|

|

Home

| Databases

| WorldLII

| Search

| Feedback

High Court of New Zealand Decisions |

Last Updated: 15 May 2011

IN THE HIGH COURT OF NEW ZEALAND CHRISTCHURCH REGISTRY

CIV-2011-409-000435

UNDER the Securities Markets Act 1988

BETWEEN FINANCIAL MARKETS AUTHORITY (FORMERLY SECURITIES COMMISSION)

Plaintiff

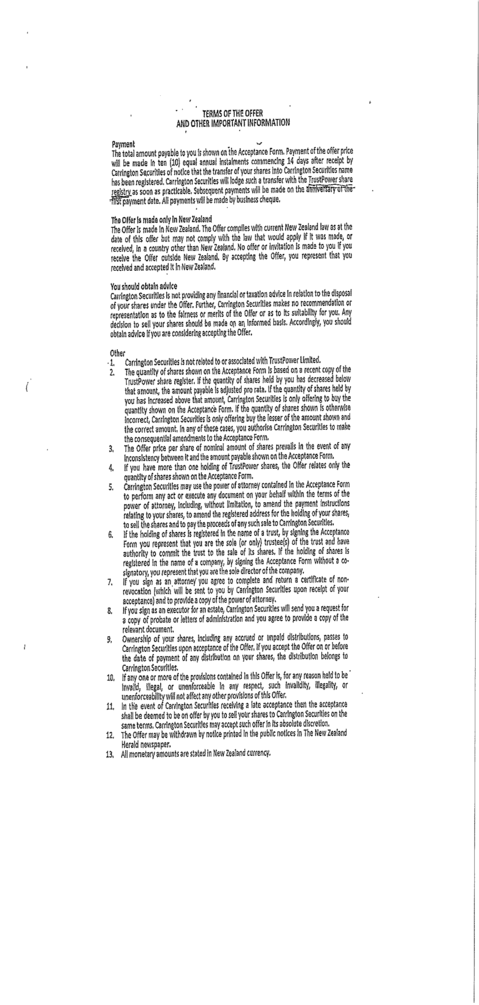

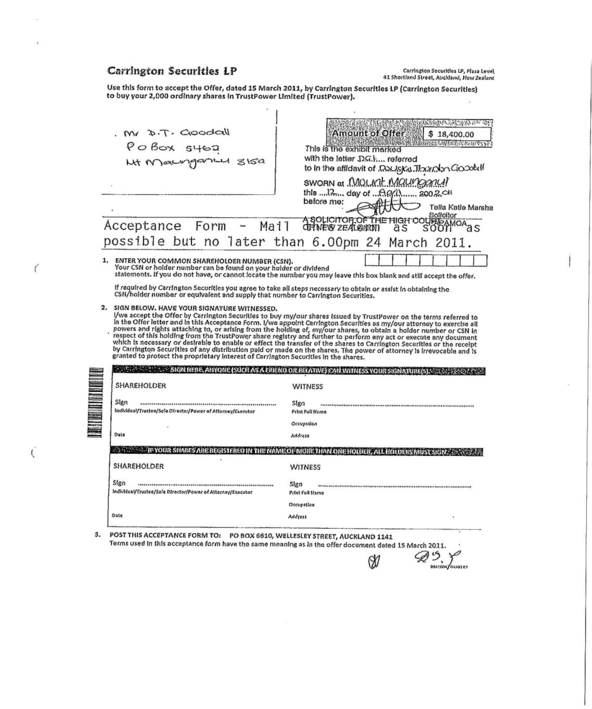

AND CARRINGTON SECURITIES LP First Defendant

AND CHASE SECURITIES LP Second Defendant

AND CARLYLE SECURITIES LP Third Defendant

AND NZ INVESTMENT SECURITIES LP Fourth Defendant

AND ENERGY SECURITIES LP Fifth Defendant

AND POWERSHARES SECURITIES LP Sixth Defendant

AND PEARSON SECURITIES LP Seventh Defendant

AND CARGILL SECURITIES LP Eighth Defendant

AND FAIRFIELD SECURITIES LP Ninth Defendant

AND BERNARD WHIMP Tenth Defendant

Hearing: 9 May 2011 (at Wellington)

Counsel: J B M Smith and F J Cuncannon for Plaintiff

N Till QC and M A L McDonald for Defendants

FINANCIAL MARKETS AUTHORITY (FORMERLY SECURITIES COMMISSION) V CARRINGTON SECURITIES LP HC CHCH CIV-2011-409-000435 12 May 2011

Judgment: 12 May 2011

In accordance with r 11.5 I direct the Registrar to endorse this judgment with the delivery time of 4.00pm on the 12th day of May 2011.

RESERVED JUDGMENT OF GENDALL J

[1] These proceedings were brought by the Securities Commission (the Commission) against nine defendants, which are Limited Partnerships and a tenth defendant, Bernard Whimp, the General Partner that is “managing” in respect of each. The Commission was disestablished on 1 May 2011 by the Financial Markets Authority Act 2011. That Act provides that proceedings brought by the Commission may be continued by its replacement Authority, namely the Financial Markets Authority (FMA), without amendment.

[2] The essence of the first cause of action in the proceedings is that Mr Whimp, and six of the Limited Partnerships made offers to purchase shares in a number of public companies in the form of “Deferred Payment” Offers which were said to be misleading and deceptive, in breach of s 13 of the Securities Markets Act 1988 (the Act).

[3] In a second cause of action the FMA pleads that Mr Whimp and eight of his Limited Partnerships made offers to shareholders in public companies in the form of Cash Offers which were also misleading and deceptive (for different reasons), also in breach of s 13 of the Act.

[4] The hearing before me proceeded only in relation to the “Deferred Payment” Offers. The second cause of action relating to the earlier separate Cash Offers has been adjourned, by consent, for later determination.

[5] Shortly before the hearing commenced the Court was advised that the issue for it to determine was one of relief. Although Mr Whimp and his Limited Partnerships did not consent to a finding, nor concede, that the

“Deferred Payment” Offers were misleading and deceptive so as to breach s 13 of the Act, they did not pursue any active opposition. But, naturally, the granting of relief by the Court under ss 42K, 42L and compensatory orders under ss 42ZA,

42ZB, 42ZF (as sought by the FMA) of the Act is dependent upon there being a finding that s 13 has been contravened. So a summary of the factual background is necessary.

Background

[6] The FMA has filed extensive affidavits from the Director of the former Commission, an expert accountant, an expert NZX advisor, and several shareholders in public companies to whom “Deferred Payment” Offers were sent. The defendants have filed one affidavit from an expert accountant. There is no other evidence from Mr Whimp, or on his behalf, dealing with the substance of the allegation that he engaged in dealings that were misleading or deceptive or were likely to mislead or deceive. All he has filed is a procedural discovery affidavit and assertion as to what he has done since an interim order was made by Miller J on 24 March 2011.

[7] The first to fifth defendants and the ninth defendant were registered as Limited Partnerships on 17 December 2010 (apart from Carrington Securities LP which was registered on 13 July 2010). Mr Bernard Whimp is the tenth defendant and the General Partner with a recorded address in Sydney, Australia, although I am told from the Bar that he now resides in Christchurch. Particulars of any Limited Partner or the Partnership Deed are not known to the Court or to anyone else and are not available through a search of the Register, because of s 64(2) of the Limited Partnerships Act 2008.

[8] The first cause of action arises out of a procedure adopted by Mr Whimp to make offers in the names of the Limited Partnerships to selected shareholders in a number of public companies. Those companies are TrustPower Limited, Guinness Peat Group plc, Contact Energy Limited, Vector Limited, DNZ Property Fund Limited, and Fletcher Building Limited. The share registers of those companies were made available to Mr Whimp and offers were made through the agency of each Limited Partnership on 15 March 2011. They were to shareholders who generally

had smallish holdings in the companies, and to investors such as fund managers and entities that might be described as discerning large-scale shareholders.

[9] FMA contends that the offers were devised so as to deceive and mislead shareholders. In each of the communications the offered share price exceeds the current share trading price of the company by a significant margin. That is the “bait”. However, the document contains in smaller and finer print on its later page terms of the “Deferred Payment” which derogated from the impression created by the particular offer and clearly intended to be so created that the offer was very attractive. This fine print includes the crucial provision that payment of the offered price would be made in ten annual instalments.

[10] Evidence filed on behalf of the FMA is that the “Deferred Payment” Offers whilst on their face appear to be for consideration higher than the current market value of the shares, the overall terms of the offer are deceptive and misleading so that many shareholders would not clearly understand the effect of the terms of payment for the offer being made.

[11] In fact, FMA received numerous complaints about these offers from shareholders who found them to be misleading and from other shareholders who accepted the offers as a result of being deceived and misled, which they realised too late. Complaints were also received by representatives of the targeted companies through concern that their shareholders may be misled.

[12] The opinion of the FMA is expressed in the first affidavit of Susan Brown in which she says:[1]

This concern is accentuated by the fact that the font size of the headline of the offer (containing the share price) is larger than the terms of payments and the latter were of a compressed line spacing. Further, and in particular, it was not made clear to shareholders that:

(a) there would not be interest payable on the outstanding instalments so that, in real terms, the value of the instalment would decrease over time;

(b) for the 10 year period the recipient of that letter would be an unsecured creditor of the relevant Limited Partnership and is therefore reliant on the creditworthiness of the relevant Limited Partnership [and I add of its managing partner Mr Whimp];

(c) any returns on the shares during the 10 year period would accrue to the relevant Limited Partnership; and

(d) the net present value of the offer price was less than the amount the shareholder would receive if they sold the shares through a sharebroker at their current trading price.

[13] The offer document emphasises the contrast between the offer price and current share price. The deal looks at first sight very attractive. The offer includes phrases such as “first come, first served” and “offer limited” so as to instil into the recipient a sense of urgency if he/she was to take advantage of the bargain. Although full terms of the payment are printed on the back page, it is said that they are not sufficient to overcome the misleading impression created by the offer letter.

[14] Annexed hereto is a copy of one of the “Deferred Payment” Offers, which is

common to all sent to shareholders in the several companies:

[15] As at 13 April 2011 the FMA had received 69 complaints in respect of the “Deferred Payment” Offers. On 29 March 2011, Discovery showed that there had been acceptances of 647 “Deferred Payment” Offers, and by 12 July 2011 a further

528 acceptances. So, in all there were 1,175 acceptances for the “Deferred Payment” Offers in respect of those six companies. These represented 2,102,621 shares in the six companies.

[16] A summary of the consideration in respect of each of those acceptances, in each company, based upon the offered price:

|

Company

|

Acceptances

|

Shares

|

$ value at offer price

|

|

TrustPower Limited

|

45

|

72,880

|

670,496.00

|

|

Guinness Peat Group plc

|

84

|

560,677

|

616,744.70

|

|

Contact Energy

Limited

|

446

|

375,005

|

2,850,038.00

|

|

Vector Limited

|

426

|

482,899

|

1,545,276.80

|

|

DNZ Property Fund

Limited

|

42

|

498,746

|

822,930.90

|

|

Fletcher Building

Limited

|

132

|

112,414

|

1,292,761.00

|

|

Total

|

1,175

|

2,102,621

|

7,798,247.40

|

[17] Given total consideration of $7,798,247.40, the initial one-tenth payments required to be made by the Limited Partnerships would therefore be $779,824 and thereafter $7,018,423 would remain as the total unsecured debt of the six Limited Partnerships.

[18] I do not consider Mr Whimp devised the strategy of the “Deferred Payment” Offers through creation of Limited Partnerships and the offers in this form, from any original thought. If he did, he does not say so. They bear close similarity to offers made by an Australian man, Mr David Tweed, through a company, National Exchange Pty Limited, to purchase shares at an offer price in excess of total “market price” on a “Deferred Payment” scheme ( with payment to be made over

15 years). They were the subject of proceedings brought by the Australian Securities

Investments Commission, leading to the decisions National Exchange Pty Ltd (ACN

006 079 974) v Australian Securities & Investments Commission.[2] It was alleged

that Mr David Tweed had aided, abetted, counselled and procured the contraventions of the Corporations Act 2001, being offers which were misleading, deceptive, or likely to mislead or deceive. There Finkelstein J, at first instance said:[3]

... it is impossible to ignore the fact ... that the offer has been purposely composed so that it will mislead shareholders. No reasonable shareholder appreciating the offer price is payable over 15 years would accept it.

[19] Although the liability of Mr Whimp and his Limited Partnerships does not depend upon proof of intention to mislead or deceive, I consider those remarks are equally apt in this case, despite the time period being ten years, because it is a significant period during which Partnerships, and the unstated alter ego of them, would be unsecured debtors, matters necessarily bound up in the composition of the offer.

[20] As Mr Whimp has adduced no substantive evidence, it is not known whether he took legal advice before instigating such offers. If he did, he must surely have been advised of that case and known what the Australian Courts had said about them. If he did not take any advice, the similarities are such that an inference is available that he knew at least something about this strategy. I am bound to draw, as I do, that he purposely composed the offer documents to catch some smaller shareholders off guard.

Statutory provisions

[21] Section 13 of the Act provides that:

(1) A person must not engage in conduct, in relation to any dealings in securities, that is misleading or deceptive or likely to mislead or deceive.

(2) To make the position clear, this section applies more broadly than the rest of this Part and so applies to securities whether listed or non- listed and to all dealings in securities (not only trading).

[22] Section 19 provides:

A court hearing a proceeding brought against a person under the Fair Trading Act 1986 must not find that person liable for conduct that is regulated by this Part if that person would not be liable for that conduct under this Part.

[23] The phrase “misleading or deceptive or likely to mislead or deceive” is common to s 9 of the Fair Trading Act and s 13 of the Securities Markets Act. Section 13 essentially is the Securities Markets Act equivalent of s 9. But for s 19, there would be a duplication between the two offences. Section 13 approximates, when dealing in securities, to the prohibition in s 9 of the Fair Trading Act 1986 of misleading or deceptive conduct.

Discussion

[24] A summary of the principles to determine whether conduct is actually or potentially misleading or deceptive is set out by McGechan J in Taylor Bros v Taylors Group Ltd:[4]

(a) Conduct cannot, for the purposes of sec 52, be categorised as misleading, or deceptive, or likely to be misleading or deceptive, unless it contains or conveys a misrepresentation: Taco Company of Australia Inc v Taco Bell Pty Limited (1982) ATPR para 40-303 at p 43,751; [1982] FCA 136; (1982) 42 ALR 177 at p 202.

(b) A statement which is literally true may nevertheless be misleading or deceptive: see Hornsby Building Information Centre Pty Limited v Sydney Building Information Centre Ply Limited (1978) ATPR para 40-067 at p 17,690; [1978] HCA 11; (1978) 140 CLR 216 at p 227. This will occur, for example, where the statement also conveys a second meaning which is untrue: World Series Cricket Pty Limited v Parish (1977) ATPR para 40-040 at p 17,436; (1977) 16 ALR 181 at p 201.

(c) Conduct is likely to mislead or deceive if this is a „real or not remote chance or possibility regardless of whether it is less or more than 50 per cent‟: Global Sportsman Pty Limited v Mirror Newspapers Limited (1984) ATPR para 40-463 at p 45,343; [1984] FCA 180; (1984) 55 ALR 25 at p 30.

(d) The question whether conduct is, or is likely to be, misleading or deceptive is an objective one, to be determined by the Court for itself, in relation to one or more identified sections of the public, the Court considering all who fall within an identified section of the

public „including the astute and the gullible, the intelligent and the not so intelligent, the well educated as well as the poorly educated, men and women of various ages pursuing a variety of vocations‟: Taco Company at ATPR p 43,752; ALR p 202. Evidence of the formation in fact of an erroneous conclusion is admissible but not conclusive: Global Sportsman at ATPR p 45,343, ALR p 30.

(e) Ordinarily, mere proof of confusion or uncertainty will not suffice to prove misleading or deceptive conduct: Parkdale Custom Built Furniture Pty Limited v Puxu Pty Limited (1982) ATPR Para 40-

307; [1982] HCA 44; (1982) 149 CLR 191. However, where confusion is proved, the Court should investigate the cause; so that it may determine whether this is because of misleading or deceptive conduct on the part of the respondent: Taco at ATPR p 43,752; ALR p 203.

[25] Conduct that is misleading or likely to mislead so as to amount to a false representation is a question of fact to be decided objectively, the intention of a defendant being irrelevant, although if existing may be persuasive. What is necessary is there be a likelihood or reasonable possibility that persons to whom the offer is directed will be misled. It is not necessary to show actual deception, even though, in this case the FMA has filed six affidavits from persons who accepted the “Deferred Payment” Offer and were actually misled. Some were careful, some busy, some did not understand the full import of the offer, some overlooked the fine print, and some believed they had to act quickly because of time limits imposed on the offer. All did not understand the full import of accepting the offer.

[26] As I have said the “Deferred Payment” Offers bear considerable similarity to those in the National Exchange Pty case, where the offers were held to be misleading and deceptive even though showing, more prominently (than in this case) on the front page of the offer the fact that the payments were to be deferred over 15 years. In the present case the fine print payment terms are on the second page. But common features are the prominently displayed comparison between the offer price and the market price to highlight the apparent financial benefit that could be achieved by accepting. There is common reference to a closure date occurring on receipt of 1,000,000 shares. The words “first come, first served” basis are used in both forms. Both state that no brokerage is payable and there is reference to cheques being posted to the recipients at certain times. There is a “recommendation” that independent advice be obtained and that the offer is not to be construed as a

recommendation that the recipients sell their share. The time available within which such advice could be sought in the present case was impossibly short.

[27] The offer in National Exchange Pty Ltd may on its face be clearer and less deceptive, given the manner in which the information is set out on the front and only page. Yet Finkelstein J at first instance was left with the clear impression that a number of shareholders would have wrongly formed the view, that they received a cash offer for their shares and may not have stopped to analyse the offer in debt

being influenced by the general impression which was misleading. He said:[5]

The section is not there for experts; it is there to protect the general shareholding public, many of whom do not analyse offer documents in any great detail, but act on appearances and impressions. This cannot be characterised as unreasonable conduct on their part. It is just the natural order of things.

[28] His Honour said:[6]

... little is known about the shareholders save that they have a small shareholding in Onesteel. It is, however, appropriate to proceed on the assumption that the shareholders who received the offer include the educated as well as the uneducated, the thinking as well as the unthinking, the credulous as well as the cautious. Moreover, given their likely diversity, it is reasonable to act on the basis that many shareholders will not weigh each word of the offer as an educated or analytical mind might do. Nor will they necessarily subject the offer to close scrutiny.

[29] So an offer which is factually true may plainly be misleading and that was found to be the case at first instance. On appeal Dowsett J made it clear that the subsequent provision for “Deferred Payment” significantly undermined the validity of any comparison between that which was invited, namely the offer price and current market price because the comparison as between “likes”; the invitation implying the shareholder would be better off if he or she accepted rather than

rejected. Dowsett J said:[7]

Price is usually of pre-eminent importance in an offer to purchase property of any kind. Terms of payment might reasonably be treated by some people as being of subsidiary importance. An offeree would not normally expect

that information as to payment would have the effect of substantially undermining the correctness of information found elsewhere in the document, particularly information as to a matter of pre-eminent importance such as price. The prominence of the invited comparison in the offer documents and the absence of any reference to deferred payment in the share transfer form would have further discouraged any such expectation.

[30] And further:[8]

I am conscious of the traditional caution exercised by courts in determining whether or not a person deliberately intended to mislead. However ... it is impossible to imagine even the most unworldly of investors finding the offer attractive, given the arrangements for deferred payment of the purchase price. It is of some significance that the National Exchange sent the vast majority of the offers to the holders of relatively small parcels of shares. Such persons, or some of them, could have been expected to pay less attention to the offers than they would if large holdings were involved.

[31] And further:[9]

No doubt, a sceptical shareholder would look for the “catch” but in my view, many reasonable shareholders would have been inclined to accept the offer at face value, assuming that conditions as to payment would be subsidiary and not such as significantly to reduce the value of the offer or the favourable comparison of it with the market place. It may be that many reasonable shareholders would, before finally accepting, have read the documents more closely and more critically. However I am satisfied that not ever reasonable shareholder in the class would have done so.

[32] Similar views are expressed by Jacobson and Bennett JJ, where they said:[10]

The striking feature of the document when read as a whole is the disparity between the impression created by the primary statement, namely that the offer is for payment in full on acceptance, and the true position stated in the qualification under which payment is to be made over 15 years. The primary statement is made in bold so as to emphasise it to the reader and is repeated and reinforced in the comparative table.

The representation made in the table is that the shareholders will receive in cash in full on acceptance a premium ... over the closing price. The true position is that accepting shareholders make an interest free loan of the purchase price to the appellant over a period of 15 years. To describe it as a cheeky offer would be to understate the full import of the document.

[33] In assessing present value of the offer a crucial issue has to be the risk associated with any unsecured loan made over an extended period to a person or his

partnerships in such circumstances. It is for that reason that I do not accept the opinion evidence of Mr Hadlee, filed on behalf of the defendants, that in assessing the present value of the “Deferred Payment” Offers the appropriate interest (discount) rate to be calculated on the unpaid balance of an unpaid purchase price was six per cent – and that he disagreed that the rate assessed by the expert of the FMA, 17 – 19 per cent, was appropriate.

[34] The crucial issue, in determining present value, must be whether the lenders are prepared to lend to the particular borrowers unsecured amounts on a long-term basis. The extent of the risk in many respects governs the interest content. Whilst Mr Hadlee says it is inappropriate to adopt bank unsecured lending rates of 17 – 19 per cent to judge the fairness or otherwise of the defendant‟s offer because this rate was not available to shareholders as “they were not banks”, this overlooks the essential question. That question is, whether the shareholders firstly knew or understood they were making unsecured personal loans to the entities involved; and secondly, the identity of them as “lenders” not being a bank, is not what is relevant, but rather status and standing and credit worthiness of the borrowers, when assessing risk.

[35] In the end, I am satisfied on all the evidence that the present value of what was being offered (and largely taken as unsecured loans) and other factors resulted in the present value of the consideration offered being significantly below that of the market price or values of the shares. I accept the assessment of values as provided by Mr Dent on behalf of the FMA in para 5.2 of his first affidavit.

[36] It is clear that the degree of prominence required in the aspect of the qualification or fine print explanation will vary with the potential for the primary statement to be misleading or defective. The question will remain whether the later small print has a link to the additional information, which is sufficiently prominent to prevent the original statement being misleading and deceptive, or likely to mislead to deceive.

[37] Just as the Fair Trading Act is legislation aimed at consumer protection, so too, in the context of offers made to shareholders, is s 13 aimed at protection of the

public against those who engage in conduct that is misleading or deceptive, or likely to mislead or deceive.

[38] I agree with Mr Smith‟s submissions that the Court need not go further than the remarks contained in National Exchange Pty Ltd. I agree with them. As I have said, there are very clear similarities in respect of the offers in this case and those distributed in that case (apart from the term being 15 years rather than ten years) and indeed the later qualifications in the present case are more subtly made in fine print than existed in National Exchange Pty Ltd.

[39] I accept the argument that the liability of the Limited Partnerships and Mr Whimp in respect of the first cause of action is clearly established. The offer is likely to be misleading and deceptive, as objectively determined by the Court. None of the defendants actively contested that proposition. They simply did not concede any misleading or deceptive behaviour. Even if the test was “beyond reasonable doubt” (which it is not) I am well satisfied to that standard. The impression is clearly given that full payment would be made immediately or promptly, and that the offer price, presented on the face of the document as a comparison with the current market price represented a value exceeding the current share trading price when that was not accurate.

[40] Likewise, the document does not convey clearly that the consideration for the acquisition of the shares was, to the extent of 9/10ths an unsecured loan to Limited Partnerships about which no information was given. Nor was any information given about the credit worthiness of Bernard Whimp, the General Partner who has residual liability for the obligations of the Limited Partnerships. He is not referred to in any of the offers. Those who accept the offers, because of the “bait” initially provided,

are contracting to make unsecured long-term loans to entities about which nothing is known. Mr Whimp operated on the basis of the maxim of “let the buyer beware” but did so through a misleading and deceptive mechanism. Any reasonable shareholder in these public companies, if understanding he/she was to make extended unsecured loans essentially to Mr Whimp through the agency of his recently created Limited Partnerships, would have appreciated or understood that the present value of the offer was well below the figure being offered. Those who have already affirmed

their acceptance and wish to proceed, are entitled to do so, but the likelihood is that they may remain misled into thinking that there is some commercial bargain in it for them.

[41] In terms of the amended statement of claim the cause of action alleging misleading or deceptive conduct in respect of the “Deferred Payment” Offers in breach of s 13 of the Act has been established.

Remedy/relief

[42] The FMA submitted draft orders that it seeks. The defendants through Mr Till QC, have proposed different forms of relief. I do not consider the defendants are in any position to “negotiate” the form of relief that they might find acceptable.

[43] The evidence before the Court is that Mr Whimp had previously been subject to an order prohibiting him from managing companies under s 385 of the Companies Act 1993. This was for a period of four years from 30 October 2006, for reasons which are set out in the Notice and Minute of the Deputy Registrar of Companies presented to the Court. Discussion and detail of why this came about is not required.

[44] In addition, Mr Whimp has convictions entered in the Christchurch District Court on 8 October 2008 for 14 breaches of the Companies Act 1993 and for burglary. It is said on his behalf that these all related to his own property and concerned companies in which he was involved. They are matters which might be relevant to assessment of any risk in lending, essentially, to him, but obviously, did not have to be disclosed in the offer documents – yet are relevant to issues of remedy or relief.

[45] The proposed certain orders as being required by the FMA are contained in a draft submitted by Mr Smith.

[46] But the defendants and Mr Whimp seek to negotiate, or propose, alternative orders or requirements.

[47] Mr Till QC on behalf of the defendants accepts that shareholders who do not wish to proceed cannot be held to their acceptances. He says that those who have elected to proceed (149 out of 1,175) should be bound by that election. It appears that 17 confirmations were sent to the FMA and 132 confirmations sent to one or other of the defendants. The FMA has concerns about those 132 and wishes to make further inquiries. For that reason it sought 20 working days after orders are made to undertake investigations.

[48] The proposed notice that accompanied the interim order of Miller J required, amongst other things, confirmations from those wishing to proceed with the sale to be sent to the Securities Commission only. But for a number of reasons this did not occur. Mr Whimp, through his partnerships himself sent out notices, some of which omitted matters contained in form of the order proposed by Miller J.

[49] What Mr Till QC on behalf of the defendant says is that there should be a further opportunity for shareholders to “opt in or opt out” of their contracts. That is, there is a third category of the 1,175 original acceptors of the offer, comprising those who did not respond to the letter sent by the then Securities Commission. That letter asked shareholders:

If you would like to proceed with the sale whether or not the Court decides the offer was misleading you may do so. In that case you should sign this document where indicated below and return it to the Securities Commission in the envelope supplied.

[50] Accompanying this, was a further letter, which said the recipient was about to receive, if they had not already done so, the notice from the Securities Commission about the offer and it says:

You don‟t have to do anything now, but you may decide to go ahead and sell your shares regardless of whether the Court says the offer was misleading or not.

DO NOT SIGN and return the notice UNLESS you want to go ahead and sell your shares to [the Limited Partnership].

Mr Till QC says that those who did not respond should now be given the option to respond and affirm or otherwise the contracts.

[51] The proposed orders he submits on behalf of Mr Whimp and the Limited

Partnerships provide essentially:

![]() contracts made on acceptance of the “Deferred

Payment” Offer can be

contracts made on acceptance of the “Deferred

Payment” Offer can be

“terminated at [the election] of the shareholders”;

![]() a compensatory order cancelling contracts of those

who have

a compensatory order cancelling contracts of those

who have

communicated a wish to terminate their contract may be made;

![]() that “middle group” of shareholders who have

communicated nothing back to the Commission they have 28 days after dispatch

of

a letter to them revoking their contract, but otherwise the registration of

the

that “middle group” of shareholders who have

communicated nothing back to the Commission they have 28 days after dispatch

of

a letter to them revoking their contract, but otherwise the registration of

the

transfer of their shares can proceed. [Italics mine]

[52] Mr Till QC says this is a mechanism that was adopted by Finkelstein J at first instance in National Exchange Pty Ltd. But in that case Finkelstein J stated:[11]

I have mentioned that a handful of people have accepted the National Exchange offer. National Exchange is willing to allow these shareholders 28 days within which to revoke their acceptance. To this end I will require National Exchange to send to all accepting shareholders a letter giving them notice that any contract made on acceptance of the offer can be terminated at their election.

But here that has already been done, not to a “handful” of shareholders, but to more than a thousand. The letter suggested by Finkelstein J and also now suggested on behalf of Mr Whimp, makes no reference to the order that the defendants propose the Court make, namely that shareholders who do not respond to this further letter are bound by the acceptance.

[53] The contents of the letter submitted by counsel‟s memorandum of 11 May

2011 on behalf of the defendants makes no reference to a shareholder being bound if he/she does nothing.

[54] It seems that Mr Whimp‟s sanguine expectations and optimism have no

bounds. That letter, subtly, does not tell the recipient that failure to respond binds

him/her to a contract. The letter suggested by the defendants (and I presume Mr Whimp) simply says the FMA “brought proceedings against us alleging that the offer is misleading”. It does not say what the Court has found, nor, crucially, the reasons why it has found deception. The letter again places the onus on the shareholder to say if they “wish to terminate the contract”. Yet the order proposed by the defendants places an onus on the shareholder to respond otherwise they are bound to their contracts. The letter that Mr Whimp or the defendants wish to send to shareholders does not say that if they do not within 28 days respond by “revoking the contract” then they are bound by it. So, Mr Whimp can proceed to register the share transfers if these shareholders do not reply. It is a strategy which the Court will not permit.

[55] The proposal advanced by the defendants as to relief which they would like to see happen is totally unacceptable. Contracts arising from acceptances not already affirmed are to be terminated. This legislation is designed to protect the public which includes the gullible and those who are not careful. Remedial orders can only be made upon a finding that there has been misleading and deceptive conduct, which I have found that to be clear beyond any question. The smaller shareholders were in my view specifically targeted through the sending of notices to them, which they did not solicit. Those who accepted and who have already said they wish to affirm their acceptances – despite knowledge of what has occurred – may do so. But I am clear that remaining shareholders ought not be subject to further communications, as they have not already acted to affirm their contracts. It is not now for the shareholders to determine whether contracts are binding on them. It is the Court‟s responsibility to make the remedial orders necessary to protect them and I propose to exercise my discretion to do so. Just as the offer could be described as “cheeky”, so any scheme under which shareholders who do not reply to the defendants‟ letter within 28 days and revoke their contracts, will have their share transfers registered, is an artifice.

[56] I agree with Mr Smith that the FMA should have time to investigate the 132 confirmations sent to one or other of the defendants. It is untenable that there be continued uncertainty or absence of finality or room for confusion. In the exercise of my discretion I am not prepared to order that “silent” shareholders should receive

any further communications, or be under any obligation to communicate affirmation or denial of their contracts.

[57] The Court may cancel the contract under s 42ZB of the Act and it may make such a compensatory order if satisfied there is a contravention of civil remedy provision and that an “aggrieved person” is likely to suffer loss or damage because of that contravention. The “aggrieved person” need not be a party to the proceedings. I am satisfied that there are “aggrieved persons” likely to suffer loss or damage arising out of the misleading or deceptive conduct, and that those contracts which have previously not been affirmed should be cancelled as part of the exercise of the Court‟s discretion. Those contracts will be cancelled apart from any which are contained within the Schedule of the draft orders submitted on behalf of the FMA.

[58] Under s 42K of the Act the Court may grant an injunction to restrain the defendants from engaging in similar conduct that constitutes a contravention of the Act. Section 42L provides further guidance. The Court may grant an injunction where satisfied that a person has engaged in prohibited conduct or it appears that if an injunction is not granted is likely to engage in conduct of that kind. I am satisfied that a permanent injunction should be made. That, and the further orders proposed by the FMA should be made. Those orders are:

(1) Pursuant to s 42K of the Act a permanent injunction restraining the First, Second, Third, Fourth, Fifth, Ninth, and Tenth Defendants from making offers in the form of the offer attached to this order or in any substantially similar form.

(2) Pursuant to ss 42ZA and 42ZB(c)(ii) of the Act, a compensatory order cancelling any contract formed by one of the First, Second, Third, Fourth, Fifth, and Ninth Defendants with a recipient of the “Deferred Payment” Offers (as defined in the Amended Statement of Claim). Subject to order 5 below, this order does not apply to the contracts contained in the schedule of contracts attached to this order.

(3) Pursuant to ss 42ZA and 42ZB(b) of the Act, a compensatory order directing the return of any shares that have been transferred to the First, Second, Third, Fourth, Fifth, and Ninth Defendants pursuant to a contract formed with a recipient of the “Deferred Payment” Offers. Subject to order 5 below, this order does not apply to the contracts contained in the schedule of contracts attached to this order.

(4) Pursuant to s 42ZF(b) of the Act, an order restraining the registration of any shares acquired by the First, Second, Third, Fourth, Fifth, and Ninth Defendants pursuant to a contract formed with a recipient of the “Deferred Payment” Offers. Subject to order 5 below, this order does not apply to the contracts contained in the schedule of contracts attached to this order.

(5) Order 1 shall take effect immediately. Orders 2 to 4 inclusive will take effect 25 working days after they are made, during which time the interim order made by the Miller J on 24 March 2011 will continue in effect. At any time within the period of 25 working days, the FMA may apply to vary orders 2-4 including, without limitation, to have any of the contracts referred to in the schedule removed from the schedule.

(6) The Defendants are to provide discovery of copies, and the originals for inspection if required, of the 132 purported affirmations of acceptance of the “Deferred Payment” Offer they have received to the FMA by 5pm on Wednesday 18 May 2011. If they do not do so, the FMA has leave to apply to the Court for an extension of the time provided for in order 5.

[59] The orders are not to apply to the “Deferred Payment” Offers accepted by those 17 named persons in the Schedule (attached) and which are to annexed to the order itself and the 132 affirmations it is said have been received by the defendants which may be the subject of the FMA applying to vary orders 2-4 should any of those contracts be required to be removed from the Schedule.

[60] The FMA is entitled to costs against each of the first to fifth defendants, the ninth defendant and the tenth defendant jointly and severally. At the request of Mr Smith on behalf of the FMA, quantum of costs is to be reserved pending the final determination of the second cause of action or earlier application by the FMA.

[61] Leave is reserved to the parties to come back to the Court should there be the need for further orders or variations to them.

[62] The parties will note that the timetable contained in order (5) has been

enlarged to “25 working days” and the provision of documents required in (6) is to

be by Wednesday 18 May 2011.

J W Gendall J

Solicitors:

Meredith Connell, Auckland for Plaintiff

R A Fraser & Associates, Christchurch for Defendants

Schedule of Contracts

The Orders of the Court do not apply to the Deferred Payment Offers accepted by:

1 Aitken, M E

2 Bhola, S

3 Carroll, M S

4 Casey, L M

5 Cummins, S A

6 Goatham, L A

7 Hannah, P M

8 Hsu, C W

9 Kelley, J

10 Li, J

11 McNeill, R

12 Pearson, M J

13 Rogers, J L

14 Sarich, P

15 Su, R

16 Walker-Mead, B W

17 Wong, GC & F

18 Those 132 affirmations referred to in [58](6)

[1] Affidavit of Susan Brown sworn 23 March 2011 at Wellington at 3.6.

[2] National Exchange Pty Ltd (ACN 006 079 974) v Australian Securities & Investments Commission [2004] FCAFC 90; at first instance, Australia Securities and Investment Commission v National Exchange Pty and Anor [2002] ALR 24. Special leave to appeal declined by High Court, [2004] HCA Trans 557.

[3] Australia Securities and Investment Commission v National Exchange Pty and Anor [2002] ALR 24 at 30

[4] Taylor Bros v Taylors Group Ltd [1988] 2 NZLR 1 at 28 (HC); confirmed on an appeal by the Court of Appeal ) at 33.

[5] Australian

Securities and Investments Commission v National Exchange Pty Ltd, above n

2, at [20].

[6] At

[12].

[7]

National Exchange Pty Ltd (ACN 006 079 974) v Australian Securities &

Investments Commission, above n 2, at

[38].

[8] At

[39].

[9]

At

[42].

[10] At

[53] – [54].

[11] At [22].

NZLII:

Copyright Policy

|

Disclaimers

|

Privacy Policy

|

Feedback

URL: http://www.nzlii.org/nz/cases/NZHC/2011/80.html