rules for the formation of a consolidated group; and

• transitional provisions that apply to:

− consolidated groups that form, with effect, before 1 July 2004; and

− all consolidated groups.

1.12 The changes to the cost setting rules in the Consolidation Bill introduced on 16 May 2002 relate to technical refinements and enhancements to the core rules (relating to cost setting), rules for a single entity joining and rules for an entity leaving a consolidated group.

1.13 The formation rules operate by modifying the basic case of a single entity joining a consolidated group. In general, when a consolidated group is formed, no changes are made in relation to the assets of the head company of the group. Intra-group debt and intra-group membership interests held by the head company are exceptions. These are not recognised for income tax purposes after the group is formed.

1.14 The transitional provisions are primarily required in order to reduce the compliance costs associated with forming a consolidated group.

1.15 Division 701 of the IT(TP) Act 1997 provides for a modified application of the ITAA 1997 for certain consolidated groups formed in the 2002-2003 and 2003-2004 financial years. Where a consolidated group is formed, with effect, before 1 July 2004, the head company may choose that assets of certain subsidiary members retain their ‘costs’ for tax purposes (e.g. adjustable values). This choice enables existing groups to consolidate without valuing the assets of, or calculating allocable cost amounts for, subsidiary members. There are also transitional provisions that apply to groups formed within the transitional period where they do not elect to retain their existing tax costs.

1.16 Division 702 of the IT(TP) Act 1997 provides for a modified application of the other transitional provisions (e.g. capital allowance provisions) in relation to assets that an entity brings into a consolidated group. These rules ensure that the transitional provisions of the uniform capital allowances system continue to apply to consolidated groups.

|

New law

|

Current law

|

|---|---|

|

Technical corrections and refinements are made to the rules contained in

the Consolidation Bill introduced on 16 May 2002

|

The Consolidation Bill introduced on 16 May 2002 contains the cost setting

rules for a single entity joining and leaving a consolidated group.

|

|

Rules for formation enable groups to apply the cost setting rules when

forming a consolidated group.

|

The cost setting rules contained in the Consolidation Bill introduced on

16 May 2002 did not contain rules for group formation.

|

|

Transitional rules reduce the compliance costs associated with forming a

consolidated group.

|

The cost setting rules contained in the Consolidation Bill introduced on

16 May 2002 did not provide for the transitional operation of the

rules.

|

1.17 The new law explained in this chapter is discussed under the following topics:

• changes to the cost setting rules that were introduced in the Consolidation Bill introduced on 16 May 2002 (see paragraphs 1.18 to 1.47);

• rules for the formation of a consolidated group (see paragraphs 1.48 to 1.74); and

• transitional provisions that apply to:

− consolidated groups that form, with effect, before 1 July 2004 (see paragraphs 1.77 to 1.114); and

− all consolidated groups (see paragraphs 1.115 to 1.117).

1.18 The changes to the cost setting rules in the Consolidation Bill introduced on 16 May 2002 relate to amendments to the following areas:

• core rules contained in Division 701 (see paragraphs 1.19 to 1.26);

• rules dealing with an entity joining an existing consolidated group contained in Subdivision 705-A (see paragraphs 1.27 to 1.45); and

• rules dealing with entities leaving a consolidated group contained in Division 711 (see paragraphs 1.46 to 1.47).

1.19 The reference in the heading for subsections 701-25(4) and 701-35(4) is amended so that it more correctly refers to value of trading stock rather than the cost of trading stock. [Schedule 2, notes to items 1 and 2]

1.20 The cost setting rules provide that where assets of an entity that becomes a subsidiary member of a consolidated group constitutes trading stock the entity is taken to have disposed of the closing trading stock for a specified value in order for there to be neither a gain nor a loss in respect of the closing trading stock in the tax return for the joining entity in the period ending at the joining time. Similarly where an entity leaves a consolidated group and takes with it trading stock the head company is taken to have disposed of the trading stock for a tax-neutral value. As a consequence the joining entity and head company are not able to utilise the choice that is generally available to an entity to revalue its trading stock at the end of an income year under section 70-45. [Schedule 2, items 1 and 3, notes to subsections 701-25(4) and 701–35(4)]

1.21 To allow an entity to revalue its trading stock immediately prior to joining a consolidated group would be inappropriate where the cost of trading stock is reset on entry into the consolidated group. However, where a transitional consolidated group elects to retain the existing costs of assets for tax purposes this option would be available (see paragraph 1.88). The exit of an entity from a consolidated group (as distinct from the disposal of membership interests in a leaving entity) should also result in a tax-neutral consequence for the head company of the consolidated group.

1.22 The rule for adjustments to taxable income where identities of parties to an arrangement merge on an entity becoming a subsidiary member of a consolidated group (section 701-70) is amended to ensure that the adjustment to the taxable income of the head company is made in the same income year as the adjustment to the taxable income of the entity. This ensures that there is symmetry as to the timing of the adjustments. [Schedule 2, item 5, paragraph 701-70(3)(a)]

1.23 The rules for adjustments to taxable income where identities of parties to an arrangement merge (or re-emerge) on joining (or leaving) a group (sections 701-70 and 701-75) are amended to ensure that where they apply in respect of part year periods the operation is consistent with the part-year rule in section 701-30. Section 701-30 provides that where an entity is not a subsidiary member of a consolidated group for the whole of an income year for the period that it is not a subsidiary member its taxable income for the period is worked out as if the start and end of the period were the start and end of an income year.

1.24 The amendments to sections 701-70 and 701-75 ensure that the rules which apply in respect of the end of an income year (or start of an income year) also apply in the same way to an income year that is taken to end (or start) as a consequence of an entity not being a subsidiary member of a consolidated group for the whole of an income year. [Schedule 2, items 5 to 11]

1.25 A minor amendment is made to subsection 701-55(6) to ensure that it relates to where a provision is to apply in relation to an asset. [Schedule 2, item 4, subsection 701-55(6)]

1.26 An amendment is also made to subsection 701-35(4) to ensure that the reference to the end of the income year is expanded to also cover where the income year is taken to end as a consequence of an entity not being a subsidiary member of a consolidated group for the whole of an income year. [Schedule 2, item 2, subsection 701-35(4)]

1.27 References to depreciating assets in the cost setting rules applying where an entity becomes a member of a consolidated group are amended to ensure that those provisions only apply to depreciating assets to which Division 40 applies. Consequently, the cost setting rules which provide for a specific outcome in respect of depreciating assets will not apply where the depreciating asset is one which is excluded from the operation of Division 40. Section 40-45 provides that Division 40 does not apply to capital works, certain indefeasible rights to use international telecommunications cables and films. [Schedule 2, items 12 to 14 and 17]

1.28 As discussed in paragraph 9.22, the definition of ‘revenue asset’ is amended as part of the proposals for the general value-shifting regime. Under the new definition, an asset is a revenue asset if:

• the profit or loss arising when an entity disposes of, ceases to own, or otherwise realises the asset would be taken into account in calculating the entity’s assessable income or tax loss, otherwise than as a capital gain or capital loss; and

• the asset is neither trading stock nor a depreciating asset.

[Schedule 15, item 19, section 977-50]

1.29 As a consequence, the tax cost setting limit rule in section 705-40 is amended by adopting the new definition, but adding trading stock and depreciating assets, so as to preserve the class of assets presently covered by that rule. Under the rule, the assets affected by the tax cost setting amount limit are therefore:

• trading stock;

• depreciating assets; and

• revenue assets.

[Schedule 4, item 1, subsection 705-40(1)]

1.30 Consequential changes ensure that any reduction in the tax cost setting amount arising because of an application of the limit rule is allocated appropriately across the other reset cost base assets, including other trading stock, depreciating assets and revenue assets. [Schedule 4, item 1, subsections 705-40(2) and (3)]

1.31 An amendment is made to the rule for reducing the cost for tax purposes of over depreciated assets (section 705-50) so that subsection 705-50(2) does not apply in relation to an entity that becomes a subsidiary member and was previously a subsidiary member of a consolidated group where subsection 705–50(5) applies. This amendment ensures that section 705–50 only applies in relation to an entity that becomes a subsidiary member and was previously a subsidiary member of a consolidated group where the special rule in subsection 705-50(5) applies. [Schedule 2, item 15, paragraph 705-50(2)(a)]

1.32 The operation of section 705–50 is also modified to prevent a duplicated reduction to a joined consolidated group’s cost for its assets because of an unfranked dividend paid by a joining entity to a member of the joined group before the joining time. This could arise because the same unfranked dividend could cause a reduction to the allocable cost amount under step 4 in working out the allocable cost amount and a reduction in the amount allocated to the cost of an over-depreciated asset. [Schedule 2, item 16, paragraph 705-50(3)(a)]

1.33 Amendments are made to section 705-65 (dealing with costs of membership interests – step 1 in working out the allocable cost amount) to ensure that the provision appropriately interacts with Subdivision 165-CD which deals with adjustments for certain equity and debt interests in a loss company where there has been an alteration in ownership or control of the company.

1.34 Subsection 705-65(3) is modified to ensure that it does not have the unintended effect of triggering an alteration time (i.e. change of ownership and control) for the purposes of Subdivision 165-CD. It will also ensure it does not inadvertently trigger a changeover time for Subdivision 165-CC. This is achieved by referring to a CGT event rather than a disposal. The reference to a CGT event is sufficient to trigger the outstanding CGT adjustments. [Schedule 2, item 18, subsection 705-65(3)]

1.35 As discussed in paragraph 13.56, section 165-115ZD or section 165-115ZD of the IT(TP) Act 1997 may result in an adjustment (or further adjustment) to the reduced cost base for a membership interest that is realised at a loss after the global method has been used. Subsection 705-65(3A) requires that in relation to the joining time there be a testing in terms of section 165-115ZD on the assumption that:

• just before the joining time, a membership interest in the entity becoming a subsidiary member was disposed of; and

• members of the consolidated group received consideration equal to the market value of the membership interest at that time.

1.36 Where an adjustment would have been made as a result of section 165-115ZD applying on those assumptions (the adjustments would have been made under section 165-115ZA based on amounts calculated under section 165-115ZB) then the reduced cost base of the membership interest in the entity becoming a subsidiary members is reduced by the amount of that adjustment for the purposes of working out step 1 of the allocable cost amount. This subsection is needed, in addition to subsection (3), to trigger section 165-115ZD and determine a specific amount of adjustment, without also inadvertently triggering a new alteration time. [Schedule 2, item 20, subsection 705-65(3A)]

1.37 Consequential amendments are also made to subsection 705-65(4) to ensure that where Subdivision 165-CD applied in respect of an alteration time that happened before the joining time it does not have an effect in respect of a CGT event that happens after the joining time. [Schedule 2, items 21 and 22, subsection 705-65(4)]

1.38 In order to ensure that a reduction to the reduced cost base of a membership interest that has been made under subsection 165-115ZA(3) does not double count a subtraction for an amount of loss taken into account under step 5 or step 6 of working out the allocable cost amount, subsection 705-65(5A) ensures that the reduction under Subdivision 165-CD is added back. [Schedule 2, item 23, subsection 705-65(5A)]

1.39 A similar issue arises in respect of the reduced cost bases of debts owned by members of the consolidated group that have been subject to reductions under Subdivision 165-CD in respect of losses taken into account under step 5 or step 6 of working out the allocable cost amount. Subsection 705-75(5) ensures that there is no double counting where subsection 165-115ZA(3) has applied in respect of a debt owned by members of the consolidated group. [Schedule 2, item 27, subsection 705-75(5)]

1.40 The provisions dealing with the interaction of Subdivision 165-CC and the cost setting rules (both on entry into a consolidated group and where an entity leaves) are repealed in response to concerns over the workability of the provisions. Revised rules are to be included in a later bill. [Schedule 2, items 37 to 40, 43 and 44]

1.41 An amendment is made to the operation of section 705-75 to ensure that in working out the step 2 amount of the allocable cost amount the reduction for intra-group liabilities is determined having regard to the modified operation of subsections 705–65(2) to 705-65(4) (which deal with value shifting, loss transfer, and section 165-115ZD adjustments). [Schedule 2, items 26 and 27]

1.42 In working out the amount of liabilities to be added under step 2 in working out the allocable cost amount, it is the value of the liability to the joined group and not the value of the liability to the entity becoming a subsidiary member that is the relevant amount [Schedule 2, item 25, subsection 705–70(1A)]. This ensures that the liabilities are correctly valued in working out the cost to the consolidated group of acquiring the entity.

1.43 Amendments are also made to the cost setting rules dealing with working out the allocable cost amount where membership interests are held in an entity becoming a subsidiary member prior to the time it becomes a subsidiary member. The amendments ensure that steps 3, 5, 6 and 7 in working out the allocable cost amount use the concept of accrued rather than earned, so that amounts that are taken into account are by reference to the amount accruing over a period in which membership interests are held not just when the amount is realised. The amendments to step 3 are incorporated in a revised section 705–90 (see paragraph 1.45). [Schedule 2, items 28 and 34]

1.44 In determining the amount of a profit that ‘accrued’ between 2 points in time it would not be correct to assume a constant rate of appreciation of an asset through time where there are grounds for believing that the appreciation of the asset would have departed from constancy in a specific way. For example, the entity may be aware of circumstances (e.g. a change in operations) which would lead it to conclude that a profit accrued faster over an earlier period of time than a later point in time.

1.45 The rule for adding to the allocable cost amount, the undistributed frankable profits that accrued to the joined consolidated group’s membership interests before the entity joined (step 3) has been revised to incorporate the following changes:

• the undistributed profits comprise those retained profits calculated under the accounting standards that could be recognised in the entity’s statement of financial position if that statement was prepared as at the joining time [Schedule 2, item 28, subsection 705–90(2)];

• the extent to which dividends paid out of the undistributed profits would be frankable is determined by working out the amount the entity would be able to frank after its income tax is settled in respect of all income years up to the joining time (but not any period prior to leaving another consolidated group) [Schedule 2, item 28, subsections 705–90(3) to (5)]; and

• amounts that are taken into account are by reference to the amount of undistributed profit accruing over a period in which membership interests are held not just when the amount is realised [Schedule 2, item 28, subsections 705-90(6) to (8)].

Consequential amendments are also made to provisions which refer to step 3. [Schedule 2, items 29 to 33, 35 and 36]

Example 1.1: Undistributed profit accruing to membership interests

Headco acquired 100% of the shares in Subco on 1 July 2001 for $94. Subco, at this time, held one asset with a cost base of $80 and a market value of $100. Headco paid $94 for the entity as it recognised a deferred tax liability in respect of the asset of $6.

The asset was disposed of on 1 January 2002 for $140 realising an after tax profit of $42 ($140 less $80 less tax liability of $18).

Headco and Subco form a consolidated group on 1 July 2002.

The amount of undistributed profit to be added at step 3 when working out the group’s allocable cost amount for Subco is $28 ($140 less $100 less tax liability of $12) being the amount of undistributed after tax profit that accrued to the membership interests of Headco.

1.46 An amendment is made to correct the typographical error in the general company tax rate in the formula in subsection 711-35(1). [Schedule 2, item 41, subsection 711-35(1)]

1.47 An amendment is also made to replace the incorrect reference to joined group in subsection 711-45(5) with old group. [Schedule 2, item 42, subsection 711-45(5)]

1.48 Subdivision 705-B contains the cost setting rules for the formation of a consolidated group. Each entity that becomes a subsidiary member of a consolidated group at the time it is formed (the formation time) is treated in the same way, subject to certain modifications, as an entity joining an existing consolidated group. [Schedule 3, item 2, section 705-130]

1.49 The Subdivision applies where one or more entities become subsidiary members of a consolidated group at the time it comes into existence as a consolidated group. It applies by modifying the basic case rules of a single entity joining a consolidated group. [Schedule 3, item 2, sections 705-135 and 705-140]

1.50 The modifications to the case of a single entity joining a consolidated group are:

• order in which tax cost setting amounts are worked out (see paragraphs 1.52 to 1.55);

• allocable cost amount adjustments where there have been roll-overs from the head company to subsidiaries before the formation time (see paragraphs 1.56 to 1.66);

• adjustments for successive distributions of profits (see paragraphs 1.67 and 1.68);

• allocation of allocable cost amount to membership interests in subsidiary entities with certain losses (see paragraphs 1.69 to 1.71); and

• determining pre-CGT factors for assets of subsidiaries (see paragraphs 1.72 and 1.73).

1.51 Where a consolidated group forms before 1 July 2004 there are transitional options available that may alter the treatment under the formation cost setting rules. Those transitional options are explained in paragraphs 1.77 to 1.114.

1.52 Where a subsidiary member of the group (the first subsidiary) holds membership interests in another subsidiary member of the group (the second subsidiary), it is necessary to first apply the tax cost setting rules to the first subsidiary. This will set the tax cost of the assets of the first subsidiary, including a cost for the membership interests in the second subsidiary. [Schedule 3, item 2, subsections 705-145(1) and (2)]

1.53 The amount set for the membership interests in the second subsidiary will then determine the cost base of those membership interests for the purposes of determining the joined group’s allocable cost amount in relation to the second subsidiary [Schedule 3, item 2, subsection 705-145(3)]. This amount replaces the amount that would be worked out under subsection 705-65(1) in relation to these membership interests. As such, subsections 705-65(2) to (4) do not apply in relation to this amount. However, the prevention of the later operation of the value shifting rules in relation to these membership interests is preserved [Schedule 3, item 2, subsection 705-145(4)].

1.54 This tax cost setting amount for the membership interests is not used for the purposes of working out the terminating value of assets consisting of those membership interests. Rather, the terminating value of membership interests is calculated by reference to the assets the leaving entity takes with it when it leaves the consolidated group.

1.55 In the basic case of a single entity joining a consolidated group, rights and options to acquire membership interests are treated as if they were membership interests. Similarly, in the formation case, rights and options to acquire membership interests are treated as if they were membership interests. [Schedule 3, item 2, subsection 705-145(5)]

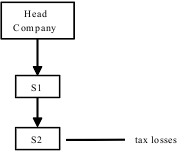

Example 1.2: Order of application of the tax cost setting rules

Head Co owns all the membership interests in T Co. T Co owns all the membership interests in X Co. On 1 July 2002, Head Co forms a consolidated group with the other companies.

First, work out the tax cost setting amounts for T Co’s assets according to the rules for an entity joining a consolidated group. T Co’s assets will include the membership interests T Co holds in X Co.

Then work out the tax cost setting amounts for X Co’s assets according to the same rules. For this purpose, the cost base of the membership interests in X Co (step 1 in working out the allocable cost amount) is determined by the reset costs of those membership interests, the costs for these membership interests having been reset along with the rest of T Co’s assets.

1.56 In certain circumstances, where there has been a roll-over from the head company, adjustments need to be made in working out the allocable cost amounts for subsidiary members.

1.57 One effect of a roll-over within a wholly-owned group (under Subdivision 126-B or section 160ZZO of the ITAA 1936) is to defer the gain that would otherwise be brought to account as a result of the disposal. The gain is deferred until the asset leaves the group – either because it is disposed of directly, or it leaves the group via the disposal of an entity. The deferral takes place by allowing the recipient company to retain the originating company’s cost base for the asset. Another effect that can occur where the originator in a roll-over is the head company, is that the group’s aggregate cost for its assets following consolidation would be different from what it would have been if the roll-over had not occurred. The purpose of this provision is to offset any effect that a roll-over would otherwise have in altering a consolidated group’s aggregate cost for its assets. [Schedule 3, item 2, subsection 705-150(1)]

1.58 An adjustment is not required under the basic case of a single entity joining a consolidated group as the relevant roll-over can only occur within a wholly-owned group. An adjustment is also not required where the roll-over does not involve the head company. This is because:

• Division 138 applies to adjust cost bases for membership interests where roll-overs shift value between ‘sister’ companies or from a wholly-owned subsidiary to its parent; and

• a roll-over from a parent to its wholly-owned subsidiary will only alter the aggregate cost for assets in a subsequently formed consolidated group where the originating company in a roll-over within a wholly-owned group is the head company.

1.59 Allocable cost amount adjustments will need to be considered where all of the following conditions are met:

• before the formation time, there is a roll-over under Subdivision 126-B or section 160ZZO of the ITAA 1936 (the head company roll-over event) in relation to a CGT asset (the head company roll-over asset);

• a member of the consolidated group was the recipient company (the head company roll-over recipient), and the entity that becomes the head company of the consolidated group was the originating company, in relation to the roll-over;

• after the first roll-over but before the formation time there was not a further roll-over from the head company to a member of the consolidated group (this can only occur if after the first roll-over the same asset was rolled back to the head company and then rolled-over by the head company again – either to the same entity as the first roll-over, or to another member of the consolidated group);

• there was either:

− no CGT event between the time of the roll-over and the formation time; or

− if there was a CGT event, then there must have been a roll-over under Subdivision 126-B or section 160ZZO of the ITAA 1936;

• the CGT asset that was the subject of the roll-over is not a pre-CGT asset at the formation time; and

• the sum of the head company’s cost bases of all of its CGT assets just before the head company roll-over event was different to the sum of the head company’s cost bases of all of its CGT assets just after the head company roll-over event.

[Schedule 3, item 2, subsection 705-150(2)]

1.60 The amount of any adjustment is worked out by reference to the head company roll-over adjustment amount. The head company roll-over adjustment amount is the difference between the head company’s cost bases of CGT assets immediately before the roll-over and the sum of its cost bases of CGT assets just after the roll-over event.

1.61 If the specified conditions are met (listed in paragraph 1.59), the result from step 3 in working out the group’s allocable cost amount for the recipient company is adjusted. The result from step 3 is reduced (if the amount worked out for the purposes of this rule is positive) or increased (if the amount is negative) by the amount worked out as follows:

[Schedule 3, item 2, subsections 705-150(3)]

1.62 The components of the formula are such that, where the sum of the head company’s cost bases for CGT assets does not change as a result of the roll-over event, no adjustments are required. No correction is required because the roll-over would not alter the group’s aggregate cost for its assets after applying the cost setting rules for consolidation from what that aggregate cost would have been if the roll-over had not occurred.

Example 1.3: Effect of a pre-formation roll-over

Prior to consolidation the head company of a consolidated group (HC) rolls over an asset with a cost base of $10 and market value of $100 to a subsidiary company (SC) for consideration consisting only of the shares issued in SC. HC’s cost base for the consideration shares is the market value of the roll-over asset (i.e. $100). This has the effect of increasing HC’s aggregate cost bases for its CGT assets, which include the membership interests in SC, by $90. (Before the roll-over it had a CGT asset with a cost base of $10, after the roll-over it had a CGT asset with a cost base of $100).

If HC and SC were then to form a consolidated group, HC’s allocable cost amount for SC would be $100 at step 1, for HC’s cost base for membership interests in SC. This amount is reduced under section 705-150 by $90 (the head company roll-over adjustment amount). Assuming the asset is the only asset held by SC, upon consolidation, the reduced allocable cost amount of $10 will be pushed down onto the rolled over asset.

Without a rule to reduce the allocable cost amount, after consolidation the roll-over would have increased the group’s cost base for its assets by $90.

1.63 Where the head company holds membership interests in a company interposed between it and the recipient company, adjustments must be made to the step 3 result in working out the group’s allocable cost amount for the interposed entity.

1.64 The step 3 result is reduced (if the amount worked out for the purposes of this rule is positive) or increased (if the amount is negative) by the amount worked out as follows:

[Schedule 3, item 2, subsection 705-150(4)]

1.65 If an adjusted step 3 result after applying these provisions would be negative, the step 3 result is taken to be nil and the head company makes a capital gain equal to that negative amount. Rules to provide a CGT event under which the capital gain will arise are to be included in a later bill.

1.66 In applying step 4, the adjusted step 3 result is the amount to be taken into account.

1.67 A modification to step 4 of the allocable cost amount calculation is required on formation of a group to prevent duplication of reductions in the allocable cost amount for distributions that are effectively a return of the cost of acquiring membership interests. This duplication can occur if reductions are made separately for the distribution of the same profits through a chain of 2 or more entities. [Schedule 3, item 2, subsection 705-155(1)]

1.68 The basic case rules are altered on formation so that if a reduction to the allocable cost amount for a subsidiary member at the formation time is required because of step 4 in respect of a distribution, there is no further reduction of the allocable cost amount of a second entity that becomes a subsidiary member of the group at that time if step 4 would otherwise require a reduction for the successive distribution of that amount. [Schedule 3, item 2, sections 705-155(2) and (3)]

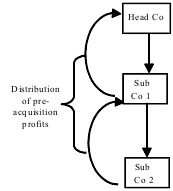

Example 1.4: Successive distributions of pre-acquisition profits

Suppose Sub Co 2 makes a distribution of pre-acquisition profits (i.e. a distribution of profits that accrued to membership interests before those membership interests came to be directly or indirectly owned by the head company and which, therefore, would require an amount to be deducted at step 4 in working out the allocable cost amount for an entity joining a consolidated group) to Sub Co 1 and Sub Co 1 also makes a distribution of those same profits to Head Co. In this case, without modification step 4 would reduce the group’s allocable cost amount for Sub Co 1 and also reduce the group’s allocable cost amount for Sub Co 2. This would result in a duplicated reduction in allocable cost amounts as a result of the distribution of the same profits.

Therefore, the reduction is only taken into account in relation to the distribution by Sub Co 2, as the distribution by Sub Co 1 is a successive distribution of the same amount.

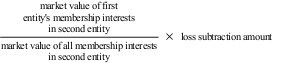

1.69 The rule for the allocation of the allocable cost amount to reset cost base assets is modified on formation where a reset cost base asset is a membership interest in a group entity and that group entity has an amount of losses that will be deducted under step 5 of the allocable cost amount calculation. For the purpose of allocating the allocable cost amount, the value to be used for that membership interest is its market value plus the amount of that membership interest’s pro-rata share of the losses. [Schedule 3, item 2, subsections 705-160(1) and (2)]

1.70 The amount of that membership interest’s share of the losses is calculated under the following formula (where the loss subtraction amount is the amount that is required to be deducted under step 5 of the allocable cost amount calculation):

[Schedule 3, item 2, subsection 705-160(3)]

1.71 The purpose of the adjustment is to prevent a distortion in the allocation of the allocable cost amount. In the absence of section 705-160, the losses of a subsidiary member would reduce both:

• the amount of the allocable cost amount that is allocated to membership interests, which represent direct or indirect interests in the subsidiary member with the losses (the unintended effect); and

• the allocable cost amount for the subsidiary member with the losses (the intended effect of step 5 in working out the allocable cost amount).

Example 1.5: Allocation to subsidiaries with membership interests in other subsidiaries with certain losses

Head Company forms a consolidated group with subsidiary members S1 and S2. Assuming that S2 has an amount of tax losses that will be deducted under step 5, when allocating the consolidated group’s allocable cost amount to the membership interests that S1 has in S2, the market value of those interests will reflect the losses that S2 has, and will be therefore lower than if S2 did not have losses. The lower market value of these membership interests will distort the amount of allocable cost amount allocated to those membership interests and is an unintended consequence.

Therefore, when working out the market value of the membership interests that S1 has in S2, an amount must be added to that market value to take into account S1’s share of S2’s losses.

1.72 Where a head company’s directly held and indirectly held membership interests in a joining subsidiary entity are pre-CGT assets, the pre-CGT status of those interests is preserved by attaching a pre-CGT factor to the assets, other than current assets, of the subsidiary. This treatment also applies upon the formation of a consolidated group. The pre-CGT membership interests to be preserved, by attaching a pre-CGT factor to underlying assets, are the pre-CGT membership interests held by the head company only. [Schedule 3, item 2, subsection 705-165(1)]

1.73 If, when a consolidated group is formed, subsidiary members of the group hold membership interests in another subsidiary member of the group, a pre-CGT factor must first be worked out for the assets of those members before any pre-CGT factor can be worked out for the assets of the other subsidiary member. The actual pre-CGT membership interest that the subsidiary member holds in the other subsidiary member is ignored. [Schedule 3, item 2, subsection 705-165(2)]

Example 1.6: Determining a pre-CGT factor for assets of subsidiaries

Head Co owns all the membership interests in T Co. T Co owns all the membership interests in X Co. On 1 July 2002, Head Co forms a consolidated group with the other companies.

First, work out the pre-CGT factor for T Co’s assets, including for the membership interests T Co holds in X Co.

Then work out the pre-CGT factor for X Co’s assets. For this purpose, the number of pre-CGT membership interests in X Co is determined from the pre-CGT factor for those membership interests worked out in determining the pre-CGT factor for all of T Co’s assets.

1.74 Rules dealing with the interaction between Subdivisions 165-CC and 165-CD and the cost setting rules on formation of a consolidated group will be included in a later bill.

1.75 The rules dealing with the changes to the cost setting rules that were included in the Consolidation Bill introduced on 16 May 2002 and the rules for forming a consolidated group have effect from 1 July 2002. [Schedule 7, item 1, section 700-1]

1.76 The transitional rules will apply to:

• modify the application of rules for transitional groups (see paragraphs 1.77 to 1.114); and

• modify the capital allowance provisions in the IT(TP) Act 1997 (see paragraphs 1.115 to 1.117).

1.77 There are certain transitional rules that are only applicable to a consolidated group if it comes into existence during the period from 1 July 2002 to 30 June 2004 (the transitional period).

1.78 These rules concern:

• forming a consolidated group during the transitional period (see paragraphs 1.79 to 1.85);

• chosen transitional entities (see paragraphs 1.86 to 1.87);

− tax cost and trading stock value not set for assets of chosen transitional entities (see paragraph 1.88);

• working out the allocable cost amount on formation for subsidiary members other than chosen transitional entities (see paragraphs 1.89 to 1.97);

• no operation of value shifting and loss transfer provisions to membership interests in chosen transitional entities (see paragraphs 1.98 to 1.99);

• undistributed, unfrankable pre-formation profits of non-chosen transitional entities – adjustment to allocable cost amount and tax cost setting amount reduction for over-depreciated assets (see paragraphs 1.100 to 1.103);

• CGT event for pre-formation roll-over after 16 May 2000 to be disregarded if cost base, etc. would be different (see paragraphs 1.104 to 1.107);

• when an entity leaves the consolidated group, the head company may choose, for the purposes of a transitional group’s allocable cost amount, to increase the terminating values of over-depreciated assets (see paragraphs 1.108 to 1.111); and

• when an entity leaves the consolidated group, the head company may choose, for the purposes of transitional group’s allocable cost amount, to use formation time market values, instead of terminating values, for certain pre-CGT assets (see paragraphs 1.112 to 1.114).

1.79 The rules separate the transition period into 3 categories. Groups can be formed:

• on 1 July 2002;

• after 1 July 2002 but before 1 July 2003; or

• during the financial year starting on 1 July 2003.

1.80 Where a consolidated group comes into existence on 1 July 2002, the group is a transitional group and each entity that becomes a subsidiary member of the group on that day is a transitional entity. [Schedule 7, item 2, subsection 701-1(1)]

1.81 Where a consolidated group comes into existence after 1 July 2002 but before 1 July 2003, the group is a transitional group if at least one entity that becomes a subsidiary member of the group on that day is a transitional entity. [Schedule 7, item 2, paragraph 701-1(2)(a)]

1.82 For those groups, an entity will be a transitional entity if at some time after 1 July 2002 and before the group came into existence, it was a wholly-owned subsidiary of the head company of the group and remained a wholly-owned subsidiary from that time until the consolidated group came into existence. [Schedule 7, item 2, subparagraph 701-1(2)(b)(ii)]

1.83 For these groups, an entity will also be a transitional entity if it is a subsidiary member of the group on the formation day, and became a wholly-owned subsidiary of the head company on that day, and had not at any time after 1 July 2002 and before formation day previously been a wholly-owned subsidiary. This will cover entities that become wholly-owned subsidiaries on the day of formation, provided they had not previously been wholly-owned and had stopped being a wholly-owned subsidiary during the period after 1 July 2002 and before formation. [Schedule 7, item 2, subparagraph 701-1(2)(b)(i)]

1.84 Where a consolidated group comes into existence during the year starting on 1 July 2003, the group is a transitional group if at least one entity that becomes a subsidiary member of the group on the day of formation is a transitional entity. [Schedule 7, item 2, paragraph 701-1(3)(a)]

1.85 For these an entity will be a transitional entity if just before 1 July 2003 it was a wholly-owned subsidiary of the head company and it remained wholly-owned from 1 July 2002 or the earliest time after 1 July 2002 when it became a wholly-owned subsidiary until the consolidated group came into existence. [Schedule 7, item 2, paragraph 701-1(3)(b)]

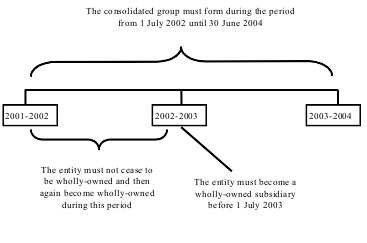

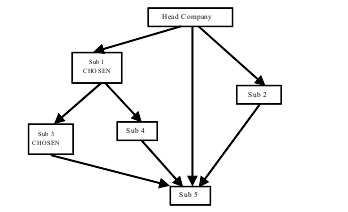

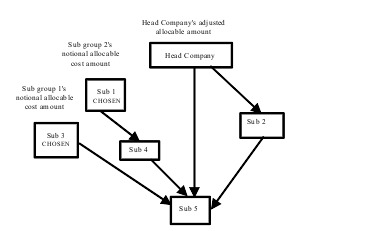

Diagram 1.1: Transitional time line

Chosen transitional entity

Chosen transitional entity1.86 Some transitional provisions are only available to transitional entities where a choice has been made by the head company of a transitional group in relation to those entities. Where a head company makes such a choice, the entity is a chosen transitional entity, or if there is more than one the entities are chosen transitional entities. The choice must be made by the end of the period for notifying the Commissioner of the decision to consolidate. Once this choice has been made, it cannot be revoked. [Schedule 7, item 2, section 701-5]

1.87 However, the rules for determining a pre-CGT factor for the assets of a subsidiary member are unchanged for chosen transitional entities. For this purpose, limited valuations will be required (i.e. valuation of the subsidiary entity itself and valuation of the aggregate of the assets to which a pre-CGT factor is attached).

1.88 Where a consolidated group is a transitional group, the head company may choose that the tax cost is not set for assets of chosen transitional entities. Instead, the head company will inherit the existing tax costs of the assets. This choice provides an option for groups to consolidate during the transitional period without having to undertake market valuations of all of the assets of subsidiary members of the group, or undertake allocable cost amount calculations for subsidiary members. Where the consolidated group elects that the tax cost of assets is not set, subsection 701-35(4) does not apply, and an entity is able to revalue its trading stock in accordance with the trading stock provisions immediately prior to joining a consolidated group. [Schedule 7, item 2, section 701-15]

1.89 Where the head company of a transitional group elects that a transitional entity is to be a chosen transitional entity, it is necessary to modify the core rules for working out the allocable cost amount of each entity that is not a chosen transitional entity at the formation time. This is because the chosen transitional entity is like a head company in relation to any membership interests it holds in other entities. [Schedule 7, item 2, subsections 701-20(1) and (2)]

1.90 The allocable cost amount for each non-chosen subsidiary, will be affected if a chosen transitional entity has any membership interests in it, held either directly or indirectly. Where a chosen transitional entity holds membership interests in non-chosen subsidiary, either directly or indirectly through one or more other non-chosen subsidiaries, the chosen transitional entity and each interposed non-chosen subsidiary comprise a sub-group in relation to the non-chosen subsidiary. [Schedule 7, item 2, paragraph 701-20(6)(a)]

1.91 The sub group membership interests in relation to the sub group comprise the membership interests that the chosen transitional entity holds directly in the non-chosen subsidiary and any of the interposed non-chosen subsidiaries, and the membership interests that each interposed non-chosen subsidiary holds directly in the non-chosen subsidiary or in any of the other interposed non-chosen subsidiaries. [Schedule 7, item 2, paragraph 701-20(6)(b)]

1.92 If a chosen transitional entity holds any membership interests in another chosen transitional entity, these membership interests are disregarded.

1.93 In relation to each sub-group, it is necessary to work out the subgroup’s notional allocable cost amount for each non-chosen subsidiary. This is the amount that would be the allocable cost amount if the sub group was treated as a consolidated group, formed at the same time as the transitional group, with the chosen transitional entity as the head company. [Schedule 7, item 2, subsection 701-20(5)]

1.94 In applying steps 2 to 7 to work out the sub group’s notional allocable cost amount, only a portion of the amount that is calculated in relation to those steps is taken into account. The portion represents the proportion of those sub group membership interests in the amounts. [Schedule 7, item 2, paragraph 701-20(5)(d)]

1.95 The head company’s adjusted allocable amount for the non-chosen subsidiary is the amount that would be the transitional group’s allocable cost amount for that entity if the sub group membership interests were disregarded. That is, only the membership interests held by the head company directly or via any interposed non-chosen transitional entities are taken into account at step 1. [Schedule 7, item 2, paragraph 701-20(4)(a)]

1.96 In applying steps 2 to 7 to work out the head company adjusted allocable amount, only a portion of the amount that is calculated in relation to those steps is taken into account. The portion represents the proportion of those sub group membership interests in the amounts. [Schedule 7, item 2, paragraph 701-20(4)(b)]

1.97 The allocable cost amount for each non-chosen transitional entity is the sum of the head company adjusted allocable amount and each sub group’s notional allocable cost amount for the non-chosen subsidiary. [Schedule 7, item 2, subsection 701-20(3)]

Example 1.7: Chosen transitional entity and sub groups

Suppose

that this group is a transitional group, and that all the subsidiaries are

transitional entities. Head Company makes the choice under the transitional

measures to retain the existing cost bases of Sub 1 and Sub 3, making them

chosen transitional entities. Sub 2, Sub 4 and Sub 5 are all non-chosen

transitional entities.

Suppose

that this group is a transitional group, and that all the subsidiaries are

transitional entities. Head Company makes the choice under the transitional

measures to retain the existing cost bases of Sub 1 and Sub 3, making them

chosen transitional entities. Sub 2, Sub 4 and Sub 5 are all non-chosen

transitional entities.

There are 2 sub-groups in relation to Sub 5 as a result of the elections. Sub 3 forms a sub group in relation to its membership interests in Sub 5. Sub 1 and Sub 4 are also a sub group in relation to their direct and indirect membership interests in Sub 5. The sub group’s calculate their notional allocable cost amount in relation to Sub 5. The Head company’s adjusted allocable amount is calculated ignoring its membership interests in the 2 sub-groups. The head company’s adjusted allocable amount is added to the 2 sub group’s notional allocable cost amounts to arrive at the allocable cost amount for Sub 5. This means that membership interests that Head company holds in Sub 1 and the membership interests that Sub 1 holds in Sub 3 are disregarded in working out the allocable cost amount for Sub 5.

No operation of value shifting and loss transfer provisions

to membership interests in chosen transitional entities

No operation of value shifting and loss transfer provisions

to membership interests in chosen transitional entities 1.98 Where the head company of a consolidated group elects that an entity is a chosen transitional entity and therefore inherits the ‘tax costs’ for its assets, then any outstanding cost base adjustments for value shifting or loss transfers will not apply to membership interests in that subsidiary member in relation to events that happened before the consolidated group comes into existence. [Schedule 7, item 2, section 701-25]

1.99 The cost base adjustments do not need to be made because the cost base of the membership interests is not allocated to the entities assets, so the effect of the value shift or loss transfer on the membership interests has not been transferred to the tax cost of the assets of the entity. Furthermore, intra-group membership interests within a consolidated group are ignored for income tax purposes. This means, for example, that the potential for losses to be duplicated or created in relation to those membership interests no longer exists.

1.100 The requirement that undistributed profits be frankable to be included in step 3 when working out the allocable cost amount is not required for a non-chosen transitional entity. For a non-chosen transitional entity the amount to be added at step 3 of the allocable cost amount calculation is the undistributed profits of the entity that accrued to the joined consolidated group’s membership interests and if distributed to the head company, the head company and every other transitional entity interposed between the non-chosen entity and the head company would be entitled to a rebate of income tax under section 46 or 46A of the ITAA 1936. [Schedule 7, item 2, subsection 701-30(1)]

1.101 This is achieved by increasing the step 3 amount (the step 3 unfrankable profits increase) by disregarding subsections 705-90(3) and (4) and paragraph 705-90(6)(b)when working out the step 3 amount. This has the effect of ignoring the unfrankable undistributed and not excluding those profits that recouped a tax loss. [Schedule 7, item 2, subsection 701-30(2)]

1.102 As a consequence of the change in step 3 when working out the allocable cost amount for non-chosen transitional entities, the tax deferral amount for the purpose of applying section 705-50 (reduction in tax cost setting amount for over-depreciated assets) may be increased. [Schedule 7, item 2, subsection 701-30(3)]

1.103 The increase, if any, is equal to the amount that would have been the step 3 unfrankable profits increase, provided that the profits that gave rise to that increase also meet the following requirements:

• they were not subject to income tax because of deductions for the asset’s decline in value;

• the decline in value represented the over-depreciation of the asset; and

• the deductions for the decline in value do not form part of a tax loss covered by the step 5 amount.

[Schedule 7, item 2, subsection 701-30(4)]

1.104 Where, following the formation of a transitional group, the cost base or reduced cost base of an asset of the group would be different from what it would otherwise have been because the asset was rolled over under Subdivision 126-B after 16 May 2002, the transfer of the asset is disregarded in applying the consolidation provisions. The transfer is also disregarded in applying the consolidation provisions where there was not a roll-over under Subdivision 126-B but there was roll-over relief under section 40-340. [Schedule 7, item 2, section 701-35]

1.105 Section 701-35 applies to disregard the asset transfer where the transfer would have altered the cost base or reduced cost base of any asset within the group after group formation. Consequently, any effect the transfer would have had in altering the tax value of any asset within the group for any purpose (i.e. for CGT, capital allowances or trading stock purposes) does not occur.

Example 1.8: Pre-formation asset transfer with roll-over

In June 2002, Subco A transfers Asset X to Subco B and there is a roll-over under Subdivision 126-B in connection with the transfer. On 1 July 2002 a consolidated group is formed with Subco A and Subco B as subsidiary members. The tax values of the assets of the group within consolidation will be those that they would have been if the asset transfer had not occurred – that is, as though Asset X were an asset of Subco A at the formation time and any consideration that Subco B gave for the transfer were still an asset of Subco B.

1.106 Section 701-35 is not confined in its application to tax values of assets immediately involved in an asset transfer. If the tax value of any other asset within a consolidated group would be different because of an asset transfer with roll-over (for CGT or capital allowances purposes) within the relevant time period, the tax value of that asset will be what it would have been had the asset transfer not occurred.

1.107 Where an affected asset is subsequently disposed of or becomes an asset of an entity that leaves the group, this provision operates to the extent that it affects the tax value of the asset or the head company’s terminating value for the asset. It does not, for example, preclude the asset from being an asset of a leaving entity because the pre-consolidation transfer is disregarded in applying the consolidation provisions.

1.108 As a transitional concession, the head company is able to choose in certain circumstances that, where a subsidiary holding an over-depreciated asset leaves the consolidated group, the cost base of the equity in the subsidiary is not reduced because of the over-depreciated asset adjustment. [Schedule 7, item 2, subsection 701-40(1)]

1.109 In order to make the choice, the following conditions must be satisfied:

• the leaving subsidiary must hold an asset at the leaving time [Schedule 7, item 2, subsection 701-40(2)];

• the asset became an asset of the head company of the transitional group because of the single entity rule [Schedule 7, item 2, paragraph 701-40(3)(a)];

• section 705-50 applied to the asset on formation to reduce the tax cost setting amount of the asset [Schedule 7, item 2, paragraph 701-40(3)(b)]; and

• the asset must have been continuously held by the group at all times from formation until the entity ceases to be a subsidiary member of the transitional group [Schedule 7, item 2, subsection 701-40(4)].

1.110 The effect of the choice is that if the leaving subsidiary joins another consolidated group, section 705-50 may again apply to the asset. Because of this, the head company must advise the leaving subsidiary of the amount by which the head company increases the terminating value. [Schedule 7, item 2, subsection 701-40(5)]

1.111 If all the requirements are satisfied, the head company may increase the terminating value for the asset by so much of the reduction amount (under section 705-50) as the head company chooses. This will have the effect of increasing the cost base of the head company’s equity in the leaving subsidiary. [Schedule 7, item 2, subsection 701-40(6)]

1.112 A head company that holds pre-CGT assets immediately prior to consolidation may be at a disadvantage when compared to a head company that transfers their pre-CGT assets (with roll-over) to a wholly-owned subsidiary. This is because the pre-CGT assets that come into the consolidated group via a subsidiary will have a reset cost base whereas the pre-CGT assets that the head company holds will not have their cost base changed.

1.113 Therefore, a transitional concession is provided to a head company that holds pre-CGT assets just before the consolidated group comes into existence, allowing it to choose to use the market value of the assets at formation time as the terminating value in determining its cost for membership interests in a leaving entity. This will enable the group to put itself in the same position as that of a group where pre-CGT assets have been transferred with roll-over relief to a subsidiary member, whilst avoiding the costs associated with rolling over assets. [Schedule 7, item 2, subsection 701-45(2)]

1.114 The concession does not apply if the head company only holds the pre-CGT asset because of a roll-over under Subdivision 126-B that happened after 11.45 am, by legal time in the Australian Capital Territory, on 21 September 1999 (announcement in the Government’s response to A Tax System Redesigned). This will prevent groups from transferring assets from subsidiaries to their head companies with roll-over relief to increase their cost base for membership interests in a leaving entity to take advantage of the choice that is available under this section. [Schedule 7, item 2, subsection 701-45(1)]

1.115 In setting the tax cost of a depreciating asset to which the capital allowance provisions in Subdivisions 40-A to 40-D and sections 40-425 to 40-445 apply, the cost for tax purposes is set on the basis that the asset was acquired by the head company at the time the entity became a subsidiary member of the consolidated group. As such, modifications are required to section 40-77 and subsection 40-285(6) of the IT(TP) Act 1997 to ensure the continued application of the capital allowances transitional provisions.

1.116 The modified application of section 40-77 will: