Commonwealth Consolidated Acts Commonwealth Consolidated Acts

Commonwealth Consolidated Acts Commonwealth Consolidated ActsPart 1 -- The rewritten share capital tainting rules

Income Tax Assessment Act 1997

1 At the end of Part 3 - 5

Add:

Division 197 -- Tainted share capital accounts

Table of Subdivisions

Guide to Division 197

197 - A What transfers into a company's share capital account does this Division apply to?

197 - B Consequence of transfer: franking debit arises

197 - C Consequence of transfer: tainting of share capital account

197 - 1 What this Division is about

This Division:

(a) applies to certain amounts transferred to a company's share capital account (see Subdivision 197 - A); and

(b) provides for a franking debit to arise if such an amount is transferred to the share capital account (see Subdivision 197 - B); and

(c) provides for the tainting of the share capital account if such an amount is transferred, for how the account may be untainted, and for consequences that flow from untainting the account (see Subdivision 197 - C).

Table of sections

197 - 5 Division generally applies to an amount transferred to share capital account from another account

197 - 10 Exclusion for amounts that could be identified as share capital

197 - 15 Exclusion for amounts transferred under debt/equity swaps

197 - 20 Exclusion for amounts transferred leading to there being no shares with a par value--non - Corporations Act companies

197 - 25 Exclusion for transfers from option premium reserves

197 - 30 Exclusion for transfers made in connection with demutualisations of non - insurance etc. companies

197 - 35 Exclusion for transfers made in connection with demutualisations of insurance etc. companies

197 - 40 Exclusion for post - demutualisation transfers relating to life insurance companies

(1) Subject to subsection (2), this Division applies to an amount (the transferred amount ) that is transferred to a company's * share capital account from another of the company's accounts, if the company was an Australian resident immediately before the time of the transfer.

Note: If a company has 2 or more share capital accounts, those accounts are taken to be a single account (see subsection 975 - 300(2)).

(2) The other provisions of this Subdivision may stop this Division from applying to some or all of the transferred amount. If those other provisions stop this Division from applying to only some of the transferred amount, this Division (other than this Subdivision) applies to the balance of the transferred amount as if only that balance of the amount had been transferred to the company's * share capital account.

197 - 10 Exclusion for amounts that could be identified as share capital

This Division does not apply to the transferred amount if it could, at all times before the transfer, be identified in the books of the company as an amount of share capital.

197 - 15 Exclusion for amounts transferred under debt/equity swaps

(1) Subject to subsection (2), this Division does not apply to the transferred amount if:

(a) the transfer is under an * arrangement under which:

(i) a person discharges, releases or otherwise extinguishes the whole or a part of a debt that the company owes to the person; and

(ii) the discharge, release or extinguishment is in return for the company issuing * shares (other than redeemable preference shares) in the company to the person; and

(b) the transfer is a credit to the * share capital account that is made because of the issue of the shares in return for the discharge, release or extinguishment of the debt.

(2) If the transferred amount exceeds the lesser of:

(a) the * market value of the * shares issued by the company; and

(b) so much of the debt as is discharged, released or extinguished in return for the shares;

subsection (1) does not stop this Division from applying to the amount of the excess.

This Division does not apply to the transferred amount if:

(a) immediately before the transfer of the amount, the company was not incorporated under the Corporations Act 2001 ; and

(b) the transfer is under, or in accordance with, a law of the Commonwealth, or of a State or Territory, that requires or allows either or both of the following to become part of the company's * share capital account:

(i) the company's share premium account;

(ii) the company's capital redemption reserve; and

(c) the transfer is made as part of a process that leads to there being no * shares in the company that have a par value; and

(d) the amount is transferred from the company's share premium account or capital redemption reserve.

197 - 25 Exclusion for transfers from option premium reserves

This Division does not apply to the transferred amount if:

(a) it is transferred from an option premium reserve of the company; and

(b) the transfer is because of the exercise of options to acquire * shares in the company; and

(c) premiums in respect of those options were credited to the option premium reserve.

(1) Subject to subsection (2), this Division does not apply to the transferred amount if:

(a) the amount is transferred in connection with a demutualisation of the company; and

(b) Division 326 in Schedule 2H to the Income Tax Assessment Act 1936 applies to the demutualisation; and

(c) the transfer occurs within the limitation period in relation to the demutualisation (see subsection 326 - 20(3) in that Schedule).

(2) If the sum of:

(a) the transferred amount; and

(b) any other amounts that were previously transferred to the company's * share capital account, from another account of the company, in connection with the demutualisation;

exceeds the total capital contributions amount described in whichever of subsections (3) and (4) applies, subsection (1) does not stop this Division from applying to so much of the transferred amount as equals the lesser of the transferred amount and the amount of the excess.

Note: If there are several transfers of amounts to the company's share capital account in connection with the demutualisation, this section must be applied separately in relation to each transferred amount, in the order in which the transfers are made.

(3) If the company was not formed by the merger of 2 or more mutual entities, the total capital contributions amount referred to in subsection (2) is the sum of all the capital amounts:

(a) that were contributed to the company by * members of the company before its demutualisation; and

(b) in respect of which deductions are not allowable to the members; and

(c) that were not payments for goods or services provided by the company.

(4) If the company was formed by the merger of 2 or more mutual entities, the total capital contributions amount referred to in subsection (2) is the sum of:

(a) all the capital amounts:

(i) that were contributed to the company, before its demutualisation, by persons who became * members of the company at or after the time when the merger took place; and

(ii) in respect of which deductions are not allowable to those members; and

(iii) that were not payments for goods or services provided by the company; and

(b) the * market values, at the time of the merger, of the entities that merged to form the company, as determined by a qualified valuer.

(1) Subject to subsection (2), this Division does not apply to the transferred amount if:

(a) the amount is transferred in connection with the demutualisation of a company; and

(b) the demutualisation is implemented in accordance with a demutualisation method specified in Division 9AA of Part III of the Income Tax Assessment Act 1936 ; and

(c) the transfer occurs within the listing period in relation to the demutualisation (see subsection 121AE(6) of that Act); and

(d) the company (the issuing company ) to whose * share capital account the amount is transferred is:

(i) if the demutualisation method is the method specified in section 121AF or 121AG of the Income Tax Assessment Act 1936 --the demutualising company; or

(ii) if the demutualisation method is the method specified in section 121AH, 121AI, 121AJ, 121AK or 121AL of the Income Tax Assessment Act 1936 --the company issuing the ordinary shares referred to in that section.

(2) If the sum of:

(a) the transferred amount; and

(b) all amounts that were previously transferred to the issuing company's * share capital account, from another account of the company, in connection with the demutualisation; and

(c) all amounts that were previously transferred to the issuing company's retained profit account in connection with the demutualisation;

exceeds the listing day company valuation amount (see subsection (3)), subsection (1) does not stop this Division from applying to so much of the transferred amount as equals the lesser of the transferred amount and the amount of the excess.

Note: If there are several transfers of amounts to the issuing company's share capital account, this section must be applied separately in relation to each transferred amount, in the order in which the transfers are made.

(3) The listing day company valuation amount has the same meaning as it has for the purposes of table 1 in section 121AS of the Income Tax Assessment Act 1936 , as that table applies in relation to the demutualising company (see note 3 to that table).

197 - 40 Exclusion for post - demutualisation transfers relating to life insurance companies

(1) Subject to subsection (2), this Division does not apply to the transferred amount if:

(a) a * life insurance company (the demutualised company ) has demutualised; and

(b) the demutualisation was implemented in accordance with a demutualisation method specified in Division 9AA of Part III of the Income Tax Assessment Act 1936 ; and

(c) the amount is transferred after the end of the listing period in relation to the demutualisation (see subsection 121AE(6) of that Act); and

(d) the company transferring the amount to its * share capital account is either:

(i) the demutualised company (whichever demutualisation method was used); or

(ii) if the demutualisation method was the method specified in section 121AH, 121AI, 121AJ, 121AK or 121AL of the Income Tax Assessment Act 1936 --the company (the issuing company ) that issued the ordinary shares referred to in that section; and

(e) if subparagraph (d)(i) applies--the following conditions are satisfied in relation to the transferred amount:

(i) the amount is transferred from an account of the demutualised company consisting of shareholders' capital (within the meaning of the Life Insurance Act 1995 ) in relation to a statutory fund (within the meaning of that Act);

(ii) the amount was part of such an account at the time of the demutualisation; and

(f) if subparagraph (d)(ii) applies--the amount is transferred from a capital reserve created at the time of or in connection with the demutualisation.

(2) If the sum of:

(a) the transferred amount; and

(b) all amounts that were previously transferred to the demutualised company's * share capital account, from another account of the demutualised company, as described in subsection (1); and

(c) if the demutualisation method was the method specified in section 121AH, 121AI, 121AJ, 121AK or 121AL of the Income Tax Assessment Act 1936 --all amounts that were previously transferred to the issuing company's share capital account, from another account of the issuing company, as described in subsection (1); and

(d) all amounts that were previously transferred, in connection with the demutualisation, to the share capital account of the issuing company (within the meaning of section 197 - 35) as described in subsection 197 - 35(1), or to its retained profit account as described in paragraph 197 - 35(2)(c);

exceeds the listing day company valuation amount (see subsection (3)), subsection (1) does not stop this Division from applying to so much of the transferred amount as equals the lesser of the transferred amount and the amount of the excess.

Note: If there are several transfers of amounts to the share capital account of the demutualised company or the issuing company, this section must be applied separately in relation to each transferred amount, in the order in which the transfers are made.

(3) The listing day company valuation amount has the same meaning as it has for the purposes of table 1 in section 121AS of the Income Tax Assessment Act 1936 , as that table applies in relation to the demutualised company (see note 3 to that table).

Subdivision 197 - B -- Consequence of transfer: franking debit arises

Table of sections

197 - 45 A franking debit arises in relation to the transfer

197 - 45 A franking debit arises in relation to the transfer

(1) A * franking debit arises in a company's * franking account if an amount (the transferred amount ) to which this Division applies is transferred to the company's * share capital account. The debit arises immediately before the end of the * franking period in which the transfer of the amount occurs.

(2) The amount of the * franking debit is calculated in accordance with the formula:

where:

"applicable franking percentage" means:

(a) if, before the debit arises, the * benchmark franking percentage for the * franking period in which the transfer of the amount occurs has already been set by section 203 - 30--that percentage; or

(b) otherwise--100%.

Subdivision 197 - C -- Consequence of transfer: tainting of share capital account

Table of sections

197 - 50 The share capital account becomes tainted (if it is not already tainted)

197 - 55 Choosing to untaint a tainted share capital account

197 - 60 Choosing to untaint--liability to untainting tax

197 - 65 Choosing to untaint--further franking debits may arise

197 - 70 Due date for payment of untainting tax

197 - 75 General interest charge for late payment of untainting tax

197 - 80 Notice of liability to pay untainting tax

197 - 85 Evidentiary effect of notice of liability to pay untainting tax

197 - 50 The share capital account becomes tainted (if it is not already tainted)

(1) A company's * share capital account becomes tainted when an amount to which this Division applies is transferred to the account, if, at the time of the transfer, the account is not already tainted (because of the application of this section in relation to a previous transfer).

Note: If a company's share capital account is tainted, then a distribution from the account is taxed as a dividend in the hands of the shareholder. This is because a tainted share capital account does not count as a share capital account for the purposes of paragraph (d) of the definition of dividend in subsection 6(1) of the Income Tax Assessment Act 1936 (see subsection 6D(3) of that Act). However, although the distribution is taxed as a dividend, the company cannot pass on to the shareholder the benefit of the tax it has paid, because a distribution from a share capital account (whether or not tainted) is not frankable (see subsections 46M(1), (3) and (4) of that Act).

(2) The * share capital account remains tainted until the company chooses to untaint the account (see section 197 - 55).

Note: If, after a choice to untaint is made, the company's share capital account becomes tainted again, the account remains tainted until a fresh choice to untaint is made.

(3) The tainting amount , for a company's * share capital account that is * tainted at a particular time, means the sum of:

(a) the amount transferred to the company's share capital account that most recently caused the account to become tainted; and

(b) any other amounts to which this Division applies that have been transferred to the company's share capital account since the transfer referred to in paragraph (a) and before the particular time.

197 - 55 Choosing to untaint a tainted share capital account

(1) A company with a * share capital account that is * tainted may make a choice in the * approved form given to the Commissioner to untaint the account.

(2) The choice can be made at any time, but cannot be revoked.

Note: The choice has no effect in relation to a subsequent tainting of the share capital account that occurs after the choice is made.

197 - 60 Choosing to untaint--liability to untainting tax

Definitions

(1) For the purpose of this section:

(a) a company whose * share capital account is * tainted is a company with only lower tax members in relation to the tainting period if, throughout the tainting period, all * members of the company were covered by one, or a combination of 2 or more, of the following subparagraphs:

(i) other companies;

(ii) * complying superannuation entities;

(iii) foreign residents; and

(b) a company whose share capital account is tainted is a company with higher tax members in relation to the tainting period if it is not a company with only lower tax members in relation to the tainting period.

For this purpose, the tainting period is the period beginning when the share capital account most recently became tainted and ending when the company chooses to untaint the account.

Liability to untainting tax

(2) A company that chooses to untaint its * share capital account is liable to pay tax, known as untainting tax , equal to the amount calculated in accordance with the formula:

where:

"applicable tax amount" has the meaning given by subsection (3).

"section 197-45 franking debits" means the total * franking debits arising under section 197 - 45 because of the transfer of the amounts that made up the * tainting amount at the time of the choice.

"section 197-65 franking debits" means the total (if any) * franking debits arising under section 197 - 65 because of the choice to untaint.

Note: The payment of untainting tax does not give rise to a franking credit.

(3) In subsection (2), the applicable tax amount is the amount calculated in accordance with the formula:

where:

"applicable tax rate" means:

(a) for a company with only lower tax members in relation to the tainting period--the * corporate tax rate; or

(b) for a company with higher tax members in relation to the tainting period--the sum of:

(i) the maximum rate specified in column 2 of the table in Part I of Schedule 7 to the Income Tax Rates Act 1986 that applies for the income year in which the choice is made; and

(ii) 2.5%.

Note: The 2.5% referred to in subparagraph (b)(ii) relates to rates of Medicare levy and surcharge.

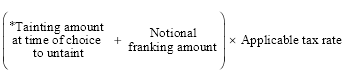

"notional franking amount" has the meaning given by subsection (4).

(4) In subsection (3), the notional franking amount is the amount calculated in accordance with the formula:

197 - 65 Choosing to untaint--further franking debits may arise

When this section applies

(1) This section applies if:

(a) a company chooses to untaint its * share capital account; and

(b) the applicable franking percentage (within the meaning of subsection (3)) is higher than the percentage that was the * benchmark franking percentage in relation to the * franking period in which the transfer of an amount (the transferred amount ) that is, or is part of, the * tainting amount occurred.

Note: If paragraph (b) is satisfied in relation to 2 or more amounts, this section is to be applied separately in relation to each of those amounts (so a separate franking debit will arise in relation to each of those amounts).

Franking debit arises in relation to making the choice

(2) A * franking debit arises in the company's * franking account in relation to the transferred amount. The debit arises immediately before the end of the * franking period in which the choice to untaint is made.

(3) The amount of the * franking debit is the amount by which the amount calculated in accordance with the following formula exceeds the amount of the franking debit that arose under section 197 - 45 in relation to the transferred amount:

where:

"applicable franking percentage" means:

(a) if, before the debit arises, the * benchmark franking percentage for the * franking period in which the choice to untaint is made has already been set by section 203 - 30--that percentage; or

(b) otherwise--100%.

197 - 70 Due date for payment of untainting tax

* Untainting tax is due and payable at the end of 21 days after the end of the * franking period in which the choice to untaint was made.

Note: For provisions about collection and recovery of untainting tax, see Part 4 - 15 in Schedule 1 to the Taxation Administration Act 1953 .

197 - 75 General interest charge for late payment of untainting tax

If any of the * untainting tax that a company is liable to pay remains unpaid 60 days after the day by which it is due to be paid, the company is liable to pay the * general interest charge on the unpaid amount for each day in the period that:

(a) started at the beginning of the 60th day after the day by which the untainting tax was due to be paid; and

(b) ends at the end of the last day on which, at the end of the day, any of the following remains unpaid:

(i) the untainting tax;

(ii) general interest charge on any of the untainting tax.

197 - 80 Notice of liability to pay untainting tax

(1) The Commissioner may give a company, by post or otherwise, a notice specifying:

(a) the amount of any * untainting tax that the Commissioner has ascertained is payable by the company; and

(b) the day on which that tax became or will become due and payable.

Effect of notice on liability etc.

(2) Subject to section 197 - 85, the amount of the liability of a company to * untainting tax, and the due date for payment of the tax, are not dependent on, or in any way affected by, the giving of a notice.

Amendment of notice

(3) The Commissioner may at any time amend a notice. An amended notice is a notice for the purposes of this section.

Inconsistency between notices

(4) If there is an inconsistency between notices that relate to the same subject matter, the later notice prevails to the extent of the inconsistency.

Objections

(5) A company that is dissatisfied with a notice made in relation to the company may object against the notice in the manner set out in Part IVC of the Taxation Administration Act 1953 .

197 - 85 Evidentiary effect of notice of liability to pay untainting tax

(1) The production of:

(a) a notice given under section 197 - 80; or

(b) a document that is signed by the Commissioner and appears to be a copy of such a notice;

is conclusive evidence that:

(c) the notice was duly given; and

(d) the amount of * untainting tax specified in the notice became due and payable by the company to which it was given on the day specified in the notice.

(2) Subsection (1) does not apply in proceedings under Part IVC of the Taxation Administration Act 1953 on a review or appeal relating to the review.

Division 2--Application and transitional provisions

Income Tax (Transitional Provisions) Act 1997

2 At the end of Part 3 - 5

Add:

Division 197 -- Tainted share capital accounts

Table of Subdivisions

197 - A Definitions

197 - B General application provision

197 - C Special provisions about companies whose share capital accounts were tainted when old Division 7B was closed off

Subdivision 197 - A -- Definitions

Table of sections

197 - 1 Definitions

In this Part:

"introduction day" means the day on which the Bill for the Act that added this Division was introduced into the Parliament.

"new Division 197" means Division 197 of the Income Tax Assessment Act 1997 .

"old Division 7B" means Division 7B of Part IIIAA of the Income Tax Assessment Act 1936 .

"old Division 7B close" -off day means 1 July 2002.

Subdivision 197 - B -- General application provision

Table of sections

197 - 5 Application of new Division 197

197 - 5 Application of new Division 197

Subject to Subdivision 197 - C of this Division, new Division 197 applies to transfers made into a company's share capital account after the introduction day.

Table of sections

197 - 10 Subdivision applies to companies whose share capital accounts were tainted when old Division 7B was closed off

197 - 15 Account taken to have ceased to be tainted when old Division 7B was closed off

197 - 20 After introduction day, account taken to have become tainted under new Division 197 to extent of previous tainting

197 - 25 Special provisions if company chooses to untaint after introduction day

This Subdivision applies to a company if, immediately before the old Division 7B close - off day, the company's share capital account was tainted under old Division 7B.

197 - 15 Account taken to have ceased to be tainted when old Division 7B was closed off

(1) The company's share capital account is taken to have ceased to be tainted under old Division 7B at the start of the Division 7B close - off day.

(2) No liability to untainting tax, and no franking debit, arises under old Division 7B in relation to the share capital account being taken to have ceased to be tainted.

(1) Immediately after the introduction day, the company's share capital account is taken to become tainted under new Division 197 as if:

(a) the company had, at that time, transferred an amount (the notionally transferred amount ) to its share capital account from another of its accounts that equalled the tainting amount (the old Division 7B tainting amount ), within the meaning of old Division 7B, in relation to the share capital account immediately before the old Division 7B close - off day; and

(b) none of the exclusions in sections 197 - 10 to 197 - 40 of new Division 197 applied, to any extent, in relation to the notionally transferred amount.

(2) No franking debit arises under Subdivision 197 - B of new Division 197 in relation to the notionally transferred amount.

197 - 25 Special provisions if company chooses to untaint after introduction day

(1) This section applies if, after the introduction day, the company chooses under section 197 - 55 of new Division 197 to untaint its share capital account.

Working out the amount of section 197 - 60 untainting tax

(2) For the purpose of section 197 - 60 of new Division 197, the tainting amount at the time of the choice to untaint is taken to consist of:

(a) the amounts (the old Division 7B tainting amount components ) that made up the old Division 7B tainting amount; and

(b) any amounts to which new Division 197 applies that have been transferred to the company's share capital account since the introduction day and before the choice to untaint is made.

Note 1: The company will not be liable to untainting tax if it is covered by subsection (5).

Note 2: If the company is covered by subsection (6), the old Division 7B tainting amount components will not be included in the tainting amount for the purpose of section 197 - 60.

(3) For the purpose of section 197 - 60 of new Division 197, a reference to the section 197 - 45 franking debit that arose in relation to an old Division 7B tainting amount component is taken to be a reference to the tax - paid - basis franking debit amount in relation to that component (see subsection (4)).

(4) For the purpose of subsection (3), the tax - paid - basis franking debit amount , in relation to an old Division 7B tainting amount component, is the amount worked out in accordance with the formula:

where:

"class A franking debit" means the class A franking debit (if any) that arose under section 160ARDV of old Division 7B in relation to the old Division 7B tainting amount component.

"class C franking debit" means the class C franking debit that arose under section 160ARDQ or 160ARDV of old Division 7B in relation to the old Division 7B tainting amount component.

(5) The company is not liable to untainting tax under section 197 - 60 of new Division 197 in relation to the choice to untaint if:

(a) during the period from the time when the company's share capital account became tainted under old Division 7B to the time when the choice to untaint is made, the company was a company with only lower tax shareholders (as defined in subsection 197 - 60(1) of new Division 197); and

(b) the tainting amount for the purpose of section 197 - 60 of new Division 197 does not include any amounts of the kind mentioned in paragraph (2)(b) of this section.

(6) If:

(a) the tainting amount for the purpose of section 197 - 60 of new Division 197 consists of or includes an amount or amounts of the kind mentioned in paragraph (2)(b) of this section; and

(b) during the period from the time when the company's share capital account became tainted to the time when the amount, or the first of the amounts, referred to in paragraph (a) of this subsection was transferred into the company's share capital account, the company was a company with only lower tax shareholders (as defined in subsection 197 - 60(1) of new Division 197);

then, despite subsection (2) of this section, for the purpose of section 197 - 60 of new Division 197, the tainting amount at the time of the choice to untaint does not include the old Division 7B tainting amount components.

Working out the amount of section 197 - 65 franking debit

(7) For the purpose of section 197 - 65 of new Division 197, the tainting amount at the time of the choice to untaint is taken to consist of:

(a) the amounts (the old Division 7B tainting amount components ) that made up the old Division 7B tainting amount; and

(b) any amounts to which new Division 197 applies that have been transferred to the company's share capital account since the introduction day and before the choice to untaint is made.

Note: In relation to amounts described in paragraph (b), section 197 - 65 applies without any notional modifications.

(8) Paragraph 197 - 65(1)(b) of new Division 197 has effect in relation to each old Division 7B tainting amount component as if the following paragraph (the notionally substituted paragraph ) were substituted for it:

(b) the tax - paid - basis franking debit amount in relation to the old Division 7B tainting amount component is less than the amount calculated by the formula in subsection 197 - 65(3) in relation to the component.

(9) Subsection 197 - 65(3) of new Division 197 has effect in relation to each old Division 7B tainting amount component as if the reference to the amount of the franking debit that arose under section 197 - 45 in relation to the transferred amount were instead a reference to the tax - paid - basis franking debit amount in relation to the old Division 7B tainting amount component.

(10) For the purpose of the notionally substituted paragraph, and of subsection (9) of this section, the tax - paid - basis franking debit amount , in relation to an old Division 7B tainting amount component, is the amount worked out in accordance with the formula:

where:

"class A franking debit" means the class A franking debit (if any) that arose under section 160ARDV of old Division 7B in relation to the old Division 7B tainting amount component.

"class C franking debit" means the class C franking debit that arose under section 160ARDQ or 160ARDV of old Division 7B in relation to the old Division 7B tainting amount component.

Part 2 -- Consequential amendments relating to rewritten share capital tainting rules

Income Tax Assessment Act 1936

3 Subsection 6(1)

Insert:

"tainted" , in relation to a company's share capital account, has the same meaning as in the Income Tax Assessment Act 1997 .

4 Subsection 6(1) (definition of tainting amount )

Repeal the definition, substitute:

"tainting amount" has the same meaning as in the Income Tax Assessment Act 1997 .

Income Tax Assessment Act 1997

5 Section 205 - 30 (after table item 7)

Insert:

7A | a * franking debit arises under subsection 197 - 45(1) because an amount to which Division 197 applies is transferred to a company's * share capital account | the amount of the debit specified in subsection 197 - 45(2) | at the time provided by subsection 197 - 45(1) |

7B | a * franking debit arises under subsection 197 - 65(2) because a company chooses to untaint its * share capital account | the amount of the debit specified in subsection 197 - 65(3) | at the time provided by subsection 197 - 65(2) |

6 Subsection 721 - 10(2) (table item 5)

Repeal the item, substitute:

5

| section 197 - 70 (untainting tax) | the * franking period of the * head company in which the * untainting tax became due and payable |

7 Subsection 995 - 1(1)

Insert:

"tainted" : for when a company's * share capital account is tainted , see subsections 197 - 50(1) and (2).

8 Subsection 995 - 1(1)

Insert:

"tainting amount" has the meaning given by subsection 197 - 50(3).

9 Subsection 995 - 1(1)

Insert:

"untainting tax" has the meaning given by subsection 197 - 60(2).

Taxation Administration Act 1953

10 Subsection 8AAB(4) (table item 1A)

Repeal the item.

11 Subsection 8AAB(5) (after table item 2)

Insert:

2AA | 197 - 75 |

12 Subsection 250 - 10(1) in Schedule 1 (table item 25)

Repeal the item.

13 Subsection 250 - 10(2) in Schedule 1 (before table item 38)

Insert:

37A | untainting tax | 197 - 70 |

Division 2--Application provision

14 Application of amendments

The amendments made by Division 1 apply in relation to transfers made into a company's share capital account after the day on which the Bill for this Act was introduced into the Parliament.

Part 3 -- Amendment of the old share capital tainting rules

Income Tax Assessment Act 1936

15 Paragraph 160ARDM(2)(b)

Repeal the paragraph.

16 After subsection 160ARDM(2A)

Insert:

(2B) If the transfer of an amount as mentioned in subsection (1) is a transfer under a debt/equity swap (as defined in subsection (5)), the following provisions have effect:

(a) if the transferred amount does not exceed the lesser of:

(i) the market value of the shares referred to in subsection (5); and

(ii) so much of the debt referred to in subsection (5) as is discharged, released or extinguished in return for the shares;

subsection (1) does not apply to the transferred amount;

(b) if the transferred amount exceeds the lesser of the amounts referred to in paragraph (a), subsection (1) applies only to the excess.

(2C) Subsection (1) does not apply to an amount transferred as mentioned in that subsection if:

(a) it is transferred from an option premium reserve of the company; and

(b) the transfer is because of the exercise of options to acquire shares in the company; and

(c) premiums in respect of those options were credited to the option premium reserve.

17 After subsection 160ARDM(4)

Insert:

(4A) If:

(a) an amount is transferred as mentioned in subsection (1); and

(b) the amount is transferred in connection with the demutualisation of a company; and

(c) the demutualisation is implemented in accordance with a demutualisation method specified in Division 9AA of Part III; and

(d) the transfer occurs within the listing period in relation to the demutualisation (see subsection 121AE(6)); and

(e) the company (the issuing company ) to whose share capital account the amount is transferred is:

(i) if the demutualisation method is the method specified in section 121AF or 121AG--the demutualising company; or

(ii) if the demutualisation method is the method specified in section 121AH, 121AI, 121AJ, 121AK or 121AL--the company issuing the ordinary shares referred to in that section;

the following provisions have effect:

(f) if the sum of:

(i) the transferred amount; and

(ii) all amounts that were previously transferred to the issuing company's share capital account, from another account of the company, in connection with the demutualisation; and

(iii) all amounts that were previously transferred to the issuing company's retained profit account in connection with the demutualisation;

does not exceed the listing day company valuation amount (as defined in subsection (6)), subsection (1) does not apply to the transferred amount;

(g) if the sum of the amounts referred to in paragraph (f) exceeds the listing day company valuation amount (as defined in subsection (6)), subsection (1) applies only to the excess.

Note: If there are several transfers of amounts to the issuing company's share capital account, this section must be applied separately in relation to each transferred amount, in the order in which the transfers are made.

(4B) If:

(a) a life assurance company (the demutualised company ) has demutualised; and

(b) the demutualisation was implemented in accordance with a demutualisation method specified in Division 9AA of Part III; and

(c) an amount is transferred as mentioned in subsection (1); and

(d) the amount is transferred after the end of the listing period in relation to the demutualisation (see subsection 121AE(6)); and

(e) the company transferring the amount to its share capital account is either:

(i) the demutualised company (whichever demutualisation method was used); or

(ii) if the demutualisation method was the method specified in section 121AH, 121AI, 121AJ, 121AK or 121AL--the company (the issuing company ) that issued the ordinary shares referred to in that section; and

(f) if subparagraph (e)(i) applies--the following conditions are satisfied in relation to the transferred amount:

(i) the amount is transferred from an account of the demutualised company consisting of shareholders' capital (within the meaning of the Life Insurance Act 1995 ) in relation to a statutory fund (within the meaning of that Act);

(ii) the amount was part of such an account at the time of the demutualisation; and

(g) if subparagraph (e)(ii) applies--the amount is transferred from a capital reserve created at the time of or in connection with the demutualisation;

the following provisions have effect:

(h) if the sum of:

(i) the transferred amount; and

(ii) all amounts that were previously transferred to the demutualised company's share capital account, from another account of the demutualised company, as described in paragraphs (c) to (g); and

(iii) if the demutualisation method was the method specified in section 121AH, 121AI, 121AJ, 121AK or 121AL--all amounts that were previously transferred to the issuing company's share capital account, from another account of the issuing company, as described in paragraphs (c) to (g); and

(iv) all amounts that were previously transferred, in connection with the demutualisation, to the share capital account of the issuing company (within the meaning of subsection (4A)) as described in paragraphs (4A)(b) to (e), or to its retained profit account as described in subparagraph (4A)(f)(iii);

does not exceed the listing day company valuation amount (as defined in subsection (6)), subsection (1) does not apply to the transferred amount;

(i) if the sum of the amounts referred to in paragraph (h) exceeds the listing day company valuation amount (as defined in subsection (6)), subsection (1) applies only to the excess.

Note: If there are several transfers of amounts to the share capital account of the demutualised company or the issuing company, this subsection must be applied separately in relation to each transferred amount, in the order in which the transfers are made.

18 Subsection 160ARDM(6)

Insert:

"listing day company valuation amount" has the same meaning as it has for the purposes of table 1 in section 121AS, as that table applies in relation to the demutualising company referred to in subsection (4A), or the demutualised company referred to in subsection (4B), as the case requires (see note 3 to that table).

Division 2--Application provision

19 Application of amendments

The amendments made by Division 1 apply in relation to transfers of amounts made during the period starting on 1 July 1998 and ending immediately before 1 July 2002.

Part 4 -- Relocating the definition of share capital account

Income Tax Assessment Act 1997

20 After Subdivision 975 - A

Insert:

Subdivision 975 - G -- What is a company's share capital account?

Table of sections

975 - 300 Meaning of share capital account

975 - 300 Meaning of share capital account

(1) A company's share capital account is:

(a) an account that the company keeps of its share capital; or

(b) any other account (whether or not called a share capital account) that satisfies the following conditions:

(i) the account was created on or after 1 July 1998;

(ii) the first amount credited to the account was an amount of share capital.

(2) If a company has more than one account covered by subsection (1), the accounts are taken, for the purposes of this Act, to be a single account.

Note: Because the accounts are taken to be a single account (the combined share capital account ), tainting of any of the accounts has the effect of tainting the combined share capital account.

(3) However, if a company's * share capital account is * tainted, that account is taken not to be a share capital account for the purposes this Act, other than:

(a) subsection 118 - 20(6); and

(b) Division 197; and

(c) the definition of paid - up share capital in subsection 6(1) of the Income Tax Assessment Act 1936 ; and

(d) subsection 44(1B) of the Income Tax Assessment Act 1936 ; and

(e) section 46H of the Income Tax Assessment Act 1936 ; and

(f) subsection 159GZZZQ(5) of the Income Tax Assessment Act 1936 .

Division 2--Consequential amendments

Income Tax Assessment Act 1936

21 Subsection 6(1) (definition of share capital account )

Repeal the definition, substitute:

"share capital account" has the same meaning as in the Income Tax Assessment Act 1997 .

22 Section 6D

Repeal the section.

Income Tax Assessment Act 1997

23 Paragraph 118 - 20(6)(a)

Omit "share capital account", substitute " * share capital account".

24 Subsection 164 - 15(1) (definition of share capital account credit )

Omit "share capital account", substitute " * share capital account".

25 Subsection 164 - 15(2) (definition of share capital account credit )

Omit "share capital account", substitute " * share capital account".

26 Subsection 164 - 15(4) (definition of share capital account credit )

Omit "share capital account", substitute " * share capital account".

27 Paragraph 974 - 120(2)(b)

Omit "share capital account", substitute " * share capital account".

28 Subsection 995 - 1(1) (definition of paid - up share capital )

Omit "share capital account", substitute " * share capital account".

29 Subsection 995 - 1(1)

Insert:

"share capital account" has the meaning given by section 975 - 300.

Division 3--Application provision

30 Application of amendments

The amendments made by Divisions 1 and 2 apply for the purpose of determining whether an account is a share capital account when applying a provision of the Income Tax Assessment Act 1997 or the Income Tax Assessment Act 1936 in relation to a time that is after the commencement of the amendments, even if the account was in existence before that commencement.