Commonwealth Consolidated Acts Commonwealth Consolidated Acts

Commonwealth Consolidated Acts Commonwealth Consolidated ActsPart 1 -- Amendments commencing on 1 July 2000

Income Tax Assessment Act 1936

1 At the end of section 160APHBF

Add:

(6) An exempt institution whose exempt status is disregarded under subsection 160ARDAB(1) cannot be a prescribed person in relation to a company under this section.

2 At the end of section 160APHBG

Add:

(10) An exempt institution whose exempt status is disregarded under subsection 160ARDAB(1) cannot be taken to be a prescribed person in relation to a company under this section.

Part 2 -- Amendments commencing on 29 June 2002

Income Tax Assessment Act 1997

3 Paragraph 204 - 30(6)(b)

Omit "207 - 40", substitute "207 - 35".

4 Section 205 - 15 (table item 4)

Omit "through a * partnership or trust", substitute "through a partnership or the trustee of a trust".

5 Subsections 207 - 5(3), (4) and (5)

Repeal the subsections, substitute:

(3) If a franked distribution is made to a member that is a partnership or the trustee of a trust, an amount equal to the franking credit on the distribution is also included in the member's assessable income as mentioned in paragraph ( 1)(a).

(4) However, a tax offset in relation to that distribution is only available to an entity (who may be a partner, beneficiary or a trustee) if the distribution flows indirectly to it and does not flow indirectly through it to another entity. The tax offset is equal to its share of the franking credit on the distribution.

Note: That share is a notional amount and the entity can have that share without actually receiving any of that franking credit or distribution.

(5) There are exceptions to both the general rule mentioned in subsection ( 1) and the special rule mentioned in subsection ( 4). Basically, these exceptions are created:

(a) where the relevant entity would not have paid tax on the distribution or a share of the distribution (see Subdivisions 207 - D and 207 - E); and

(b) where there is a manipulation of the imputation system in a manner that is not permitted under the income tax law (see Subdivision 207 - F).

6 Subsections 207 - 15(2) and (3)

Repeal the subsections ( including the notes), substitute:

(2) This Subdivision does not apply to:

(a) a partnership or trustee to whom a * franked distribution is made (except a partnership or trustee that is a * corporate tax entity, or a trustee of a trust that is a * complying superannuation entity, when the distribution is made); or

(b) an entity to whom a franked distribution * flows indirectly.

Note: Subject to the other provisions in this Division, Subdivision 207 - B applies to an entity excluded from the application of this Subdivision because of this subsection.

(3) This Subdivision applies subject to Subdivisions 207 - C, 207 - D, 207 - E and 207 - F.

Note 1: Subdivision 207 - C sets out the residency requirements that must be satisfied by an individual or a corporate tax entity that receives a franked distribution.

Note 2: Subdivision 207 - D sets out the cases in which the gross - up and tax offset rules in this Subdivision and Subdivision 207 - B will not apply because the franked distribution (or a share of it) would not have been taxed in any case.

Note 3: Subdivision 207 - E sets out the exceptions to the rules in Subdivision 207 - D.

Note 4: Subdivision 207 - F sets out the cases in which the gross - up and tax offset rules in this Subdivision and Subdivision 207 - B will not apply because the imputation system has been manipulated in a way that is not permitted under the income tax law.

7 Subdivision 207 - B

Repeal the Subdivision, substitute:

Subdivision 207 - B -- Franked distribution received through certain partnerships and trustees

207 - 25 What this Subdivision is about

This Subdivision deals with an entity that receives a benefit of a franked distribution where:

(a) the distribution is made to a partnership or the trustee of a trust; and

(b) the benefit is received either directly or through other interposed partnerships or trusts.

The distribution is regarded as flowing indirectly to the entity under this Subdivision.

On the basis of a notional amount of the entity's share of the distribution, the entity may be entitled to have an amount included in its assessable income and/or a tax offset under this Subdivision.

Table of sections

Gross - up and tax offset

207 - 30 Applying this Subdivision

207 - 35 Gross - up--distribution made to, or flows indirectly through, a partnership or trustee

207 - 45 Tax offset--distribution flows indirectly to an entity

Key concepts

207 - 50 When a franked distribution flows indirectly to or through an entity

207 - 55 Share of a franked distribution

207 - 57 Share of the franking credit on a franked distribution

[This is the end of the Guide.]

207 - 30 Applying this Subdivision

This Subdivision applies subject to Subdivisions 207 - D, 207 - E and 207 - F.

Note 1: Subdivision 207 - D sets out the cases in which the gross - up and tax offset rules in this Subdivision and Subdivision 207 - A will not apply because the franked distribution (or a share of it) would not have been taxed in any case.

Note 2: Subdivision 207 - E sets out the exceptions to the rules in Subdivision 207 - D.

Note 3: Subdivision 207 - F sets out the cases in which the gross - up and tax offset rules in this Subdivision and Subdivision 207 - A will not apply because the imputation system has been manipulated in a way that is not permitted under the income tax law.

207 - 35 Gross - up--distribution made to, or flows indirectly through, a partnership or trustee

Additional amount of assessable income

(1) If:

(a) a * franked distribution is made in an income year to an entity that is a partnership or the trustee of a trust; and

(b) the entity is not a * corporate tax entity when the distribution is made; and

(c) if the entity is the trustee of a trust--the trust is not a * complying superannuation entity when the distribution is made;

the assessable income of the partnership or trust for that income year includes the amount of the * franking credit on the distribution.

(2) The amount is in addition to any other amount included in that assessable income in relation to the distribution under any other provision of this Act.

Note: The amount will affect the income tax liability of a partner in the partnership, or a beneficiary or the trustee of the trust: see Divisions 5 and 6 of Part III of the Income Tax Assessment Act 1936 .

Allocation of the additional amount of assessable income

(3) Despite any provisions in Divisions 5 and 6 of Part III of the Income Tax Assessment Act 1936 , if:

(a) a * franked distribution is made, or * flows indirectly, to a partnership or the trustee of a trust in an income year; and

(b) the assessable income of the partnership or trust for that year includes an amount (the franking credit amount ) that is all or a part of the additional amount of assessable income included under subsection ( 1) in relation to the distribution; and

(c) the distribution flows indirectly to an entity that is a partner in the partnership, or a beneficiary or that trustee of the trust; and

(d) the entity has an amount of assessable income for that year that is attributable to all or a part of the distribution;

then, the entity's assessable income for that year also includes so much of the franking credit amount as is equal to its * share of the * franking credit on the distribution.

Example: A franked distribution of $70 is made to the trustee of a trust in an income year. The trust also has $100 of assessable income from other sources. Under subsection ( 1), the trust's assessable income includes an additional amount of $30 (which is the franking credit on the distribution). The trust has a net income of $200 for that income year.

There are 2 beneficiaries of the trust, P and Q, who are presently entitled to the trust's income. Under the trust deed, P is entitled to all of the franked distribution and Q is entitled to all other income.

The distribution flows indirectly to P (as P is entitled to a share of that net income and has a 100% share of the distribution under section 207 - 55). P therefore has an amount of assessable income that is equal to its share of the distribution. Under this subsection, P's assessable income also includes the full amount of the franking credit (as P's share of the franking credit on the distribution is $30 under section 207 - 57). Q's share of the net income therefore does not include any of the franking credit.

207 - 45 Tax offset--distribution flows indirectly to an entity

An entity to whom a * franked distribution * flows indirectly in an income year is entitled to a * tax offset for that income year that is equal to its * share of the * franking credit on the distribution, if it is:

(a) an individual; or

(b) a * corporate tax entity when the distribution flows indirectly to it; or

(c) the trustee of a trust that is liable to be assessed on a share of, or all or a part of, the trust's * net income under section 98, 99 or 99A of the Income Tax Assessment Act 1936 for that income year; or

(d) the trustee of an eligible entity within the meaning of Part IX of that Act in relation to that income year.

Note 1: Certain superannuation funds, ADFs and PSTs are eligible entities within the meaning of Part IX of the Income Tax Assessment Act 1936 .

Note 2: The entities covered by this section are the ultimate recipients of the distribution because the distribution does not flow indirectly through them to other entities. As a result they are also the ultimate taxpayers in respect of the distribution and are given the tax offset to acknowledge the income tax that has already been paid on the profits underlying the distribution.

207 - 50 When a franked distribution flows indirectly to or through an entity

(1) For the purposes of this Subdivision, this section sets out the only circumstances in which a * franked distribution:

(a) flows indirectly to an entity ( subsection ( 2), (3) or (4)); or

(b) flows indirectly through an entity ( subsection ( 5)).

Partners

(2) A * franked distribution flows indirectly to a partner in a partnership in an income year if, and only if:

(a) during that income year, the distribution is made to the partnership, or * flows indirectly to the partnership as a beneficiary because of a previous application of subsection ( 3); and

(b) the partner has an individual interest:

(i) in the partnership's * net income for that income year that is covered by paragraph 92(1)(a) or (b) of the Income Tax Assessment Act 1936 ; or

(ii) in a * partnership loss of the partnership for that income year that is covered by paragraph 92(2)(a) or (b) of that Act;

(whether or not that individual interest becomes assessable income in the hands of the partner); and

(c) the partner's * share of the distribution under section 207 - 55 is a positive amount (whether or not the partner actually receives any of that share).

Beneficiaries

(3) A * franked distribution flows indirectly to a beneficiary of a trust in an income year if, and only if:

(a) during that income year, the distribution is made to the trustee of the trust, or * flows indirectly to the trustee as a partner or beneficiary because of a previous application of subsection ( 2) or this subsection; and

(b) the beneficiary has this amount for that income year (the share amount ):

(i) a share of the trust's * net income for that income year that is covered by paragraph 97(1)(a) of the Income Tax Assessment Act 1936 ; or

(ii) an individual interest in the trust's net income for that income year that is covered by paragraph 98A(1)(a) or (b), or paragraph 100(1)(a) or (b), of that Act;

(whether or not the share amount becomes assessable income in the hands of the beneficiary); and

(c) the beneficiary's * share of the distribution under section 207 - 55 is a positive amount (whether or not the beneficiary actually receives any of that share).

Trustees

(4) A * franked distribution flows indirectly to the trustee of a trust in an income year if, and only if:

(a) during that income year, the distribution is made to the trustee, or * flows indirectly to the trustee as a partner or beneficiary because of a previous application of subsection ( 2) or (3); and

(b) the trustee is liable or, but for another provision in this Act, would be liable, to be assessed in respect of an amount (the share amount ) that is:

(i) a share of the trust's * net income for that income year under section 98 of the Income Tax Assessment Act 1936 ; or

(ii) all or a part of the trust's net income for that income year under section 99 or 99A of that Act;

(whether or not the share amount becomes assessable income in the hands of the trustee); and

(c) the trustee's * share of the distribution under section 207 - 55 is a positive amount (whether or not the trustee actually receives any of that share).

Note: A trustee to whom a franked distribution flows indirectly under this subsection is entitled to a tax offset under section 207 - 45 and the distribution does not flow indirectly through the trustee to another entity.

(5) A * franked distribution flows indirectly through an entity (the first entity ) to another entity if, and only if:

(a) the other entity is the focal entity in an item of the table in section 207 - 55 in relation to the distribution; and

(b) that focal entity's * share of the distribution is based on the first entity's share of the distribution as an intermediary entity in that or another item of the table.

Example: A franked distribution of $140 is made to a partnership. An amount equal to the franking credit on the distribution ($60) is included in the partnership's assessable income under section 207 - 35. Because the partnership has losses of $300 from other sources, it has a partnership loss of $100 for the income year.

The partnership has 2 equal partners. One partner is the trustee of a trust and the other partner is an individual. The distribution flows indirectly to each partner under subsection ( 2). Each partner has a share of the partnership loss ($50), a share of the distribution under sections 207 - 55 ($70) and a share of the franking credit under section 207 - 57 ($30).

The individual partner is allowed a tax offset of $30 under section 207 - 45.

Because the trust has $100 of income from other sources, it has a net income of $50 for that income year ($100 minus the share of the partnership loss of $50).

The trust has one individual as a beneficiary, to whom the distribution flows indirectly under subsection ( 3). The beneficiary's share of the franked distribution is $70 under sections 207 - 55 and its share of the franking credit is $30 under section 207 - 57. The beneficiary is therefore allowed a tax offset of $30 under section 207 - 45.

207 - 55 Share of a franked distribution

Object of section

(1) The object of this section is to ensure that:

(a) the amount of a * franked distribution made to a partnership or the trustee of a trust is allocated notionally amongst entities who derive benefits from that distribution; and

(b) that allocation corresponds with the way in which those benefits were derived.

Note: An entity can derive a benefit from the distribution (and therefore has a share of the distribution) without actually receiving any of the distribution: see subsection ( 2) of this section and the example at the end of section 207 - 50.

(2) An entity's share of a * franked distribution is an amount notionally allocated to the entity as its share of the distribution, whether or not the entity actually receives any of that distribution.

(3) That amount is equal to the entity's share of the distribution as the focal entity in column 3 of an item of the table.

Note: An entity's share of the distribution is based on the share of the distribution of each preceding intermediary entity through which the distribution flows, starting from the intermediary entity to whom the distribution is made.

This means that in some cases (see items 2 and 4), more than one item of the table will need to be applied to work out the share of the distribution of an ultimate recipient of the distribution.

Share of a franked distribution | |||

Item | Column 1 For this intermediary entity and this focal entity : | Column 2 The intermediary entity's share of the franked distribution is: | Column 3 The focal entity's share of the franked distribution is: |

1 | a partnership is the intermediary entity and a partner in that partnership is the focal entity if: (a) a * franked distribution is made to the partnership; and (b) the partner has, in respect of the partnership, an individual interest mentioned in subsection 207 - 50(2) | the amount of the franked distribution | so much of the franked distribution as is taken into account in working out the amount of that individual interest |

2 | a partnership is the intermediary entity and a partner in that partnership is the focal entity if: (a) a * franked distribution * flows indirectly to the partnership as a beneficiary of a trust; and (b) the partner has, in respect of the partnership, an individual interest mentioned in subsection 207 - 50(2) | the amount worked out under column 3 of item 3 or 4 of this table where the partnership, as a beneficiary, is the focal entity in that item | so much of the amount worked out under column 2 of this item as is attributable to the partner, having regard to the partnership agreement and any other relevant circumstances |

3 | the trustee of a trust is the intermediary entity and the trustee or a beneficiary of the trust is the focal entity if: (a) a * franked distribution is made to the trustee; and (b) the trustee or beneficiary has, in respect of the trust, a share amount mentioned in subsection 207 - 50(3) or (4) | (a) if the trust has a positive amount of * net income for that year--the amount of the franked distribution; or (b) otherwise--nil | so much of the amount worked out under column 2 of this item as is taken into account in working out that share amount |

4 | the trustee of a trust is the intermediary entity and the trustee or a beneficiary of the trust is the focal entity if: (a) a * franked distribution * flows indirectly to the trustee as a partner in a partnership or as a beneficiary of another trust; and (b) the trustee or beneficiary has, in respect of the trust, a share amount mentioned in subsection 207 - 50(3) or (4) | the amount worked out under column 3 of: (a) item 1 or 2 of this table where the trustee, as a partner, is the focal entity in that item; or (b) item 3 or a previous application of this item where the trustee, as a beneficiary, is the focal entity in that item | so much of the amount worked out under column 2 of this item as is attributable to the focal entity in this item, having regard to the trust deed and any other relevant circumstances |

Note: In item 3 or 4, the trustee of a trust can be both the intermediary entity and the focal entity in the same item.

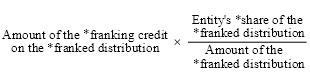

207 - 57 Share of the franking credit on a franked distribution

(1) An entity's share of a * franking credit on a * franked distribution is an amount notionally allocated to the entity as its share of that credit, whether or not the entity actually receives any of that credit or distribution.

(2) Work out that amount as follows:

8 Subdivision 207 - D

Repeal the Subdivision, substitute:

Subdivision 207 - D -- No gross - up or tax offset where distribution would not be taxed

207 - 80 What this Subdivision is about

This Subdivision creates the appropriate adjustment to cancel the effect of the gross - up and tax offset rules where a franked distribution (or a share of it) is, or would be, exempt income or an amount that is neither assessable income nor exempt income in the relevant entity's hands (and therefore would not be taxed in any case).

Table of sections

Operative provisions

207 - 85 Applying this Subdivision

207 - 90 Distribution that is made to an entity

207 - 95 Distribution that flows indirectly to an entity

207 - 85 Applying this Subdivision

This Subdivision applies subject to Subdivisions 207 - E and 207 - F.

Note 1: Subdivision 207 - E sets out exceptions to the rules in this Subdivision.

Note 2: Where both this Subdivision and Subdivision 207 - F apply to an entity, the application of this Subdivision is subject to the rules in Subdivision 207 - F: see subsections 207 - 145(3) and 207 - 150(7) and (8).

207 - 90 Distribution that is made to an entity

Whole of distribution not assessable

(1) If:

(a) a * franked distribution is made to an entity; and

(b) the distribution does not * flow indirectly through the entity to another entity; and

(c) the distribution is * exempt income or an amount that is neither assessable income nor exempt income in the hands of the entity;

then, for the purposes of this Act:

(d) the amount of the * franking credit on the distribution is not included in the assessable income of the entity under section 207 - 20; and

(e) the entity is not entitled to a * tax offset under this Division because of the distribution.

Part of distribution not assessable

(2) If:

(a) a * franked distribution is made to an entity; and

(b) the distribution does not * flow indirectly through the entity to another entity; and

(c) a part of the distribution (the relevant part ) is * exempt income or an amount that is neither assessable income nor exempt income in the hands of the entity;

then, for the purposes of this Act:

(d) the amount of the distribution is taken to have been reduced by the relevant part; and

(e) the amount of the * franking credit on the distribution is to be worked out as follows:

207 - 95 Distribution that flows indirectly to an entity

Whole of share of distribution not assessable

(1) If:

(a) a * franked distribution * flows indirectly to an entity in an income year; and

(b) the entity's * share of the distribution would, in its hands, be * exempt income or an amount that is neither assessable income nor exempt income (whether or not it had actually received that share);

then, for the purposes of this Act:

(c) subsection ( 2), (3) or (4) (as appropriate) applies to the entity in relation to that income year; and

(d) the entity is not entitled to a * tax offset under this Division because of the distribution; and

(e) if the distribution flows indirectly through the entity to another entity--subsection 207 - 35(3) and section 207 - 45 do not apply to that other entity.

Note: This section can therefore apply, for example, where the entity is a partner in a partnership that has a partnership loss and the entity does not actually receive any of the distribution.

Partner

(2) If the * franked distribution * flows indirectly to the entity as a partner in a partnership under subsection 207 - 50(2), the entity can deduct an amount for that income year that is equal to its * share of the * franking credit on the distribution.

Beneficiary

(3) If the * franked distribution * flows indirectly to the entity as a beneficiary of a trust under subsection 207 - 50(3), the entity can deduct an amount for that income year that is equal to the lesser of:

(a) its share amount in relation to the distribution that is mentioned in that subsection; and

(b) its * share of the * franking credit on the distribution.

Trustee

(4) If the * franked distribution * flows indirectly to the entity as the trustee of a trust under subsection 207 - 50(4), the entity's share amount in relation to the distribution that is mentioned in that subsection is to be reduced by the lesser of:

(a) that share amount; and

(b) its * share of the * franking credit on the distribution.

Example: A franked distribution of $70 is made to a partnership.

Under section 207 - 35, an additional amount of $30 is included in the partnership's assessable income because of the distribution.

The partnership has 2 equal partners, X and Y. X is a non - resident individual whose share of partnership's net income for the income year is $50 (share of distribution of $35 and share of franking credit of $15). That share of distribution is not assessable income and not exempt income under section 128D of the Income Tax Assessment Act 1936 .

X's assessable income of $15 (share of franking credit) is reduced to nil because of the deduction of $15 under subsection ( 2). Because of subsection ( 1), X is not entitled to a tax offset under section 207 - 45.

Part of share of distribution not assessable

(5) If:

(a) a * franked distribution * flows indirectly to an entity in an income year; and

(b) a part of the entity's * share of the distribution (the relevant part ) would, in its hands, be * exempt income or an amount that is neither assessable income nor exempt income (whether or not it had actually received that part);

then, subsection ( 2), (3) or (4) (as appropriate) applies to the entity on the basis that the amount of its * share of the * franking credit on the distribution is worked out as follows:

(6) In addition, the following apply to an entity covered by subsection ( 5):

(a) if the distribution would otherwise * flow indirectly through the entity--the entity's * share of the distribution for the purposes of this Act (other than subsection ( 2), (3) or (4)) is to be reduced by the relevant part mentioned in subsection ( 5);

(b) if the entity would otherwise be entitled to a * tax offset under this Subdivision because of the distribution--the amount of the tax offset is to be worked out as follows:

9 Subdivision 207 - E (heading)

Repeal the heading, substitute:

Subdivision 207 - E -- Exceptions to the rules in Subdivision 207 - D

10 Section 207 - 105

Repeal the section, substitute:

207 - 105 What this Subdivision is about

Subdivision 207 - D does not apply to certain exempt institutions, trusts and life insurance companies as set out in this Subdivision. Such an entity may be entitled to a tax offset under this Subdivision in relation to a franked distribution.

11 Sections 207 - 110, 207 - 115, 207 - 120 and 207 - 125

Repeal the sections, substitute:

207 - 110 Exceptions to sections 207 - 90 and 207 - 95

(1) This section applies to an entity to whom a * franked distribution is made, or * flows indirectly, in any of the following circumstances:

(a) the entity is an * exempt institution that is eligible for a refund and the distribution does not flow indirectly to the entity as a partner in a partnership under subsection 207 - 50(2);

(b) the distribution is, or the entity's * share of the distribution would have been, this kind of income in its hands:

(i) * exempt income under section 282B, 283 or 297B of the Income Tax Assessment Act 1936 (certain income derived by an eligible entity within the meaning of Part IX of that Act); or

(ii) an amount that is neither assessable income nor exempt income under paragraph 320 - 37(1)(a) (segregated exempt assets of a life insurance company) or paragraph 320 - 37(1)(d) (certain amounts received by a friendly society) of this Act.

(2) The following have effect in relation to the entity:

(a) section 207 - 90 or 207 - 95 (as appropriate) does not apply to the entity;

(b) if the entity would, apart from section 207 - 90 or 207 - 95, be entitled to a * tax offset under section 207 - 20 or 207 - 45 in relation to the distribution--the entity is entitled to that tax offset;

(c) if the entity would not be entitled to such a tax offset, the entity is entitled to a tax offset under this section that is equal to:

(i) if the distribution is made to the entity--the * franking credit on the distribution; or

(ii) if the distribution * flows indirectly to the entity--the entity's * share of the franking credit on the distribution;

(d) if the distribution flows indirectly through the entity to another entity--subsection 207 - 35(3) and section 207 - 45 do not apply to that other entity.

Note: Paragraph ( 2)(c) only applies to an exempt institution that is eligible for a refund and that is not entitled to a tax offset under section 207 - 20 or 207 - 45. An entity covered by paragraph ( 1)(b) will, in all cases, be entitled to a tax offset under section 207 - 20 or 207 - 45.

12 Before section 207 - 130

Insert:

13 Section 207 - 140

Repeal the section, substitute:

207 - 140 What this Subdivision is about

This Subdivision creates the appropriate adjustment to cancel the effect of the gross - up and tax offset rules where the entity concerned has manipulated the imputation system in a manner that is not permitted under the income tax law.

14 Sections 207 - 145 and 207 - 150

Repeal the sections, substitute:

207 - 145 Distribution that is made to an entity

Whole of distribution manipulated

(1) If a * franked distribution is made to an entity in one or more of the following circumstances:

(a) the entity is not a qualified person in relation to the distribution for the purposes of Division 1A of Part IIIAA of the Income Tax Assessment Act 1936 ;

(b) the Commissioner has made a determination under paragraph 177EA(5)(b) of that Act that no imputation benefit (within the meaning of that section) is to arise in respect of the distribution for the entity;

(c) the Commissioner has made a determination under paragraph 204 - 30(3)(c) of this Act that no * imputation benefit is to arise in respect of the distribution for the entity;

(d) the distribution is made as part of a * dividend stripping operation;

then, for the purposes of this Act:

(e) the amount of the * franking credit on the distribution is not included in the assessable income of the entity under section 207 - 20 or 207 - 35; and

(f) the entity is not entitled to a * tax offset under this Subdivision because of the distribution; and

(g) if the distribution * flows indirectly through the entity to another entity--subsection 207 - 35(3) and section 207 - 45 do not apply to that other entity.

Part of share of distribution manipulated

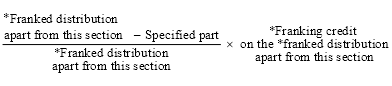

(2) If:

(a) a * franked distribution is made to an entity; and

(b) the Commissioner makes a determination under paragraph 177EA(5)(b) of the Income Tax Assessment Act 1936 that no imputation benefit (within the meaning of that section) is to arise in respect of a specified part of the distribution (the specified part ) for the entity;

then, for the purposes of this Act:

(c) the amount of the distribution is taken to have been reduced by the specified part; and

(d) the amount of the * franking credit on the distribution is to be worked out as follows:

Example: A franked distribution of $70 is made to the trustee of a trust. Apart from this section, the franking credit on the distribution ($30) would be included in the assessable income of the trust under section 207 - 35.

The Commissioner has made a determination under paragraph 177EA(5)(b) of the Income Tax Assessment Act 1936 that no imputation benefit (within the meaning of that section) is to arise for the trustee in respect of $49 of the distribution.

Under this subsection, the amount included in the assessable income of the trust under section 207 - 35 because of the distribution is reduced from $30 to $9.

If there is a beneficiary of the trust that is presently entitled to the trust's income, the amount of the distribution that flows indirectly to the beneficiary is reduced from $70 to $21 under this subsection.

What happens if both subsection 207 - 90(2) and subsection ( 2) of this section would apply

(3) If, apart from this subsection, both subsection 207 - 90(2) and subsection ( 2) of this section would apply to an entity in relation to a * franked distribution, then:

(a) apply subsection 207 - 90(2) first; and

(b) apply subsection ( 2) of this section on the basis that the amount of the * franked distribution had been reduced under subsection 207 - 90(2).

207 - 150 Distribution that flows indirectly to an entity

Whole of share of distribution manipulated

(1) If a * franked distribution * flows indirectly to an entity in an income year in one or more of the following circumstances:

(a) the entity is not a qualified person in relation to the distribution for the purposes of Division 1A of Part IIIAA of the Income Tax Assessment Act 1936 ;

(b) the Commissioner has made a determination under paragraph 177EA(5)(b) of that Act that no imputation benefit (within the meaning of that section) is to arise in respect of the distribution for the entity;

(c) the Commissioner has made a determination under paragraph 204 - 30(3)(c) of this Act that no * imputation benefit is to arise in respect of the distribution for the entity;

(d) the distribution is treated as an interest payment for the entity under section 207 - 160 of this Act;

(e) the distribution is made as part of a * dividend stripping operation;

then, for the purposes of this Act:

(f) subsection ( 2), (3) or (4) (as appropriate) applies to the entity in relation to that income year; and

(g) the entity is not entitled to a * tax offset under this Subdivision because of the distribution; and

(h) if the distribution * flows indirectly through the entity to another entity--subsection 207 - 35(3) and section 207 - 45 do not apply to that other entity.

Partner

(2) If the * franked distribution * flows indirectly to the entity as a partner in a partnership under subsection 207 - 50(2), the entity can deduct an amount for that income year that is equal to its * share of the * franking credit on the distribution.

Beneficiary

(3) If the * franked distribution * flows indirectly to the entity as a beneficiary of a trust under subsection 207 - 50(3), the entity can deduct an amount for that income year that is equal to the lesser of:

(a) its share amount in relation to the distribution that is mentioned in that subsection; and

(b) its * share of the * franking credit on the distribution.

Trustee

(4) If the * franked distribution * flows indirectly to the entity as the trustee of a trust under subsection 207 - 50(4), the entity's share amount in relation to the distribution that is mentioned in that subsection is to be reduced by the lesser of:

(a) that share amount; and

(b) its * share of the * franking credit on the distribution.

Part of share of distribution manipulated

(5) If:

(a) a * franked distribution * flows indirectly to an entity in an income year; and

(b) the Commissioner has made a determination under paragraph 177EA(5)(b) of the Income Tax Assessment Act 1936 that no imputation benefit (within the meaning of that section) is to arise in respect of a specified part of the distribution (the specified part ) for the entity;

then, subsection ( 2), (3) or (4) (as appropriate) applies to the entity on the basis that the amount of its * share of the * franking credit on the distribution is worked out as follows:

(6) In addition, the following apply to an entity covered by subsection ( 5):

(a) if the distribution would otherwise * flow indirectly through the entity--the entity's * share of the distribution for the purposes of this Act (other than subsection ( 2), (3) or (4)) is to be reduced by the specified part mentioned in subsection ( 5);

(b) if the entity would otherwise be entitled to a * tax offset under this Subdivision because of the distribution--the amount of the tax offset is to be worked out as follows:

Example: X is a partner in a partnership to which a franked distribution of $140 is made. The franking credit on the distribution ($60) is included in the assessable income of the partnership under section 207 - 35. X's share of the distribution is $70 and its share of the franking credit on the distribution is $30.

The Commissioner has made a determination under paragraph 177EA(5)(b) of the Income Tax Assessment Act 1936 that no imputation benefit (within the meaning of that section) is to arise for X in respect of $42 of the distribution.

Under subsection ( 5), X will be allowed a deduction of $18.

X is the trustee of a trust and the distribution will flow indirectly through X to beneficiaries of the trust. For the purposes of working out a beneficiary's share of the distribution and its share of the franking credit, X's share of the franked distribution is reduced to $28 under this subsection.

What happens if both subsection 207 - 95(1) and subsection ( 1) of this section would apply

(7) If, apart from this subsection, both subsection 207 - 95(1) and subsection ( 1) of this section would apply to an entity in relation to a * franked distribution, then:

(a) subsection ( 1) of this section applies to the entity; but

(b) subsection 207 - 95(1) does not apply to the entity.

What happens if both subsection 207 - 95(5) and subsection ( 5) of this section would apply

(8) If, apart from this subsection, both subsection 207 - 95(5) and subsection ( 5) of this section would apply to an entity in relation to a * franked distribution, then:

(a) apply subsections 207 - 95(5) and (6) first; and

(b) apply subsections ( 5) and (6) of this section on the basis that:

(i) the amount of the entity's * share of the * franking credit on the distribution had been reduced under subsection 207 - 95(5); and

(ii) the amount of the entity's * share of the distribution had been reduced under subsection 207 - 95(6).

15 Sections 207 - 160, 207 - 165 and 207 - 170

Repeal the sections, substitute:

207 - 160 Distribution that is treated as an interest payment

(1) For the purposes of this Subdivision, a * franked distribution is treated as an interest payment for an entity to whom the distribution * flows indirectly if:

(a) all or a part of the entity's individual interest or share amount in relation to the distribution that is mentioned in subsection 207 - 50(2), (3) or (4) could reasonably be regarded as the payment of interest on a loan, having regard to:

(i) the way in which that individual interest or share amount was calculated; and

(ii) the conditions applying to the payment or application of that individual interest or share amount; and

(iii) any other relevant matters; and

(b) the entity's interest in the last intermediary entity (see subsection ( 2)):

(i) was acquired, or was acquired for a period that was extended, at or after 7.30 pm by legal time in the Australian Capital Territory on 13 May 1997; or

(ii) was acquired as part of a * financing arrangement for the entity (including an arrangement extending to an earlier arrangement) that was entered into at or after that time.

(2) The entity's interest in the last intermediary entity is:

(a) if the distribution * flows indirectly to the entity as a partner in a partnership under subsection 207 - 50(2)--the entity's interest in the partnership; or

(b) if the distribution flows indirectly to the entity as a beneficiary of a trust under subsection 207 - 50(3)--the entity's interest in the trust; or

(c) if the distribution flows indirectly to the entity as the trustee of a trust under subsection 207 - 50(4)--the entity's interest in the trust in respect of which the entity is liable to be assessed.

16 At the end of section 208 - 40

Add:

(6) An * exempt institution that is eligible for a refund cannot be a prescribed person in relation to a * corporate tax entity under this section.

17 At the end of section 208 - 45

Add:

(10) An * exempt institution that is eligible for a refund cannot be taken to be a prescribed person in relation to a * corporate tax entity under this section.

18 Section 208 - 175

Omit "section 207 - 35", substitute "section 207 - 50".

19 Section 208 - 180

Omit "section 207 - 55", substitute "sections 207 - 55 and 207 - 57".

20 Subsection 995 - 1(1) ( paragraphs ( a) and (b) of the definition of flows indirectly )

Repeal the paragraphs, substitute:

(a) subsections 207 - 50(2), (3) and (4) set out the circumstances in which a * franked distribution flows indirectly to an entity; and

(b) subsection 207 - 50(5) sets out the circumstances in which a franked distribution flows indirectly through an entity; and

21 Subsection 995 - 1(1)

Insert:

"share" of a * franked distribution has the meaning given by section 207 - 55.

22 Subsection 995 - 1(1) ( paragraph ( a) of the definition of share )

Omit "207 - 55", substitute "207 - 57".

Part 3 -- Amendments commencing on 30 June 2003

Income Tax Assessment Act 1997

23 Subsection 67 - 25(1B)

Repeal the subsection, substitute:

(1B) If:

(a) the trustee of a trust to whom a * franked distribution * flows indirectly under subsection 207 - 50(4) is entitled to a * tax offset under Division 207 for an income year because of the distribution; and

(b) the trustee is liable to be assessed under section 98 or 99A of the Income Tax Assessment Act 1936 on a share of, or all or a part of, the trust's * net income for that income year;

the tax offset is not subject to the refundable tax offset rules.

24 Section 207 - 80

Omit "an amount that is neither assessable income nor exempt income", substitute " * non - assessable non - exempt income".

25 Paragraph 207 - 90(1)(c)

Omit "an amount that is neither assessable income nor exempt income", substitute " * non - assessable non - exempt income".

26 Paragraph 207 - 90(2)(c)

Omit "an amount that is neither assessable income nor exempt income", substitute " * non - assessable non - exempt income".

27 Paragraph 207 - 95(1)(b)

Omit "an amount that is neither assessable income nor exempt income", substitute " * non - assessable non - exempt income".

28 Paragraph 207 - 95(5)(b)

Omit "an amount that is neither assessable income nor exempt income", substitute " * non - assessable non - exempt income".

29 Subparagraph 207 - 110(1)(b)(ii)

Omit "an amount that is neither assessable income nor exempt income", substitute " * non - assessable non - exempt income".

30 Paragraph 220 - 400(1)(b)

Repeal the paragraph, substitute:

(b) an amount is included in the recipient's assessable income for the income year under section 207 - 20, and the recipient is entitled to a * tax offset for the income year under that section or section 207 - 110; and

31 Paragraph 220 - 400(1)(c)

Omit "and".

32 Paragraph 220 - 400(1)(d)

Repeal the paragraph.

33 Subsection 220 - 400(2)

After "assessable income", insert "under section 207 - 20".

34 Subsection 220 - 400(3)

After " * tax offset", insert "under section 207 - 20".

35 Subsections 220 - 400(4) and (5)

Repeal the subsections, substitute:

What happens if certain provisions apply

(4) Subsections ( 2) and (3) do not apply to the recipient in relation to the * franked distribution if one or more of the following provisions also apply to the recipient in relation to the distribution:

(a) subsection 207 - 90(1);

(b) subsection 207 - 90(2);

(c) subsection 207 - 145(1);

(d) subsection 207 - 145(2).

(5) If subsection 207 - 90(2) or 207 - 145(2) would also apply to the recipient in relation to the * franked distribution, apply that subsection on the basis that:

(a) the amount of the * franking credit on the distribution;

had been reduced by:

(b) so much of the supplementary dividend as does not exceed that amount of the franking credit.

Relationship with sections 207 - 20, 207 - 90 and 207 - 145

(6) Sections 207 - 20, 207 - 90 and 207 - 145 have effect subject to this section.

36 Section 220 - 405 (heading)

Repeal the heading, substitute:

220 - 405 Franked distribution and supplementary dividend flowing indirectly

37 Paragraph 220 - 405(1)(c)

Omit "section 207 - 50", substitute "section 207 - 45".

38 Paragraph 220 - 405(1)(d)

Omit "and".

39 Paragraph 220 - 405(1)(e)

Repeal the paragraph.

40 Subsections 220 - 405(2) to (8)

Repeal the subsections ( including the notes), substitute:

Recipient that is a partner or beneficiary

(2) If the * franked distribution * flows indirectly to the recipient under subsection 207 - 50(2) or (3), then:

(a) the recipient can deduct an amount for the income year that is equal to so much of its share of the supplementary dividend as does not exceed:

(i) if the distribution flows indirectly to the recipient under subsection 207 - 50(2)--the recipient's individual interest in relation to the distribution that is mentioned in that subsection; or

(ii) if the distribution flows indirectly to the recipient under subsection 207 - 50(3)--the recipient's share amount in relation to the distribution that is mentioned in that subsection; and

(b) the recipient's * tax offset under section 207 - 45 is reduced by so much of the deduction under paragraph ( a) as does not exceed its * share of the * franking credit on the distribution.

Recipient that is a trustee

(3) If the * franked distribution * flows indirectly to the recipient under subsection 207 - 50(4), then:

(a) the share amount mentioned in that subsection in relation to the distribution is reduced by so much of the recipient's share of the supplementary dividend as does not exceed that share amount; and

(b) the recipient's * tax offset under section 207 - 45 is reduced by so much of the reduction under paragraph ( a) as does not exceed its * share of the * franking credit on the distribution.

What happens if certain provisions apply

(4) Subsection ( 2) or (3) (as appropriate) does not apply to the recipient in relation to the * franked distribution if one or more of the following provisions also apply to the recipient in relation to the distribution:

(a) subsection 207 - 95(1);

(b) subsection 207 - 95(5);

(c) subsection 207 - 150(1);

(d) subsection 207 - 150(5).

(5) If subsection 207 - 90(5) or 207 - 150(5) would also apply to the recipient in relation to the * franked distribution, apply that subsection on the basis that:

(a) the amount of the recipient's * share of the * franking credit on the distribution;

had been reduced by:

(b) so much of the recipient's share of the supplementary dividend as does not exceed the amount of that share of the franking credit.

When does a supplementary dividend flow to an entity?

(6) A supplementary dividend flows indirectly to an entity if it would have * flowed indirectly to the entity under subsection 207 - 50(2), (3) or (4), if:

(a) the dividend had been a * franked distribution; and

(b) a reference in that subsection to the entity's * share of the franked distribution had been a reference to the entity's share of the supplementary dividend.

Share of supplementary dividend

(7) The entity's share of the supplementary dividend is worked out as follows:

(8) Nothing in this section has the effect of including in the entity's assessable income its share of the supplementary dividend.

Relationship with Subdivisions 207 - B, 207 - D, 207 - E and 207 - F

(9) Subdivisions 207 - B, 207 - D, 207 - E and 207 - F have effect subject to this section.

Income Tax Assessment Act 1997

41 Subsection 219 - 15(2) (table item 6)

Omit "through a * partnership or trust", substitute "through a partnership or the trustee of a trust".

42 Subsection 220 - 410(2)

Repeal the subsection ( including the note), substitute:

(2) The following provisions have effect subject to this section:

(a) items 3 and 4 of the table in section 205 - 15;

(b) items 5 and 6 of the table in section 219 - 15.

Note: Each of those items gives rise to a franking credit for a franked distribution if the recipient is entitled under Division 207 to a tax offset for the distribution. Those items provide that the amount of the credit equals the amount of that offset.

Part 5 -- Application and transitional provisions

43 Application provisions

(1) The amendments made by items 1 and 2 of this Schedule apply in relation to an exempt institution whose exempt status is disregarded under section 160ARDAB of the Income Tax Assessment Act 1936 on or after 1 July 2000.

(2) Subject to the rules on the application of Part 3 - 6 of the Income Tax Assessment Act 1997 set out in the Income Tax (Transitional Provisions) Act 1997 , the amendments made by the following items of this Schedule apply to events that occur on or after 1 July 2002:

(a) items 3 to 23;

(b) item 29;

(c) item 41.

(3) The amendments made by items 24 to 28 of this Schedule apply to assessments for the 2003 - 04 income year and later income years.

(4) Subject to the rules on the application of Part 3 - 6 of the Income Tax Assessment Act 1997 set out in the Income Tax (Transitional Provisions) Act 1997 , the amendments made by the following items of this Schedule apply in relation to things happening on or after 1 April 2003:

(a) items 30 to 40;

(b) item 42.

44 Transitional provision

Subparagraph 207 - 110(1)(b)(ii) of the Income Tax Assessment Act 1997 as amended by item 29 of this Schedule has effect during the period starting on 1 July 2002 and ending just before the start of the 2003 - 04 income year as if the reference in that subparagraph to an amount being non - assessable non - exempt income were a reference to the amount being neither assessable income nor exempt income.