Commonwealth Consolidated Acts Commonwealth Consolidated Acts

Commonwealth Consolidated Acts Commonwealth Consolidated ActsIncome Tax Assessment Act 1997

1 Division 328 (heading)

Repeal the heading, substitute:

Division 328 -- Small business entities

2 Subdivision 328 - A

Repeal the Subdivision, substitute:

328 - 5 What this Division is about

This Division explains the meaning of the terms small business entity , annual turnover , aggregated turnover and related concepts (Subdivision 328 - C).

If you are a small business entity, this Division allows you to change the way the income tax law applies to you in these ways:

(a) you can choose to put your depreciating assets into a long life pool or a general pool and treat each pool as a single asset (Subdivision 328 - D);

(b) you can choose not to account for annual changes in trading stock value that are not more than $5,000 (Subdivision 328 - E).

In usual circumstances, these changes will simplify the working out of your taxable income, and so reduce your compliance costs.

Table of sections

328 - 10 Concessions available to small business entities

328 - 10 Concessions available to small business entities

(1) If you are a small business entity for an income year, you can choose to take advantage of the concessions set out in the following table. Some of the concessions have additional, specific conditions that must also be satisfied.

Item | Concession | Provision |

1 | CGT 15 - year asset exemption | Subdivision 152 - B of this Act |

2 | CGT 50% active asset reduction | Subdivision 152 - C of this Act |

3 | CGT retirement exemption | Subdivision 152 - D of this Act |

4 | CGT roll - over | Subdivision 152 - E of this Act |

5 | Simpler depreciation rules | Subdivision 328 - D of this Act |

6 | Simplified trading stock rules | Subdivision 328 - E of this Act |

7 | Deducting certain prepaid business expenses immediately | Sections 82KZM and 82KZMD of the Income Tax Assessment Act 1936 |

8 | Accounting for GST on a cash basis | Section 29 - 40 of the GST Act |

9 | Annual apportionment of input tax credits for acquisitions and importations that are partly creditable | Section 131 - 5 of the GST Act |

10 | Paying GST by quarterly instalments | Section 162 - 5 of the GST Act |

11 | FBT car parking exemption | Section 58GA of the Fringe Benefits Tax Assessment Act 1986 |

12 | PAYG instalments based on GDP - adjusted notional tax | Section 45 - 130 of Schedule 1 to the Taxation Administration Act 1953 |

(2) Also, if you are a small business entity for an income year, the standard 2 - year period for amending your assessment applies to you (section 170 of the Income Tax Assessment Act 1936 ).

Note: If you are a small business entity for an income year and your aggregated turnover for the year is less than $75,000, you may also be entitled to the 25% entrepreneurs' tax offset: see Subdivision 61 - J of this Act.

3 Subdivision 328 - D (heading)

Repeal the heading, substitute:

Subdivision 328 - D -- Capital allowances for small business entities

4 Section 328 - 170

Omit "STS taxpayers deduct amounts for most of their depreciating assets", substitute "If you are a small business entity, you can choose to deduct amounts for most of your depreciating assets".

5 Section 328 - 170 (paragraph (b))

Repeal the paragraph, substitute:

(b) not choosing to use this Subdivision for an income year after having chosen to do so for an earlier income year; and

6 Subsection 328 - 175(1)

Repeal the subsection, substitute:

(1) You can choose to calculate your deductions and some amounts of assessable income under this Subdivision instead of under Division 40 for an income year for all the * depreciating assets that you * hold if:

(a) you are a * small business entity for the income year; and

(b) you started to use the assets or have them * installed ready for use, for a * taxable purpose during or before that income year.

This subsection has effect subject to subsections (2) to (10).

Note: If you choose to use this Subdivision for an income year, you continue to use this Subdivision for your small business pools for a later income year even if you are not a small business entity, or do not choose to use this Subdivision, for the later year: see section 328 - 220.

7 Subsection 328 - 175(3)

Omit "an * STS taxpayer", substitute "a * small business entity".

8 Subsection 328 - 175(3) (note)

Omit "40 - 340(3)", substitute "40 - 340(1) or (3)".

9 Subsection 328 - 175(4)

Omit "that choice for each * depreciating asset of that kind", substitute "the choice under subsection (3) for each * depreciating asset of the kind referred to in that subsection".

10 Paragraph 328 - 175(4)(a)

Omit "became, an * STS taxpayer", substitute "were, a * small business entity".

11 Paragraph 328 - 175(7)(a)

Omit "before you became an * STS taxpayer", substitute "during an income year for which you were not a * small business entity or had not chosen to use this Subdivision".

12 At the end of section 328 - 175

Add:

Exception: restriction on choosing to use this Subdivision

(10) If:

(a) you choose to use this Subdivision to deduct amounts for your * depreciating assets for an income year; and

(b) you do not choose to use this Subdivision for a later income year for which you satisfy the conditions to make this choice (see subsection (1));

you cannot choose to use this Subdivision until at least 5 years after the first later income year for which you satisfied the conditions to make this choice but did not do so.

Note 1: Your ability to choose to use this Subdivision may also be restricted by section 328 - 440 of the Income Tax (Transitional Provisions) Act 1997 .

Note 2: If you choose to use this Subdivision for an income year, you continue to use it for assets that have been allocated to your small business pools for a later income year even if you are not a small business entity, or do not choose to use this Subdivision, for the later year: see section 328 - 220.

13 Paragraph 328 - 180(1)(a)

Omit "an * STS taxpayer", substitute "a * small business entity".

14 After paragraph 328 - 180(1)(a)

Insert:

(ab) you chose to use this Subdivision for each of those years; and

15 Subsection 328 - 180(2)

Omit "for an income year for which you are an * STS taxpayer", substitute ", for an income year for which you are a * small business entity and you choose to use this Subdivision,".

16 Subsection 328 - 180(3)

Omit "STS pool", substitute "small business pool".

17 Subsection 328 - 180(5)

Omit "when you are not an * STS taxpayer", substitute "during an income year for which you are not a * small business entity or do not choose to use this Subdivision".

18 Subsection 328 - 185(1)

Omit "As an * STS taxpayer", substitute "If you are a * small business entity for an income year and you have chosen to use this Subdivision for that year".

19 Paragraph 328 - 185(2)(a)

Omit " general STS pool ", substitute " general small business pool ".

20 Paragraph 328 - 185(2)(b)

Omit " long life STS pool ", substitute " long life small business pool ".

21 Paragraph 328 - 185(3)(a)

Omit "became, an * STS taxpayer", substitute "were, a * small business entity".

22 Subsection 328 - 185(3)

Omit "STS pool" (wherever occurring), substitute "small business pool".

23 Subsection 328 - 185(4)

Omit "while you are an * STS taxpayer", substitute "for which you are a * small business entity and you choose to use this Subdivision".

24 Subsection 328 - 185(5)

Omit "STS", substitute "small business".

25 Subsection 328 - 185(6)

Omit "an * STS taxpayer", substitute "a * small business entity and you choose to use this Subdivision".

26 Subsection 328 - 185(7)

Omit "STS pool" (wherever occurring), substitute "small business pool".

27 Subsection 328 - 185(7)

Omit "even if you stop being an * STS taxpayer and again become one", substitute "even if you are not a * small business entity for a later income year or you do not choose to use this Subdivision for that later year".

28 Subsection 328 - 185(7) (note)

Repeal the note, substitute:

Note: If you chose to use this Subdivision for an income year, you continue to use it for your small business pools for a later income year even if you are not a small business entity, or do not choose to use this Subdivision, for the later year: see section 328 - 220.

29 Subsection 328 - 185(7) (example)

Repeal the example, substitute:

Example: Greg is not a small business entity for the 2008 - 09 income year. At that time his long life small business pool contains one depreciating asset with an effective life of 26 years. Greg still holds that asset in the 2010 - 11 income year. Greg is a small business entity for that income year and chooses to use this Subdivision. The asset has remained in the pool since the end of the 2008 - 09 income year. The asset is not re - allocated when he recommences deducting amounts for depreciating assets under this Subdivision, even though its remaining effective life is now 24 years.

30 Subsection 328 - 190(1)

Omit "STS" (wherever occurring), substitute "small business".

31 Subsection 328 - 190(2)

Omit "while you are an * STS taxpayer", substitute "for which you are a * small business entity and choose to use this Subdivision".

32 Subsection 328 - 190(3)

Omit "an * STS taxpayer", substitute "a * small business entity and choose to use this Subdivision".

33 Subsection 328 - 190(4) (note)

Omit all the words after "relief", substitute "under section 40 - 340 is chosen: see sections 328 - 243 and 328 - 247.".

34 Subsection 328 - 195(1)

Omit "you are an * STS taxpayer", substitute "you are a * small business entity and choose to use this Subdivision".

35 Subsection 328 - 195(2) (note)

Repeal the note, substitute:

Note: You continue to deduct amounts using your small business pools even if you are not a small business entity, or do not choose to use this Subdivision, for a later income year: see section 328 - 220.

36 Subsection 328 - 195(3)

Repeal the subsection, substitute:

(3) However, if:

(a) you are not a * small business entity for an income year or you do not choose to use this Subdivision for that year; but

(b) you are a small business entity for a later income year and you choose to use this Subdivision for the later year;

the opening pool balance of a pool includes the sum of the * taxable purpose proportions of the * adjustable values of * depreciating assets allocated to the pool under subsection 328 - 185(3) for that year.

37 Section 328 - 200 (note)

Omit all the words after "relief", substitute "under section 40 - 340 is chosen: see sections 328 - 243 and 328 - 245.".

38 Subsection 328 - 205(1)

Omit "became, an * STS taxpayer", substitute "were, a * small business entity".

39 Paragraph 328 - 205(1)(a)

Omit "STS pool" (wherever occurring), substitute "small business pool".

40 Paragraph 328 - 205(1)(c)

Before "calculate", insert "have chosen to".

41 Subsection 328 - 205(1) (note 3)

Omit all the words after "relief", substitute "under section 40 - 340 is chosen: see sections 328 - 243 and 328 - 257.".

42 Subsection 328 - 205(2)

Omit "while you are an * STS taxpayer", substitute "during an income year for which you are a * small business entity and you choose to use this Subdivision".

43 Paragraph 328 - 205(4)(b)

Omit "STS pool", substitute "small business pool".

44 Paragraph 328 - 205(4)(c)

Omit "STS pool", substitute "small business pool".

45 Subsection 328 - 205(4) (example)

Repeal the example, substitute:

Example: When Bria's van was allocated to her general small business pool for the 2007 - 08 income year, she estimated that it would be used 50% for deliveries in her florist business. Due to increasing deliveries, Bria estimates the van's business use to be 70% for the 2008 - 09 year, and 90% for the 2009 - 10 year. She makes an adjustment under section 328 - 225 for both those years.

Bria sells the van for $3,000 at the start of the 2011 - 12 income year. She must now average the business use estimates for the van for the year it was allocated to the pool and the next 3 years to work out the taxable purpose proportion of its termination value. The average is worked out as follows:

The taxable purpose proportion of the van's termination value is, therefore:

46 Subsection 328 - 210(1)

Omit "STS" (wherever occurring), substitute "small business".

47 Subsection 328 - 210(3) (example)

Omit "Amanda's Graphics, an STS taxpayer, has an opening pool balance of $1,200 for its general STS pool for the 2004 - 05 income year.", substitute "Amanda's Graphics is a small business entity for the 2008 - 09 income year and chooses to use this Subdivision for that year. The business has an opening pool balance of $1,200 for its general small business pool for that year.".

48 Section 328 - 220

Repeal the section, substitute:

(1) If you are not a * small business entity for an income year or you do not choose to use this Subdivision for that year, this Subdivision continues to apply to your * general small business pool and * long life small business pool for that year and later income years.

(2) However, * depreciating assets you started to use, or have * installed ready for use, for a * taxable purpose during an income year for which you are not a * small business entity or do not choose to use this Subdivision cannot be allocated to a pool under this Subdivision until an income year for which you are a small business entity and you choose to use this Subdivision.

(3) This section applies to a transferee referred to in subsection 328 - 243(1) or (1A) who:

(a) was not a * small business entity for the income year in which the relevant * balancing adjustment events occurred; or

(b) did not choose to use this Subdivision for that year;

as if the transferee had been a small business entity for an earlier income year and had chosen to use this Subdivision for the earlier year. This rule applies even if roll - over relief is not chosen.

49 Subsection 328 - 225(1) (note)

Omit all the words after "relief", substitute "under section 40 - 340 is chosen: see sections 328 - 243 and 328 - 257.".

50 Subsection 328 - 225(2)

Omit "STS" (wherever occurring), substitute "small business".

51 Subsection 328 - 225(3) (paragraph (a) of the definition of asset value )

Omit "while you were an * STS taxpayer", substitute "during an income year for which you were a * small business entity and chose to use this Subdivision".

52 Subsection 328 - 225(3) (paragraph (b) of the definition of asset value )

Omit "while you were not an STS taxpayer ", substitute "during an income year for which you were not a * small business entity or did not choose to use this Subdivision".

53 Subsection 328 - 225(3) (paragraph (b) of the definition of asset value )

Omit "STS pool" (wherever occurring), substitute "small business pool".

54 Paragraph 328 - 225(4)(a)

Omit "while you were an * STS taxpayer", substitute "during an income year for which you were a * small business entity and chose to use this Subdivision".

55 Paragraph 328 - 225(4)(b)

Omit "while you were not an STS taxpayer ", substitute "during an income year for which you were not a * small business entity or did not choose to use this Subdivision".

56 Subsection 328 - 225(4) (note)

Omit "general STS pool" (first occurring), substitute "general small business pool".

57 Subsection 328 - 225(4) (note)

Omit "while you were not an STS taxpayer", substitute "during an income year for which you were not a small business entity or did not choose to use this Subdivision".

58 Subsection 328 - 225(4) (note)

Omit "general STS pool" (second occurring), substitute "general small business pool".

59 Subsection 328 - 225(4) (note)

Omit "while you were an STS taxpayer", substitute "during an income year for which you were a small business entity and chose to use this Subdivision".

60 Subparagraphs 328 - 225(5)(a)(i) and (ii)

Omit "STS", substitute "small business".

61 Subsection 328 - 235(1)

Omit "as an * STS taxpayer", substitute "if you are a * small business entity for an income year".

62 Subsection 328 - 235(2)

Omit "chosen to be an * STS taxpayer", substitute "been a * small business entity and chosen to use this Subdivision".

63 Paragraph 328 - 243(2)(b)

Omit "STS" (wherever occurring), substitute "small business".

64 Subsection 328 - 247(1)

Omit "STS" (wherever occurring), substitute "small business".

65 Subsection 328 - 247(1) (example)

Omit "is an STS taxpayer", substitute "is a small business entity for the relevant income year and has chosen to use this Subdivision for that year".

66 Subsection 328 - 247(1) (example)

Omit "becomes an STS taxpayer for the income year", substitute "is a small business entity for the income year and chooses to use this Subdivision for that year".

67 Subsection 328 - 247(1) (example)

Omit "STS pool", substitute "small business pool".

68 Subsection 328 - 247(2)

Omit "STS" (wherever occurring), substitute "small business".

69 Subsection 328 - 250(3) (example)

Omit "becomes an STS taxpayer for the BAE year", substitute "is a small business entity for the BAE year, and chooses to use this Subdivision for that year".

70 Paragraph 328 - 255(1)(a)

Omit "STS" (wherever occurring), substitute "small business".

71 Subdivision 328 - E (heading)

Repeal the heading, substitute:

Subdivision 328 - E -- Trading stock for small business entities

72 Section 328 - 280

Omit "STS taxpayers do not need to account", substitute "Small business entities can choose not to account".

73 Section 328 - 280

Omit "for STS taxpayers", substitute "for small business entities".

74 Section 328 - 285 (heading)

Repeal the heading, substitute:

328 - 285 Trading stock for small business entities

75 Subsection 328 - 285(1)

Omit "(1)".

76 Subsection 328 - 285(1)

Omit "You do not have to account", substitute "You can choose not to account".

77 Paragraph 328 - 285(1)(a)

Omit "an * STS taxpayer", substitute "a * small business entity".

78 At the end of subsection 328 - 285(1)

Add:

Note 3: If you choose to account for changes in the value of your trading stock for an income year, you will have to do a stocktake and account for the change in the value of all your trading stock: see Subdivision 70 - C.

79 Subsection 328 - 285(2)

Repeal the subsection.

80 Section 328 - 290

Repeal the section.

81 Subsection 328 - 295(1)

Omit "are an * STS taxpayer", substitute "make a choice under section 328 - 285".

82 Subsection 328 - 295(2)

Omit "subsection 328 - 285(1) applies to you for an income year and you have not made a choice under subsection 328 - 285(2) for that year", substitute "you make a choice under section 328 - 285 for an income year".

83 Subsection 328 - 295(2) (note)

Omit "If subsection 328 - 285(1) does not apply", substitute "If you do not make a choice under section 328 - 285".

84 Subsection 328 - 295(2) (example)

Repeal the example, substitute:

Example: Angela operates a riding school, and also sells riding gear. Her business is a small business entity for the 2008 - 09 income year and makes a choice under section 328 - 285 for that year.

At the start of the 2008 - 09 income year, the opening value of Angela's trading stock is $30,000. Using her reliable inventory system, she estimates the closing value to be $34,000.

The closing value for the 2008 - 09 income year, and the opening value for the 2009 - 10 income year, will be $30,000.

85 Subdivision 328 - F

Repeal the Subdivision.

86 Subdivision 328 - G

Repeal the Subdivision.

87 Subsection 995 - 1(1) (paragraph (ac) of the definition of capital allowance )

Omit "STS taxpayers", substitute "small business entities".

88 Subsection 995 - 1(1) (paragraph (b) of the definition of closing pool balance )

Omit "STS" (wherever occurring), substitute "small business".

89 Subsection 995 - 1(1)

Insert:

"general small business pool" has the meaning given by section 328 - 185.

90 Subsection 995 - 1(1) (definition of general STS pool )

Repeal the definition.

91 Subsection 995 - 1(1)

Insert:

"long life small business pool" has the meaning given by section 328 - 185.

92 Subsection 995 - 1(1) (definition of long life STS pool )

Repeal the definition.

93 Subsection 995 - 1(1) (definition of STS affiliate )

Repeal the definition.

94 Subsection 995 - 1(1) (definition of STS average turnover )

Repeal the definition.

95 Subsection 995 - 1(1) (definition of STS group turnover )

Repeal the definition.

96 Subsection 995 - 1(1) (definition of STS taxpayer )

Repeal the definition.

Part 2 -- Consequential amendments

Income Tax Assessment Act 1936

97 Subsection 6(1)

Insert:

"small business entity" has the meaning given by subsection 995 - 1(1) of the Income Tax Assessment Act 1997 .

98 Paragraph 73BA(4)(a)

Omit "STS taxpayers", substitute "small business entities".

Note: The heading to subsection 73BA(4) is altered by omitting " STS " and substituting " small business ".

99 Subsection 82KZL(1) (definition of STS taxpayer )

Repeal the definition.

100 Subparagraph 82KZM(1)(aa)(i)

Repeal the subparagraph, substitute:

(i) the taxpayer is a small business entity for the year of income and has not chosen to apply section 82KZMD to the expenditure;

Note: The heading to section 82KZM is altered by omitting " STS taxpayer " and substituting " small business entities ".

101 Paragraph 82KZMA(2)(b)

Repeal the paragraph, substitute:

(b) if the taxpayer is a small business entity for the expenditure year--must, before lodging its return of income for that year or within such further time as the Commissioner allows, choose to apply section 82KZMD to the expenditure.

102 At the end of section 82KZMD

Add:

Note: This section does not apply to expenditure incurred by a small business entity unless the small business entity chooses to apply this section to the expenditure: see paragraph 82KZMA(2)(b).

Note: The heading to section 82KZMD is altered by omitting " (except by an STS taxpayer) ".

103 Subsection 170(1) (table item 1, column headed "Qualification", paragraphs (a), (b) and (d))

Omit "an STS taxpayer", substitute "a small business entity".

104 Subsection 170(1) (table item 2, column headed "Time of amendment")

Omit "an STS taxpayer", substitute "a small business entity".

105 Subsection 170(1) (table item 2, column headed "Qualification", paragraphs (a) and (c))

Omit "an STS taxpayer", substitute "a small business entity".

106 Subsection 170(1) (table item 3, column headed "Time of amendment")

Omit "an STS taxpayer", substitute "a small business entity".

107 Subsection 170(1) (table item 3, column headed "Qualification", paragraphs (a) and (b))

Omit "an STS taxpayer", substitute "a small business entity".

108 Subsection 170(14) (definition of STS taxpayer )

Repeal the definition.

Income Tax Assessment Act 1997

109 Subsection 4 - 15(2) (table item 1A)

Repeal the item.

110 Section 13 - 1 (table item headed "entrepreneurs' tax offset")

Omit " simplified tax system ", substitute " small business entities ".

111 Section 13 - 1 (table item headed "partnerships")

Omit " simplified tax system ", substitute " small business entities ".

112 Section 13 - 1 (table item headed "simplified tax system")

Omit " simplified tax system ", substitute " small business entities ".

113 Section 13 - 1 (table item headed "trusts")

Omit " simplified tax system ", substitute " small business entities ".

114 Section 20 - 157 (heading)

Repeal the heading, substitute:

20 - 157 Exception for small business entities

115 Subsection 27 - 100(5) (heading)

Repeal the heading, substitute:

Small business pools

116 Subsection 40 - 25(1) (note 2)

Omit "STS taxpayers", substitute "Small business entities can choose to".

117 Subsection 40 - 340(3) (note 2)

Omit "STS taxpayers", substitute "small business entities that calculate deductions for their depreciating assets under that Subdivision".

118 Subsection 40 - 425(7) (heading)

Repeal the heading, substitute:

Exception: small business entities

119 Subsection 40 - 425(7)

Omit "STS taxpayers", substitute "small business entities".

120 Subsection 40 - 430(1) (note 2)

Repeal the note, substitute:

Note 2: If you are a small business entity for the income year and you calculate your deductions for your depreciating assets under Subdivision 328 - D, you must deduct amounts for your depreciating assets under that Subdivision unless deductions for particular assets are specifically excluded by that Subdivision.

121 Section 61 - 500

Omit "business in the simplified tax system with annual group turnover", substitute "small business entity with aggregated turnover".

122 Section 61 - 500

Omit "the annual group turnover", substitute "your aggregated turnover".

123 Section 61 - 500

Omit "individual STS taxpayer running your own business", substitute "individual running your own small business".

124 Section 61 - 500

Omit "an STS taxpayer", substitute "a small business entity".

125 Paragraph 61 - 505(1)(b)

Omit "an * STS taxpayer", substitute "a * small business entity".

126 Paragraph 61 - 505(1)(c)

Omit " * STS group turnover", substitute " * aggregated turnover".

127 Paragraph 61 - 505(1)(d)

Omit " * net STS income", substitute " * net small business income".

128 Subsection 61 - 505(2) (method statement, steps 3, 4 and 5)

Repeal the steps, substitute:

Step 3 . Work out the percentage (the small business percentage ) using the formula:

If that percentage is more than 100%, the small business percentage is 100%.

Step 4 . If your * aggregated turnover for the year is $50,000 or less, multiply the amount at step 2 by the small business percentage: the result is the amount of your * tax offset.

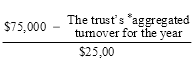

Step 5 . If your * aggregated turnover for the year is more than $50,000, work out the fraction (the small business phase - out fraction ) using the formula:

The amount of your * tax offset is worked out using the formula:

129 Subsection 61 - 505(2) (example)

Omit "an STS taxpayer", substitute "a small business entity".

130 Subsection 61 - 505(2) (example)

Omit "STS group turnover", substitute "aggregated turnover".

131 Subsection 61 - 505(2) (example)

Omit "net STS income", substitute "net small business income".

132 Subsection 61 - 505(2) (example)

Omit "STS percentage", substitute "small business percentage".

133 Paragraph 61 - 510(1)(b)

Omit "an * STS taxpayer", substitute "a * small business entity".

134 Paragraph 61 - 510(1)(c)

Omit " * STS group turnover", substitute " * aggregated turnover".

135 Paragraph 61 - 510(1)(d)

Omit " * net STS income", substitute " * net small business income".

136 Paragraph 61 - 510(1)(e)

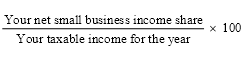

Omit all the words after "a share", substitute "( your net small business income share ) of that net small business income.".

137 Subsection 61 - 510(2) (method statement, steps 3, 4 and 5)

Repeal the steps, substitute:

Step 3 . Work out the percentage (the small business percentage ) using the formula:

If that percentage is more than 100%, the small business percentage is 100%.

Step 4 . If the partnership's * aggregated turnover for the year is $50,000 or less, multiply the amount at step 2 by the small business percentage: the result is the amount of your * tax offset.

Step 5 . If the partnership's * aggregated turnover for the year is more than $50,000, work out the fraction (the small business phase - out fraction ) using the formula:

The amount of your * tax offset is worked out using the formula:

138 Paragraph 61 - 515(1)(b)

Omit "an * STS taxpayer", substitute "a * small business entity".

139 Paragraph 61 - 515(1)(c)

Omit " * STS group turnover", substitute " * aggregated turnover".

140 Paragraph 61 - 515(1)(d)

Omit " * net STS income", substitute " * net small business income".

141 Paragraph 61 - 515(1)(e)

Omit all the words after "a share", substitute "( your net small business income share ) of that net small business income.".

142 Subsection 61 - 515(2) (method statement, steps 3, 4 and 5)

Repeal the steps, substitute:

Step 3 . Work out the percentage (the small business percentage ) using the formula:

If that percentage is more than 100%, the small business percentage is 100%.

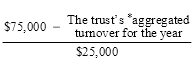

Step 4 . If the trust's * aggregated turnover for the year is $50,000 or less, multiply the amount at step 2 by the small business percentage: the result is the amount of your * tax offset.

Step 5 . If the trust's * aggregated turnover for the year is more than $50,000, work out the fraction (the small business phase - out fraction ) using the formula:

The amount of your * tax offset is worked out using the formula:

![]()

143 Paragraph 61 - 520(1)(b)

Omit "an * STS taxpayer", substitute "a * small business entity".

144 Paragraph 61 - 520(1)(c)

Omit " * STS group turnover", substitute " * aggregated turnover".

145 Paragraph 61 - 520(1)(d)

Omit " * net STS income", substitute " * net small business income".

146 Paragraph 61 - 520(1)(e)

Omit all the words after "a share", substitute "( your net small business income share ) of that net small business income.".

147 Subsection 61 - 520(2) (method statement, steps 3, 4 and 5)

Repeal the steps, substitute:

Step 3 . Work out the percentage (the small business percentage ) using the formula:

If that percentage is more than 100%, the small business percentage is 100%.

Step 4 . If the trust's * aggregated turnover for the year is $50,000 or less, multiply the amount at step 2 by the small business percentage: the result is the amount of your * tax offset.

Step 5 . If the trust's * aggregated turnover for the year is more than $50,000, work out the fraction (the small business phase - out fraction ) using the formula:

The amount of your * tax offset is worked out using the formula:

![]()

148 Section 61 - 525

Repeal the section, substitute:

61 - 525 Meaning of net small business income and small business entity turnover

Net small business income

(1) An entity's net small business income for an income year is the amount by which the entity's * small business entity turnover for the year is more than the sum of the entity's deductions attributable to that turnover.

Small business entity turnover

(2) An entity's small business entity turnover for an income year is the total * ordinary income that the entity * derives in the income year in the ordinary course of carrying on a * business.

(3) In working out an entity's * small business entity turnover for an income year, do not include any amount that is * non - assessable non - exempt income under section 17 - 5 (which is about GST).

149 Subsection 70 - 5(3) (note)

Omit "an STS taxpayer", substitute "a small business entity".

150 Subsection 70 - 35(1) (note)

Omit "an STS taxpayer", substitute "a small business entity".

151 Subsections 70 - 40(1) and (2)

Omit "STS taxpayers", substitute "small business entities".

152 Subsection 70 - 45(2) (table item 5)

Omit "an STS taxpayer", substitute "a small business entity".

153 Paragraph 104 - 235(4)(b)

Omit "STS taxpayers", substitute "small business entities".

154 Subsection 716 - 25(2) (note)

Omit "Simplified tax system", substitute "Small business entities".

155 Paragraph 727 - 15(8)(a)

Repeal the paragraph, substitute:

(a) * small business entities; and

156 Section 727 - 100 (note 2)

Omit "eligible to be an STS taxpayer", substitute "a small business entity".

157 Subsection 727 - 470(2) (heading)

Repeal the heading, substitute:

Entity that is a small business entity, or satisfies the maximum net asset value test for small business relief

158 Paragraph 727 - 470(2)(a)

Omit "eligible to be an * STS taxpayer", substitute "a * small business entity".

159 Subsection 995 - 1(1) (definition of net STS income )

Repeal the definition.

160 Subsection 995 - 1(1)

Insert:

"net small business income" has the meaning given by section 61 - 525.

161 Subsection 995 - 1(1)

Insert:

"small business entity turnover" has the meaning given by section 61 - 525.

162 Subsection 995 - 1(1) (definition of STS annual turnover )

Repeal the definition.

Part 3 -- Application and transitional

Income Tax (Transitional Provisions) Act 1997

163 Subsection 40 - 10(3) (note 2)

Omit "STS taxpayers", substitute "Small business entities can choose to".

164 Division 328 (heading)

Omit the heading, substitute:

Division 328 -- Small business entities

165 Before section 328 - 115

Insert:

In this Division:

"general STS pool" means a general STS pool under old Subdivision 328 - D.

"long life STS pool" means a long life STS pool under old Subdivision 328 - D.

"new Subdivision 328-D" means Subdivision 328 - D of the Income Tax Assessment Act 1997 , as in force after the commencement of this section.

"old Subdivision 328-D" means Subdivision 328 - D of the Income Tax Assessment Act 1997 , as in force immediately before the commencement of this section.

"STS taxpayer" means an STS taxpayer within the meaning of Division 328 of the Income Tax Assessment Act 1997 , as in force immediately before the commencement of this section.

(1) This section applies for the purpose of working out whether you are a small business entity (other than because of subsection 328 - 110(4) of the Income Tax Assessment Act 1997 ) for the 2007 - 08 or 2008 - 09 income year.

(2) You work out your aggregated turnover for the 2005 - 06 or 2006 - 07 income year as if the amendments made by Schedule 1 to the Tax Laws Amendment (Small Business) Act 2007 had been in force in relation to that year.

(3) However, your aggregated turnover for the 2005 - 06 income year is taken to be less than $2 million if:

(a) your aggregated turnover for the 2005 - 06 income year (worked out in accordance with subsection (2)) is $2 million or more; but

(b) your STS group turnover for that year (worked out under Subdivision 328 - F of the Income Tax Assessment Act 1997 , as in force immediately before the commencement of this section) is less than $2 million.

(1) This section applies if:

(a) in the 2007 - 08 income year or a later income year you are winding up a business you previously carried on; and

(b) you were an STS taxpayer for the income year in which you stopped carrying on that business.

(2) The following provisions apply as if you are a small business entity for the income year in which you are winding up the business:

(a) Subdivision 328 - D of the Income Tax Assessment Act 1997 (simpler rules for depreciating assets);

(b) Subdivision 328 - E of the Income Tax Assessment Act 1997 (simplified trading stock rules);

(c) Subdivision 61 - J of the Income Tax Assessment Act 1997 (25% entrepreneurs' tax offset);

(d) sections 82KZM and 82KZMD of the Income Tax Assessment Act 1936 (deducting certain prepaid expenses immediately);

(e) section 170 of the Income Tax Assessment Act 1936 (standard 2 - year period for amending assessments).

(1) For the purpose of working out whether you are a small business entity for the 2007 - 08, 2008 - 09, 2009 - 10 or 2010 - 11 income year (each a relevant income year ) for the purposes of a provision to which subsection (3) applies:

(a) subsection 328 - 125(4) of the Income Tax Assessment Act 1997 does not apply; and

(b) the following subsection applies instead.

(2) An entity (the first entity ) controls a discretionary trust for a relevant income year if, for any of the 4 income years (a previous income year ) before that year:

(a) if the previous income year is before the 2007 - 08 income year--the trustee of the trust made a distribution of $100,000 or more to the first entity, any of its affiliates, or the first entity and any of its affiliates; or

(b) if the previous income year is the 2007 - 08 income year or a later income year:

(i) the trustee of the trust paid to, or applied for the benefit of, the first entity, any of the first entity's affiliates, or the first entity and any of its affiliates, any of the income or capital of the trust; and

(ii) the percentage (the control percentage ) of the income or capital paid or applied is at least 40% of the total amount of income or capital paid or applied by the trustee for that year.

(3) This subsection applies to the following provisions:

(a) Subdivision 328 - D of the Income Tax Assessment Act 1997 (simpler rules for depreciating assets);

(b) Subdivision 328 - E of the Income Tax Assessment Act 1997 (simplified trading stock rules);

(c) Subdivision 61 - J of the Income Tax Assessment Act 1997 (25% entrepreneurs' tax offset);

(d) sections 82KZM and 82KZMD of the Income Tax Assessment Act 1936 (deducting certain prepaid expenses immediately);

(e) section 170 of the Income Tax Assessment Act 1936 (standard 2 - year period for amending assessments).

166 Paragraph 328 - 115(1)(a)

Omit "an STS taxpayer", substitute "a small business entity".

167 Paragraph 328 - 115(2)(a)

Omit "stop being an STS taxpayer", substitute "are not a small business entity".

168 Subsection 328 - 115(3)

After " 1997 ", insert "(as in force immediately before its repeal by Schedule 2 to the Tax Laws Amendment (2004 Measures No. 7) Act 2005 )".

169 Subsection 328 - 115(3)

Omit "an STS taxpayer", substitute "using the STS accounting method".

170 Subsection 328 - 115(4)

After "that Act", insert "(as in force immediately before its repeal by Schedule 2 to the Tax Laws Amendment (2004 Measures No. 7) Act 2005 )".

171 Subsection 328 - 115(4)

Omit "an STS taxpayer", substitute "using the STS accounting method".

172 Section 328 - 120

Repeal the section, substitute:

328 - 120 Continuing to use the STS accounting method

(1) This section applies if:

(a) you were an STS taxpayer for the most recent income year that started before 1 July 2005; and

(b) you continued to be an STS taxpayer until the end of the 2006 - 07 income year; and

(c) you used the STS accounting method for the 2005 - 06 and 2006 - 07 income years; and

(d) you are a small business entity for the 2007 - 08 income year.

(2) You can continue to use the STS accounting method:

(a) for the 2007 - 08 income year; and

(b) for any later income year for which you are a small business entity but only if you used the STS accounting method for the income year before that later year.

Example: You are a small business entity for the 2007 - 08 and 2008 - 09 income years and you continue to use the STS accounting method for those years. You are not a small business entity for the 2009 - 10 income year so you cannot continue to use the STS accounting method for that year. Because you cannot use the STS accounting method for the 2009 - 10 income year, you will not be able to use it again for a later income year even if you are a small business entity for that later year.

173 After section 328 - 125

Insert:

328 - 175 Choices made in relation to depreciating assets used in primary production business

(1) This section applies if:

(a) you were an STS taxpayer for an income year; and

(b) you made a choice under subsection 328 - 175(3) of old Subdivision 328 - D in relation to a depreciating asset you use to carry on a primary production business and for which you could deduct amounts under Subdivision 40 - F or 40 - G of the Income Tax Assessment Act 1997 .

(2) The choice has effect for the purposes of subsection 328 - 175(3) of new Subdivision 328 - D.

Note: This means you cannot change the choice: see subsection 328 - 175(4) of new Subdivision 328 - D.

328 - 185 Depreciating assets allocated to STS pools

Assets allocated to general STS pool

(1) A depreciating asset of yours that had been allocated to your general STS pool is treated as being allocated to your general small business pool.

Assets allocated to long life STS pool

(2) A depreciating asset of yours that had been allocated to your long life STS pool is treated as being allocated to your long life small business pool.

Choice not to allocate assets to long life STS pool

(3) If you made a choice, under subsection 328 - 185(5) of old Subdivision 328 - D, not to have a depreciating asset allocated to your long life STS pool, the choice has effect for the purposes of subsection 328 - 185(5) of new Subdivision 328 - D.

Note: This means you cannot change the choice: see subsection 328 - 185(6) of new Subdivision 328 - D.

328 - 195 Opening pool balances for 2007 - 08 income year

(1) This section applies if a depreciating asset of yours is treated as being allocated to your general small business pool or long life small business pool under section 328 - 185.

(2) The opening pool balance of your general small business pool or long life small business pool for the 2007 - 08 income year is taken to be the closing pool balance of your general STS pool or long life STS pool, as the case requires, for the 2006 - 07 income year, reduced or increased by any adjustment required under section 328 - 225 of new Subdivision 328 - D (about change in the business use of an asset).

(3) However, if:

(a) you were not an STS taxpayer for the 2006 - 07 income year (because you stopped being an STS taxpayer before that time); but

(b) you are a small business entity for the 2007 - 08 income year or a later income year and you choose to use new Subdivision 328 - D to deduct amounts for your depreciating assets for that income year;

the opening pool balance of your general small business pool or long life small business pool includes the sum of the taxable purpose proportions of the adjustable values of depreciating assets allocated to the pool under subsection 328 - 185(3) of new Subdivision 328 - D for that year.

174 Section 328 - 440

Repeal the section, substitute:

328 - 440 Taxpayers who left the STS on or after 1 July 2005

(1) This section applies if you chose to stop being an STS taxpayer for the 2005 - 06 income year or the 2006 - 07 income year.

(2) You cannot choose to use new Subdivision 328 - D to deduct amounts for your depreciating assets until at least 5 years after the income year for which you chose to stop being an STS taxpayer.

Note: Subdivision 328 - D of the Income Tax Assessment Act 1997 continues to apply to depreciating assets that have been allocated to your small business pools even if you are not a small business entity, or do not choose to use that Subdivision, for an income year: see section 328 - 220 of that Subdivision.

175 At the end of Division 727

Add:

(1) This section applies to an indirect value shift if:

(a) the indirect value shift happens in the 2007 - 08 income year or a later income year; and

(b) the scheme that results in the indirect value shift was entered into before the start of the 2007 - 08 income year.

(2) Paragraph 727 - 470(2)(a) of the Income Tax Assessment Act 1997 (as in force immediately before the commencement of this section) continues to have effect in relation to the indirect value shift as if the repeals and amendments made by Schedule 1, Parts 1 and 2 of Schedule 3 and Schedule 8 to the Tax Laws Amendment (Small Business) Act 2007 had not been made.

176 Application

The amendments made by this Schedule apply in relation to the 2007 - 08 income year and later income years.