Commonwealth Consolidated Acts Commonwealth Consolidated Acts

Commonwealth Consolidated Acts Commonwealth Consolidated ActsIncome Tax Assessment Act 1997

1 Section 705 - 155

Repeal the section, substitute:

Object

(1) The object of this section is to ensure that, in working out the group's * allocable cost amount for entities that become * subsidiary members of the group at the formation time, the reduction under step 4 in the table in section 705 - 60 (about pre - formation time distributions out of certain profits) is made only for profits that have been effectively distributed to the * head company in respect of its direct * membership interests in the entities. This ensures consistency with the ordering rule in section 705 - 145.

When section applies

(2) This section applies to a distribution (the subject distribution ) to the extent that the following conditions are satisfied:

(a) the distribution is made by an entity (the subject entity ) that becomes a * subsidiary member of the group at the formation time;

(b) in working out the group's * allocable cost amount for the subject entity there would, apart from this section, be a reduction under step 4 in the table in section 705 - 60 for the distribution.

Step 4 reduction only if subject distribution is made to head company etc.

(3) There is no reduction as mentioned in paragraph ( 2)(b) for the subject distribution unless:

(a) the subject distribution is made to the * head company of the group; or

(b) the reduction is in accordance with subsection ( 5).

Step 4 reduction for effective distribution to head company

(4) If:

(a) at the formation time, the * head company of the group has a direct * membership interest in the subject entity; and

(b) the head company acquired the membership interest directly from another entity, or indirectly as a result of one or more acquisitions from other entities, where:

(i) section 160ZZ0 of the Income Tax Assessment Act 1936 applied to each acquisition; or

(ii) there was a roll - over under Subdivision 126 - B for each acquisition;

or a combination of these happened; and

(c) while it held the membership interest, the entity, or one of the entities, mentioned in paragraph ( b) (the recipient of the further distribution ) received a distribution (the further distribution ) of some of the subject distribution from the subject entity;

the consequences in subsections ( 5) and (6) apply.

Reduction for further distribution that remains with recipient

(5) If:

(a) the following happen:

(i) by the formation time, any of the further distribution (the eligible reduction amount ) had not again been distributed by the recipient of the further distribution;

(ii) the recipient of the further distribution does not become a * subsidiary member of the group at the formation time; or

(b) the following happen:

(i) by the formation time, any of the further distribution (the eligible reduction amount ) had been distributed by the recipient of the further distribution to another entity directly, or indirectly though successive distributions by interposed entities;

(ii) that other entity does not become a subsidiary member of the group at the formation time; or

(c) both of the above paragraphs apply;

then, in working out the group's * allocable cost amount for the subject entity, the reduction under step 4 in the table in section 705 - 60 for the subject distribution only takes place to the extent that it equals the sum of all eligible reduction amounts.

Step 1 reduced cost base adjustment to reverse effect of reduction for further distribution

(6) Also, if subsection 160ZK(5) of the Income Tax Assessment Act 1936 or subsection 110 - 55(7) of this Act applied to the further distribution, then for the purposes of step 1 in the table in section 705 - 60 in working out the group's * allocable cost amount for the subject entity:

(a) the reference in subsection 705 - 65(3) to a reduction resulting from the application of subsection 160ZK(5) of the Income Tax Assessment Act 1936 ; and

(b) the reference in subsection 705 - 65(5) to a reduction that has taken place under subsection 110 - 55(7);

include a reference to the reduction in the * reduced cost base of the membership interest in the subject entity resulting from the application of subsection 160ZK(5) of the Income Tax Assessment Act 1936 , or subsection 110 - 55(7) of this Act, to the further distribution.

2 Section 705 - 230

Repeal the section, substitute:

Object

(1) The object of this section is to ensure that, in working out the group's * allocable cost amount for the linked entities, the reduction under step 4 in the table in section 705 - 60 (about pre - formation time distributions out of certain profits) is made only for profits that have been effectively distributed to the * head company in respect of its direct * membership interests in the entities. This ensures consistency with the ordering rule in section 705 - 225.

When section applies

(2) This section applies to a distribution to the extent that the following conditions are satisfied:

(a) the distribution is made by a linked entity;

(b) in working out the group's * allocable cost amount for the linked entity there would, apart from this section, be a reduction under step 4 in the table in section 705 - 60 for the distribution.

Step 4 reduction only if subject distribution is made to head company

(3) There is no reduction as mentioned in subsection ( 2) for the distribution unless it is made to the * head company of the group.

Part 2 -- Consequential amendments relating to simplified imputation system

Income Tax Assessment Act 1997

3 Section 705 - 60 (table item 3, column headed "What the step requires")

Omit "frankable", substitute "taxed".

4 Subsection 705 - 90(3)

Repeal the subsection, substitute:

Extent to which tax paid on undistributed profits

(3) Then work out how much of the undistributed profits does not exceed the amount worked out using the following formula as at the joining time:

5 Section 705 - 90 (heading)

Repeal the heading, substitute:

6 Paragraph 705 - 90(6)(a)

Omit ", if they had been distributed as dividends at the joining time, could have been so franked", substitute "satisfy the requirements of subsection ( 3)".

Income Tax (Transitional Provisions) Act 1997

7 Subsection 701 - 30(2)

Omit " unfrankable ", substitute " untaxed ".

Note: The heading to section 701 - 30 is altered by omitting " unfrankable " and substituting " untaxed ".

8 Subsection 701 - 30(4)

Omit "unfrankable", substitute "untaxed".

Income Tax Assessment Act 1997

9 Section 705 - 160

Repeal the section, substitute:

Object

(1) The object of this section is to prevent a distortion under section 705 - 35 in the allocation of * allocable cost amount to an entity that becomes a * subsidiary member of the group where that entity has direct or indirect * membership interests in another entity that has certain profits or tax losses when it becomes a subsidiary member.

Adjustment to allocation of allocable cost amount where direct interest in entity with profits/losses

(2) If:

(a) an entity becomes a * subsidiary member of the group at the formation time; and

(b) the entity has * membership interests in a second entity that becomes a subsidiary member of the group at that time; and

(c) in working out the group's * allocable cost amount for the second entity:

(i) an amount is required to be added (the second entity's profit/loss adjustment amount ) under step 3 in the table in section 705 - 60 (about profits accruing before becoming a subsidiary member of the group); or

(ii) an amount is required to be subtracted (also the second entity's profit/loss adjustment amount ) under step 5 in the table in section 705 - 60 (about losses accruing before becoming a subsidiary member of the group);

then, for the purposes of working out under section 705 - 35 the * tax cost setting amount for the assets of the first entity, the * market value of the first entity's membership interests in the second entity is reduced (in a subparagraph ( c)(i) case) or increased (in a subparagraph ( c)(ii) case) by the first entity's interest in the second entity's profit/loss adjustment amount (see subsection ( 3)).

First entity's interest in second entity's profit/loss adjustment amount

(3) The first entity's interest in the second entity's profit/loss adjustment amount is worked out using the formula:

Adjustment to allocation of allocable cost amount for indirect interest in entity with profits/losses

(4) If:

(a) an entity becomes a * subsidiary member of the group at the formation time; and

(b) the entity has * membership interests in a second entity that becomes a subsidiary member of the group at that time; and

(c) the second entity has, directly or indirectly through one or more interposed entities that become subsidiary members of the group at the formation time, membership interests in a third entity that becomes a subsidiary member of the group at that time; and

(d) in working out the group's * allocable cost amount for the third entity:

(i) an amount is required to be added (the third entity's profit/loss adjustment amount ) under step 3 in the table in section 705 - 60 (about profits accruing before becoming a subsidiary member of the group); or

(ii) an amount is required to be subtracted (also the third entity's profit/loss adjustment amount ) under step 5 in the table in section 705 - 60 (about losses accruing before becoming a subsidiary member of the group);

then, for the purposes of working out under section 705 - 35 the * tax cost setting amount for the assets of the first entity, the * market value of the first entity's membership interests in the second entity is reduced (in a subparagraph ( d)(i) case) or increased (in a subparagraph ( d)(ii) case) by the first entity's interest in the third entity's profit/loss adjustment amount (see subsection ( 5)).

First entity's interest in third entity's profit/loss adjustment amount

(5) The first entity's interest in the third entity's profit/loss adjustment amount is worked out using the formula:

where:

"market value of first entity's membership interests in third entity held through second entity" means the * market value of all * membership interests in the third entity that the first entity holds indirectly through the second entity (including through that entity and one or more other entities that become * subsidiary members of the group and are interposed between the second entity and the third entity).

10 Section 705 - 235

Repeal the section, substitute:

Object

(1) The object of this section is to prevent a distortion under section 705 - 35 in the allocation of * allocable cost amount to a linked entity where that entity has direct or indirect * membership interests in another linked entity that has certain profits or tax losses.

Adjustment to allocation of allocable cost amount where direct interest in linked entity with profits/losses

(2) If:

(a) a linked entity has * membership interests in a second linked entity; and

(b) in working out the group's * allocable cost amount for the second linked entity:

(i) an amount is required to be added (the second linked entity's profit/loss adjustment amount ) under step 3 in the table in section 705 - 60 (about profits accruing before becoming a subsidiary member of the group); or

(ii) an amount is required to be subtracted (also the second linked entity's profit/loss adjustment amount ) under step 5 in the table in section 705 - 60 (about losses accruing before becoming a subsidiary member of the group);

then, for the purposes of working out under section 705 - 35 the * tax cost setting amount for the assets of the first linked entity, the * market value of the first linked entity's membership interests in the second linked entity is reduced (in a subparagraph ( b)(i) case) or increased (in a subparagraph ( b)(ii) case) by the first linked entity's interest in the second linked entity's profit/loss adjustment amount (see subsection ( 3)).

First linked entity's interest in second linked entity's profit/loss adjustment amount

(3) The first linked entity's interest in the second linked entity's profit/loss adjustment amount is worked out using the formula:

Adjustment to allocation of allocable cost amount for indirect interest in linked entity with profits/losses

(4) If:

(a) a linked entity has * membership interests in a second linked entity; and

(b) the second linked entity has, directly or indirectly through one or more interposed linked entities, membership interests in a third linked entity; and

(c) in working out the group's * allocable cost amount for the third linked entity:

(i) an amount is required to be added (the third linked entity's profit/loss adjustment amount ) under step 3 in the table in section 705 - 60 (about profits accruing before becoming a subsidiary member of the group); or

(ii) an amount is required to be subtracted (also the third linked entity's profit/loss adjustment amount ) under step 5 in the table in section 705 - 60 (about losses accruing before becoming a subsidiary member of the group);

then, for the purposes of working out under section 705 - 35 the * tax cost setting amount for the assets of the first linked entity, the * market value of the first linked entity's membership interests in the second linked entity is reduced (in a subparagraph ( c)(i) case) or increased (in a subparagraph ( c)(ii) case) by the first linked entity's interest in the third linked entity's profit/loss adjustment amount (see subsection ( 5)).

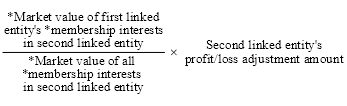

First linked entity's interest in third linked entity's profit/loss adjustment amount

(5) The first linked entity's interest in the third linked entity's profit/loss adjustment amount is worked out using the formula:

where:

"market value of first" linked entity's membership interests in third linked entity held through second linked entity means the * market value of all * membership interests in the third linked entity that the first linked entity holds indirectly through the second linked entity (including through that entity and one or more other linked entities that are interposed between the second linked entity and the third linked entity).

Income Tax Assessment Act 1997

11 Section 705 - 60 (after table item 3)

Insert:

3A | For each step 3A amount (if any) under section 705 - 93 (which is about pre - joining time intra - group roll - overs from foreign resident companies): (a) if the step 3A amount is an increase amount under that section--add to the result of step 3 (as affected by any previous application of this step) the step 3A amount; or (b) if the step 3A amount is a reduction amount under that section--subtract from the result of step 3 (as affected by any previous application of this step) the step 3A amount | To adjust for certain intra - group roll - overs from foreign companies before the joining time |

12 Section 705 - 60 (table item 4, column headed "What the step requires")

Omit "step 3", substitute "step 3A".

13 At the end of section 705 - 60

Add:

Note: The head company may be taken to have made a capital gain, depending on the amount remaining after applying step 3A: see CGT event L2.

14 After section 705 - 90

Insert:

When there is a step 3A amount

(1) For the purposes of step 3A in the table in section 705 - 60, there is a step 3A amount if:

(a) before the joining time:

(i) there was a roll - over under Subdivision 126 - B (a Subdivision 126 - B roll - over ) in relation to a * CGT event that happened in relation to an asset (the roll - over asset ); or

(ii) section 160ZZO of the Income Tax Assessment Act 1936 applied in relation to a disposal (a section 160ZZO roll - over ) of an asset (also the roll - over asset ); and

(b) the originating company in relation to the Subdivision 126 - B roll - over, or the transferor in relation to the section 160ZZO roll - over, was a foreign resident; and

(c) the recipient company in relation to the Subdivision 126 - B roll - over, or the transferee in relation to the section 160ZZO roll - over, was an Australian resident and was not the entity that became the * head company of the joined group; and

(d) between the Subdivision 126 - B roll - over, or the section 160ZZO roll - over, and the joining time, no other CGT event happened in relation to the roll - over asset for which there was not a Subdivision 126 - B roll - over or a section 160ZZO roll - over; and

(e) the roll - over asset is not a * pre - CGT asset at the joining time; and

(f) the roll - over asset becomes that of the head company of the joined group because subsection 701 - 1(1) (the single entity rule) applies when the joining entity becomes a * subsidiary member of the group.

What the step 3A amount is

(2) The step 3A amount is:

(a) if, as a result of the Subdivision 126 - B roll - over mentioned in subparagraph ( 1)(a)(i), or the section 160ZZO roll - over mentioned in subparagraph ( 1)(a)(ii), a * capital loss of the originating company was disregarded or a capital loss of the transferor was not incurred--an increase amount equal to the capital loss; or

(b) if, as a result of the Subdivision 126 - B roll - over mentioned in subparagraph ( 1)(a)(i), or the section 160ZZO roll - over mentioned in subparagraph ( 1)(a)(ii), a * capital gain of the originating company was disregarded or a capital gain of the transferor did not accrue--a reduction amount equal to the capital gain.

15 After section 705 - 145

Insert:

Object

(1) The object of this section is to modify the effect that section 705 - 93 (step 3A of allocable cost amount) has in accordance with this Subdivision so that it takes account of * membership interests that entities that become * subsidiary members hold in other such entities.

Apportionment of step 3A amount among first level interposed entities

(2) If:

(a) under section 705 - 93, in its application in accordance with this Subdivision, there is a step 3A amount for the purpose of working out the group's * allocable cost amount for an entity (the subject entity ) that becomes a * subsidiary member of the group at the formation time ; and

(b) at that time one or more entities (the first level entities ), that become subsidiary members of the group and in which the * head company holds * membership interests, are interposed between the head company and the subject entity;

then the step 3A amount is apportioned among the first level entities and the subject entity on the following basis:

(c) each first level entity has the following proportion of the step 3A amount:

where:

market value of all membership interests in subject entity means the * market value, at the formation time, of all * membership interests in the subject entity that are held by entities that become * members of the group at that time.

market value of first level entity's direct and indirect membership interests in subject entity means so much of the market value of all membership interests in the subject entity (as defined above) as is attributable to * membership interests that the first level entity holds directly, or indirectly through other interposed entities that become * subsidiary members of the group at the formation time; and

(d) the subject entity has the remainder of the step 3A amount.

Step 3A amount for assets consisting of membership interests held by subsidiary members in other subsidiary members

(3) If:

(a) before the formation time:

(i) there was a roll - over under Subdivision 126 - B (a Subdivision 126 - B roll - over ) in relation to a * CGT event that happened in relation to an asset (the roll - over asset ); or

(ii) section 160ZZO of the Income Tax Assessment Act 1936 applied in relation to a disposal (a section 160ZZO roll - over ) of an asset (also the roll - over asset ); and

(b) the originating company in relation to the Subdivision 126 - B roll - over, or the transferor in relation to the section 160ZZO roll - over, was a foreign resident; and

(c) the recipient company in relation to the Subdivision 126 - B roll - over, or the transferee in relation to the section 160ZZO roll - over, was an Australian resident and was not the entity that became the * head company of the group; and

(d) between the Subdivision 126 - B roll - over, or the section 160ZZO roll - over, and the formation time, no other CGT event happened in relation to the roll - over asset for which there was not a Subdivision 126 - B roll - over or a section 160ZZO roll - over; and

(e) the roll - over asset is a * membership interest in an entity that becomes a * subsidiary member at the formation time, other than one that is held at that time by the entity that becomes the head company of the group;

then, subject to subsection ( 5), there is under section 705 - 93 a step 3A amount for the purpose of working out the group's * allocable cost amount for the entity (the subject entity ) that holds the roll - over asset at the formation time.

What the step 3A amount is

(4) The step 3A amount is:

(a) if, as a result of the Subdivision 126 - B roll - over mentioned in subparagraph ( 3)(a)(i), or the section 160ZZO roll - over mentioned in subparagraph ( 3)(a)(ii), a * capital loss of the originating company was disregarded or a capital loss of the transferor was not incurred--an increase amount equal to the capital loss; or

(b) if, as a result of the Subdivision 126 - B roll - over mentioned in subparagraph ( 3)(a)(i), or the section 160ZZO roll - over mentioned in subparagraph ( 3)(a)(ii), a * capital gain of the originating company was disregarded or a capital gain of the transferor did not accrue--a reduction amount equal to the capital gain.

Apportionment of step 3A amount among first level interposed entities

(5) If at the formation time one or more entities, that become * subsidiary members of the group and in which the * head company holds * membership interests, are interposed between the head company and the subject entity, then the step 3A amount is apportioned among those entities and the subject entity in the same way as a step 3A amount is apportioned under subsection ( 2).

16 Section 705 - 150 (heading)

Repeal the heading, substitute:

17 Subsection 705 - 150(3) (heading)

Repeal the heading, substitute:

Adjustment to result of step 3A in allocable cost amount for head company roll - over recipient

18 Subsection 705 - 150(3)

Omit "step 3", substitute "step 3A".

19 Subsection 705 - 150(4) (heading)

Repeal the heading, substitute:

Adjustment to result of step 3A in allocable cost amount for interposed entity

20 Subsection 705 - 150(4)

Omit "step 3", substitute "step 3A".

21 Subsection 705 - 150(4) (note)

Repeal the note, substitute:

Note: If, after applying this section, the amount remaining as a result of step 3A in the table in section 705 - 60 is negative, the head company makes a capital gain equal to that amount: see CGT event L2.

22 After section 705 - 225

Insert:

Object

(1) The object of this section is to modify the effect that section 705 - 93 (step 3A of allocable cost amount) has in accordance with this Subdivision so that it takes account of * membership interests that linked entities hold in other linked entities at the time (the linked entity joining time ) when the linked entities become * subsidiary members of the group .

Apportionment of step 3A amount among first level interposed entities

(2) If:

(a) under section 705 - 93, in its application in accordance with this Subdivision, there is a step 3A amount for the purpose of working out the group's * allocable cost amount for a particular linked entity (the subject entity ); and

(b) at the linked entity joining time, one or more of the linked entities (the first level entities ) in which the * head company holds * membership interests are interposed between the head company and the subject entity;

then the step 3A amount is apportioned among the first level entities and the subject entity on the following basis:

(c) each first level entity has the following proportion of the step 3A amount:

where:

market value of all membership interests in subject entity means the * market value, at the linked entity joining time, of all * membership interests in the subject entity that are held by entities that become * members of the group at that time.

market value of first level entity's direct and indirect membership interests in subject entity means so much of the market value of all membership interests in the subject entity (as defined above) as is attributable to * membership interests that the first level entity holds directly, or indirectly through other linked entities; and

(d) the subject entity has the remainder of the step 3A amount.

Step 3A amount for assets consisting of membership interests held by linked entities in other linked entities

(3) If:

(a) before the linked entity joining time:

(i) there was a roll - over under Subdivision 126 - B (a Subdivision 126 - B roll - over ) in relation to a * CGT event that happened in relation to an asset (the roll - over asset ); or

(ii) section 160ZZO of the Income Tax Assessment Act 1936 applied in relation to a disposal (a section 160ZZO roll - over ) of an asset (also the roll - over asset ); and

(b) the originating company in relation to the Subdivision 126 - B roll - over, or the transferor in relation to the section 160ZZO roll - over, was a foreign resident; and

(c) the recipient company in relation to the Subdivision 126 - B roll - over, or the transferee in relation to the section 160ZZO roll - over, was an Australian resident and was not the entity that became the * head company of the group; and

(d) between the Subdivision 126 - B roll - over, or the section 160ZZO roll - over, and the linked entity joining time, no other CGT event happened in relation to the roll - over asset for which there was not a Subdivision 126 - B roll - over or a section 160ZZO roll - over; and

(e) the roll - over asset is a * membership interest in a linked entity, other than one that is held at that time by the entity that becomes the head company of the group;

then, subject to subsection ( 5), there is under section 705 - 93 a step 3A amount for the purpose of working out the group's * allocable cost amount for the linked entity (the subject entity ) that holds the roll - over asset at the linked entity joining time.

What the step 3A amount is

(4) The step 3A amount is:

(a) if, as a result of the Subdivision 126 - B roll - over mentioned in subparagraph ( 3)(a)(i), or the section 160ZZO roll - over mentioned in subparagraph ( 3)(a)(ii), a * capital loss of the originating company was disregarded or a capital loss of the transferor was not incurred--an increase amount equal to the capital loss; or

(b) if, as a result of the Subdivision 126 - B roll - over mentioned in subparagraph ( 3)(a)(i), or the section 160ZZO roll - over mentioned in subparagraph ( 3)(a)(ii), a * capital gain of the originating company was disregarded or a capital gain of the transferor did not accrue--a reduction amount equal to the capital gain.

Apportionment of step 3A amount among first level interposed entities

(5) If at the linked entity joining time one or more linked entities, in which the * head company holds * membership interests, are interposed between the head company and the subject entity, then the step 3A amount is apportioned among those entities and the subject entity in the same way as a step 3A amount is apportioned under subsection ( 2).

Part 5 -- Technical corrections

Income Tax Assessment Act 1997

23 Subsection 701 - 25(4)

Omit ", and", substitute "and".

24 Subsection 701 - 45(3)

Omit " * head company", substitute "entity".

25 Subparagraph 701 - 75(3)(a)(ii)

Omit "time.", substitute "time; and".

26 Subsections 705 - 150(3) and (4)

Omit "reduced (if the head company roll - over adjustment amount is an excess), or increased", substitute "increased (if the head company roll - over adjustment is an excess), or reduced".

Income Tax (Transitional Provisions) Act 1997

27 Subsection 701 - 30(1)

Repeal the subsection, substitute:

Section only applies to transitional groups formed at certain times

(1) This section applies if the day on which the transitional group comes into existence is before 1 July 2003 or is both:

(a) the first day of the first income year of the head company starting after 30 June 2003; and

(b) before 1 July 2004.

Section only applies to non - chosen transitional entities in such groups

(1A) This section applies to each transitional entity in the transitional group, other than a chosen transitional entity. This is so even if there are no chosen transitional entities at all.

27A Paragraph 701 - 30(1)(a)

Repeal the paragraph, substitute:

(a) on or before the first day of the first income year of the head company starting after 30 June 2003; and

Income Tax (Transitional Provisions) Act 1997

28 Paragraph 701 - 20(5)(c)

Omit "in the sub - group held in any other", substitute "held at or before that time in any other entity that became a".

29 Paragraph 701 - 20(5)(c)

After "in relation to the sub - group", insert ", and any such entity held those membership interests during the period when it actually held them".

Part 8 -- Inclusion in certain transitional provisions of references to the Income Tax Assessment Act 1997

Income Tax (Transitional Provisions) Act 1997

30 Subsection 701 - 5(2)

After "703 - 50(3)", insert "of the Income Tax Assessment Act 1997 ".

31 Subsection 701 - 5(2)

After "section 703 - 50", insert "of that Act".

32 Section 701 - 15

After "amount)", insert "of the Income Tax Assessment Act 1997 ".

33 Section 701 - 15 (note)

After "701 - 5", insert "of that Act".

34 Paragraph 701 - 20(4)(b)

After "705 - 60", insert "of the Income Tax Assessment Act 1997 ".

35 Paragraph 701 - 20(5)(d)

After "705 - 60", insert "of the Income Tax Assessment Act 1997 ".

36 Section 701 - 25

Omit "this Act", substitute "the Income Tax Assessment Act 1997 ".