Commonwealth Consolidated Acts Commonwealth Consolidated Acts

Commonwealth Consolidated Acts Commonwealth Consolidated Acts(1A) This section has effect for the purposes of:

(a) section 165 - 115ZA; and

(b) sections 715 - 255 and 715 - 270 (about effect of alteration time for head company on membership interests of leaving entity just before leaving time).

Calculation of adjustment amount

(1) An adjustment amount in relation to an equity or debt is to be worked out by the affected entity, and applied by it in making reductions:

(a) if subsection (2) applies--in accordance with subsection (3); or

(b) otherwise--in accordance with subsection (6).

Selection of method of calculation

(2) This subsection applies if:

(a) the affected entity has a relevant equity interest, but does not have a relevant debt interest, in the * loss company immediately before the alteration time and:

(i) all the * shares in the loss company are of the same class and have the same * market value; and

(ii) the equity consists only of a share or shares in the loss company; or

(b) the affected entity has both a relevant equity interest, and a relevant debt interest under subsection 165 - 115Y(1), in the loss company immediately before the alteration time and:

(i) all the shares in the loss company are of the same class and have the same market value; and

(ii) the equity consists only of a share or shares in the loss company; and

(iii) the debt consists of a single debt or 2 or more debts of the same kind;

and the reductions that would result from the application of subsection (3) would be reasonable in the circumstances.

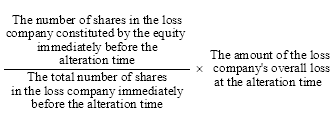

Formula method

(3) The adjustment amount to be worked out under this subsection is the amount worked out using the formula:

and the amount so worked out is to be applied in making reductions as follows:

(a) the adjustment amount is to be applied in relation to the * share or shares constituting the equity; and

(b) if there is an amount remaining after making reductions in relation to those shares--the amount remaining is to be applied in relation to any debt or, if there is a debt consisting of 2 or more separate debts, in relation to those debts.

Applying adjustment amount under formula method to shares

(4) If the adjustment amount referred to in subsection (3) is to be applied in relation to an equity consisting of 2 or more * shares:

(a) it is to be applied equally among the shares; and

(b) if there is any amount remaining after the application of part of the adjustment amount to a share, the amount remaining is to be applied to any other share, or equally among any other shares, to the maximum extent possible.

Applying adjustment amount under formula method to debt

(5) If the adjustment amount referred to in subsection (3) or part of it is to be applied in relation to a debt (the overall debt ) and the overall debt consists of 2 or more debts (the constituent debts ), the amount to be applied in relation to each constituent debt is the amount worked out using the formula:

Non - formula method

(6) The adjustment amount to be worked out under this subsection is the amount that is appropriate having regard to:

(a) the object of this Subdivision and other matters set out in section 165 - 115J; and

(b) the extent of the affected entity's relevant equity interests or relevant debt interests, as the case may be, in the * loss company immediately before the alteration time; and

(c) when, and under what circumstances, the relevant equity interests or relevant debt interests were * acquired by the affected entity; and

(d) the loss company's overall loss at the alteration time; and

(e) the extent to which that overall loss has reduced the * market values of the equity or debt; and

(f) to prevent double counting, the extent of any adjustments required under this Subdivision because of any application of this Subdivision to another loss company in which the affected entity has a relevant equity interest or relevant debt interest;

and the amount so worked out is to be applied in making reductions in an appropriate way.

How to work out the extent to which the overall loss has reduced the market value of an equity or debt

(7) To avoid doubt in applying paragraph (6)(e) in relation to an equity or a debt, if factors other than an overall loss altered the * market value of the equity or debt, the extent to which the overall loss reduced that market value is taken to be the extent to which that market value would have been reduced apart from those other factors.

Note 1: For a company's overall loss see subsections 165 - 115R(5) and 165 - 115S(5).

Note 2: An example of a factor other than the overall loss is the unrealised value of assets (including assets in respect of which there is an unrealised gain) of the loss company, whether or not generated by outlays or economic losses reflected in the loss for income tax purposes.