Journal of Law and Financial Management

|

|

Home

| Databases

| WorldLII

| Search

| Feedback

Journal of Law and Financial Management |

|

By: Josephine Diane Donato - BEco (Honours)

Increased competition in the Australian lending market over recent years has forced authorised deposit-taking institutions (ADIs) to attract and retain customers by means of relaxing lending standards. As larger amounts are granted, it appears credit is more easily available to borrowers in comparison to the past. The industry has further experienced significant growth in non-conventional products, such as low-documentation loans, which are generally offered at rates close to the standard rate for traditional loans. While these changes may not create problems during times of strong economic conditions, they are likely to exacerbate loan losses if economic conditions deteriorate, as it seems as if ADIs have taken on more risk in order to stay competitive.

The aim of this paper is to examine how lending market competition affects banking institutions’ credit risk and performance within Australia. Thus, I hypothesise that increased competition leads to a rise in credit risk and that increased competition tends toward a reduction in performance, I test these hypotheses using linear regression.

For a long time, the Australian financial industry has been highly regulated. The deregulation of the Australian financial system between 1983 and 1985 brought to the forefront a pathway of accelerated lending competition, whereby banking institutions began to compete through reductions in required collateral and lower interest rates. Banking institutions and regulators have moved from an environment focused on the tight control of credit risk to one which allows banking institutions considerably more discretion with respect to their lending practices and the degree of credit risk taken.

In her article Moullakis (2006) expresses the concern that banks are relaxing their lending policies in order to keep up with the pressure of competition within the market and particularly to maintain market share. This concern focuses on those lending institutions that provide low-document and no deposit loans in an attempt to increase their home loan volumes. Even the governor of the Reserve Bank of Australia (RBA), Ian Macfarlane, makes the point that

“…it is not unusual during times when sentiments of risk are at their minimum, over-confidence can take over and elementary precautions start to diminish” (Macfarlane, I. 2004: 1).

Thus, competitive pressures from those who under-estimate risk can push even those more prudent institutions into actions otherwise not taken without such pressure. Accordingly, increased competitive pressures in the lending market over recent years may have forced banking institutions to attract and retain customers by means of more relaxed lending standards. Hence, there are concerns about the increased credit risk associated with such practices.

Despite previous research, the relationship between competition and credit risk in lending markets are still a largely unexplored topic. Consequently, it is implausible to rely completely on general insights from the traditional literature in industrial economics. The aim of this paper is to contribute to the better understanding of how competition affects performance, but in particular credit risk in Australian banking institutions. I analyse whether there is a relationship between competition and credit risk, and competition and performance. If such relationships exist, to further examine their nature. Thus, this paper tests the hypothesis that increased competition within the lending market leads to an increase in bank credit risk and a fall in bank performance. This will assist in providing an indication for future trends should competition within the Australian lending market increase at a rapid rate.

The remainder of this paper is structured as follows. The next section discusses selected prior research, followed by an overview of competition, credit risk and performance within the Australian lending market. Section three addresses the measures employed for analysis, section four establishes the models used and the subsequent section evaluates the results and the final section concludes the paper.

A significant amount of literature has been centered upon the areas under discussion within the financial services lending sector. However, the excess of theoretical and empirical investigations focus on these areas separately, with less research concentrated on linking credit risk and performance with competition.

The banking industry is largely known for having idiosyncratic features, such as limited liability related with debt contracts, the nature of asymmetric information between lenders and borrowers, and the nature of the investment technology, which makes it difficult to evaluate the impacts of increased banking competition. Fahrer & Rohling (1992) analyse the asset composition of banks to investigate the degree of competition within the home lending market. The authors construct a Herfindahl index of concentration in the market. However, I perceive that such analysis is restrictive as banks also compete in ways that have not been modeled in Fahrer & Rohling’s study, for example price and product competition. Therefore, to provide a more complete analysis price and product competition should also be accounted for. In support of this view, Jüttner & Grischer (2001) examine the effect of competition on the profitability of banks spanning over a number of OECD countries. Their aim is to convey an understanding of the market structure and global competition. They identify competition to exert its influence upon banks typically on input and output prices (interest rates), on their cost structure, product mix, technological progress and profit margins.

Koskela & Stenbacka (2000) deduce that more intense competition in the lending market will lead to decreasing interest rates and less risky investment projects with a lower rate of return conditional on success, as long as the credit market does not face too many adverse selection problems. I agree that an increase in lending market competition tends toward a reduction in interest rates. However, I perceive that an increase in competition will also lead to more risky lending activities. This view is supported by Gehrig (1998) who argues that increased competition may make adverse selection problems more severe when customers that have been rejected at one bank can apply for loans at other banking institutions. Consequently, the pool of loans will exhibit lower average quality as the number of banks increase and the limited amount of high quality loans available within the market cannot justify the risks associated with financing the remaining loans. If a customer is rejected from one bank, they can apply for a loan at another bank. Hence, a customer can shop for the lowest financing option thereby exerting price pressure on banks.

Melink & Shy (2005) observe the impact of competition within the United States lending market on borrowers and social welfare. The authors use a model where banks choose how much to lend given the quality of the loans. They further model the nature of competition between two competing banks and find that there is a quality-cost trade-off and a resulting impact on market share. Gizycki (2001) states that increased changes in the level of competition within the banking industry may also generate system wide movements in riskiness and performance. For instance, a more competitive environment may prompt individual banking institutions to seek and capture greater market share. Thus, more generally, increased competition may erode profits, making bank profits more sensitive to the underlying riskiness of their loan portfolios.

Twenty years ago borrowers faced strict limits on the size of home loans and a long-standing relationship with the lending institution was a pre-requisite be considered for a loan. Presently, consumers are able to discharge their loan with one bank and place it with another, there is a large array of credit facilities available, for instance mortgage off-set accounts and re-draw facilities, facilities which were not contemplated previously making competition more aggressive. Today, consumers have a large range of institutions competing for their business, offering packages that suit individual needs, with more than 450 lenders presently compete for consumer’s mortgage business (ABA. 2004: 3).

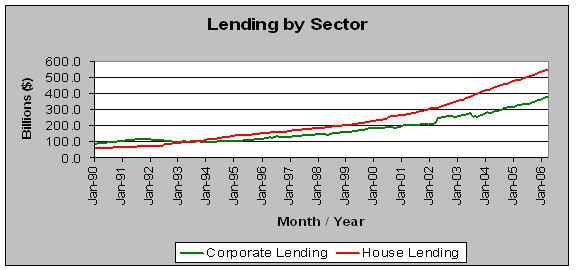

Over the past five years the intensity of competition at a domestic level has led to easier access to credit. This is reflected by the lowering of home credit risk assessment standards, a reduction in lending margins, which have been a clear indicator of increased competition within the market. The increased competition in home lending can be illustrated by the relatively steep rise in home lending volumes since the year 2000 displayed in the graph below (graph 1). Whilst home lending volumes have consistently remained above corporate lending volumes for more than a decade the gap between the two sectors have recently widened. Thus, indicating that financial institutions have exposed themselves to risks associated within the housing sector, as a result of more concentrated lending practices, leading to greater exposure to housing markets where prices have departed from intrinsic values.

(RBA Statistics: D05 - BANK LENDING CLASSIFIED BY SECTOR; www.rba.gov.au).

Innovation in product design has created new challenges for regulators, as Non-Bank Financial Institutions (NBFIs) offer lending products which have the competitive advantage of not being subject to the same stringent regulation as banks. Moreover, non-financial service companies, such as retailers, airlines and telecommunications companies, are entering the market and offering financial services to consumers. These changes have led to products and distribution channels expanding beyond the traditional categories of banking, placing pressure on regulators to ensure competitive neutrality in the treatment of like products offered by different institutions.

While theory encourages competition within markets, in the case of the financial services lending market this may only be desirable if the regulatory settings are sound and appropriate. This means:

▪ Ensuring an industry level playing field;

▪ Ensuring unregulated lenders, such as mortgage originators and non-financial service companies, do not get advantages over banks because they are not regulated by APRA;

▪ Ensuring government regulations do not impose significant and in some cases, unnecessary, costs on banks and other financial institutions (Hall, E. 2000: 1).

The increased competition within the lending market has necessitated the development of credit risk analysis tools that are quick, accurate and cost-effective. Most consumers expect fast loan decisions from financial institutions. As a result, financial institutions have had to change their credit assessment policies to meet changing consumer needs, whereby loyalty is less and less evident. Larger loan amounts are being granted in comparison to borrower income, which involves an increase in the financial institution’s risk appetite. Further, banks fail to independently verify consumer data and increasingly rely on broker-originated loans and the more streamlined techniques used for property valuations (APRA. 2006: 8-9). Financial institutions have also increased debt-servicing ratios, abandoning conservative rules of thumb when assessing a borrower’s capacity to repay debt. The traditional “30 per cent rule”, implies that lenders would limit repayments to no more than 30 per cent of a borrower’s gross income. Now all income above the cost of living estimate is considered to be available for debt servicing, thus, increasing debt-servicing ratios (Laker, J. 2004: 6-7). While these changes may not create problems during times of strong economic conditions, it would exacerbate loan losses if economic conditions deteriorate.

The choice of available products and services is also increasingly expanding. The lending market has truly become a consumers market, with over 18,000 products currently available to consumers (Cannex. 2006), the most common products include;

▪ Credit Cards

▪ Home Loans

▪ Reverse Mortgages

▪ Personal Loans

▪ Car Loans

▪ Margin Loans

▪ Corporate Loans

▪ Low Doc Home Loans

The current concern regarding “low doc” loans and other non-conventional loans are related to the fact that loans are being granted to borrower’s who self-certify their income and are inherently more risky than standard housing loans. Yet, financial institutions are not accounting for this risk appropriately when pricing such loans, as interest rates are comparable to those of standard loans exemplified in Figure 1.

|

Banks

|

Std Var. Loan

|

5 Year Fixed Loan

|

Low Doc Loan

Std Var.

|

Low Doc Loan

5 Year Fixed

|

|

Adelaide Bank

|

7.82%

|

7.50%

|

7.82% +

|

N/A

|

|

Aust. & N.Z. Bank

|

7.82%

|

7.45%

|

7.32% +

|

7.45% +

|

|

BankWest

|

7.82%

|

7.25%

|

7.74% +

|

N/A

|

|

Commonwealth Bank

|

7.82%

|

7.49%

|

7.82% +

|

7.49% +

|

|

Macquarie Bank

|

7.14%

|

7.60%

|

7.48% +

|

8.40% +

|

|

National Aust. Bank

|

7.82%

|

7.39%

|

7.82% +

|

7.39% +

|

|

St George Bank

|

7.82%

|

7.49%

|

7.82% +

|

7.49% +

|

|

Westpac

|

7.82%

|

7.49%

|

7.82% +

|

7.49% +

|

(Cannex. 2006; www.cannex.com.au).

The recent developments and the continual progress within the financial services lending market have led to increased competition within the sector. The challenge for banks and their supervisors is ensuring that the increased competitiveness within the sector does not translate into periods of repeated credit problems of the late 1980s and early 1990s, where

“…crazy loans were made to corporate cowboys” (Sykes, T. 1998: 1) and the aftermath of corporate collapses left banking institutions counting their losses, amounting to tens of billions of dollars, in our case it will be the housing sector.

Credit risk is a prominent issue that financial institutions must confront on a daily basis. A bank’s fundamental purpose is to supply finance, and a significant portion of credit risk faced by financial institutions is associated with lending activities. Credit risk can distort a bank’s balance sheet, leading to costly write-offs and a reduction in capital. Thus, the ability to preserve assets is imperative to a bank’s performance.

Credit risk is commonly referred to as

“the risk that promised cash flows on a bank’s assets, such as loans and securities, are not paid on time and/or in full” (Saunders & Cornett: 2006: 162).

While the measurement and management of credit risk is only one aspect of a banks overall risk management function, its capacity to impact a bank’s balance sheet, makes it critically important to ‘get it right’ (Ullmer, M. 1997: 20). With good management and measurement of credit risk, banks are able to significantly enhance year-on-year performance. The widely accepted convention within finance theory is that management prefers the highest returns for a given level of risk and the lowest risk for a given higher level of returns. Consequently, the degree of the total risk taken to increase returns and the type of risk taken are important considerations for management when making decisions about lending strategies. However, the intensified competition for quality assets has raised concern about the lending market’s response to the slowdown in household credit growth. APRA has cautioned that banks should be amending their business strategies and risk appetite to this new reality and should not pursue growth targets that require more risk, without robust risk management systems and appropriate pricing (Laker, J. F. 2005: 2).

Should a borrower default, both the principal loaned and the interest payments expected to be received are at risk. Barnhill et al. (2001) arrive at the conclusion that credit quality is a critical risk factor of a bank’s portfolio, thus, banking institutions with high credit risk and concentrated portfolios are anticipated to have a higher risk of failure during periods of financial stress. Alternatively, banks with lower risk and broadly diversified loan portfolios are less likely to fail even during periods of volatility. Through diversification borrower specific credit risk is reduced, as the risk of borrower defaults associated with specific segments of the lending market are reduced. On the other hand, financial institutions are still exposed to systematic credit risk, which is the risk of default associated with general economy-wide or macro-conditions affecting all borrowers (Saunders, A. & Cornett, M. M. 2006: 144).

Interest rate differentials determine the variation between the official cash rate and the standard variable rate, and thus, provide an indication of the competition pricing pressures. They essentially represent the difference between the amount banks pay to depositors and the amount banks receive from borrowers; i.e. what banks earn on loans.

Interest Rate Differential = Standard variable rate - Official cash rate (1)

Another commonly employed measure for competition is the percentage of new entrants in the lending market each year, which depicts the entry of new institutions and the exit of unprofitable institutions (normal market mechanisms).

(2)

(2)

The proxy for credit risk is loan loss provisions over total assets, encapsulating the degree of credit risk banks are taking. While a summary measure, finance theory suggests the ratio is of loan loss provisions to total assets is a good proxy for credit risk;

(3)

(3)

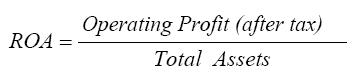

Practitioners are often skeptical of an institution’s market price as an indicator of performance. Thus, stock prices of banking institutions are not being employed as a representative measure for performance, as it cannot precisely measure how operating decisions affect market prices. The reason is that the impact that a change in one division of the business’s strategy would have on the market price is unknown. Thus, it is uncertain whether an increase in market price truly reflects improving company performance or investor sentiment. Therefore, Return on Assets (ROA) is used to measure performance to ensure that revenue from lending activities are evaluated.

Equation 5: Return on Assets (ROA)

(4)

(4)

My empirical analysis is based on the Australian lending market and Australian banking institutions from 1987 to 2005. A panel data set is used where cross-section units are observed upon more than one occasion to explain the relationships between competition and bank credit risk, and competition and bank performance. As a result, institution specific characteristics are present and estimation is conducted by means of a random effects estimation model.

After performing tests for specification, heteroskedasticity and serial correlation, the Feasible Generalised Least Squares (FGLS) model is employed. The FGLS estimator uses an estimate of the error process avoiding the restrictive assumption of a known error process and is appropriate for models where errors show panel heteroskedasticity, contemporaneous correlation and unit specific serial correlation. Consequently, it provides better estimates for models where random effects are the most suitable specification and can handle a wide range of unequally spaced panel data patterns, which is the case in this research paper.

Credit Riskit = μ + Interest Rate Spreadit β + Change in no. of ADIsit β + (αi + εit ) (5)

ROAit = μ + Interest Rate Spreadit β + Change in no. of ADIsit β + (αi + εit ) (6)

The analysis conveyed interesting results[1]. The nature of the relationship between the percentage change in the number of ADIs in the lending market and credit risk presented an expected result, where a positive relation is observed. Thus, an increase in competition tends toward a rise in credit risk. In contrast, the nature of the relationship between interest rate spreads and credit risk is unexpected. As an increase in interest rate spreads, which represents a fall in price competition, leads to a rise in credit risk. Thus, indicating a negative relation. A plausible explanation for this result is that as the interest rate spread rises, the standard variable interest rate rises. Consequently, borrowers are faced with higher borrowing costs as their loan repayments increase and this can cause an increased number of defaults, simply based on a borrower’s inability to meet increased costs. Therefore, in general the results conform to the hypotheses tested that credit risk and competition measures are positively related.

In contrast, the nature of the relationship between the interest rate spread does not have an effect on ROA. Yet, an increase in the percentage change in the number of ADIs in the lending market leads to a reduced ROA, which contradicts the results presented by Jüttner & Grischer (2001) who suggest that increased competition has a positive influence on profits. Hence, the results indicate that competition is inclined to lead to a fall in a bank’s ROA, this is justified by the argument that banks are relaxing credit standards and granting loans to a broader range and riskier borrowers, in order to maintain market share. Competition via interest rate spreads are insignificant, which further supports my view that ADIs are not competing forcefully through price, rather they are using other methods to compete. In the Australian lending market it appears that product features and relaxed lending standards are the current trends, with a number of government bodies, namely APRA expressing their concern with such practices.

The cost of competition to the banking industry can be significant, as banks may lose interest revenue, leading to increased pressure to write as many loans as possible to make up for these losses, as a result, credit quality may suffer in the long-run. While in the short-term banks are able to increase their credit growth by lending to riskier borrowers and adding to their total assets without immediately increasing impaired assets, such activities may even reduce the impaired asset ratio. However, over the long-term, the impacts of riskier borrowers are realised and it is expected that the rapid credit growth by increasing lending to riskier borrowers, will lead to an increase in banks impaired assets ratio. For example, the rapid credit growth of the late 1980s in Australia was felt in preceding years, where Australian banks experienced loan loss problems between 1990 and 1992.

The cost of competition to financial services lending is significant. Australian banks’ interest revenue has fallen, which is supported by the reduced interest rate margins and the lower interest rates in order for banks to remain competitive. As a consequence, competition via interest rates could lead to an increased pressure to write as many loans as possible to make up for the reduction in interest revenue and credit quality may suffer.

The competitive pressure from lending institutions who lower credit standards and provide non-conforming loans make it difficult for more conservative lending institutions to follow a different path, particularly when lending institutions who take on more risk may well be rewarded by higher profits and higher share prices in the short-run. The steady lowering of credit standards could essentially lead to a trend of increased credit risk, which could initiate a financial system crisis. Hence, there is a need to maintain prudent banking practices even during the “good times”. Strong economic activity generally allows financial institutions to prosper and build up their financial strength. On the other hand, continued prosperity can mask weaknesses in a financial institution’s lending strategies and can lead to an increased risk appetite. Thus, Australia’s continuing economic success should not numb an institution’s risk management strategies.

Banks face an extraordinary competitive market in the provision of credit from non-traditional lending institutions such as credit unions, building societies and mortgage lenders. However, it should be acknowledged that not only has the lending market changed on a competitive front, it is also evolving into a new regulatory landscape, with the upcoming introduction of the Basel II capital framework in 2008. The challenge for banks and their supervisors is ensuring that the increased competitiveness within the sector does not translate into periods of credit problems.

ABA. (2004). Housing Lending Standards. Media Release, Sydney, 17 November. http://www.bankers.asn.au/default.aspx?ArticleID=722

APRA. (2006). Overview of the Australian deposit-taking sector. The quarterly bulletin of the Australian Prudential Regulation Authority, APRA Insight Issue 1. http://www.apra.gov.au/Insight/loader.cfm?url=/commonspot/security/getfile.cfm&PageID=11731

Barnhill, T.M; Papapanagiotou, P; Schumacher, L. (2001). An Application to a Set of Hypothetical Banks Operating in South Africa. Milken Institute Award for Distinguished Economic Research, March. http://www.milkeninstitute.org/pdf/barnhill.pdf

Cannex Database. 2006. www.cannex.com.au

Fahrer, J. & Rohling, T. (1992). Some Tests of Competition in the Australian Housing Loan Market. RBA, Economic Research Department, Research Discussion Paper 9202, February. http://www.cs.odu.edu/~dlibug/ups/rdf/remo/rba/rbardp/rdp9202.pdf

Gehrig, T. 1998, Screening, Cross-border Banking and the allocation of Credit. Research in Economics, vol. 52, iss. 4, pp. 387-407. Retrieved August 20, 2006, from Elsevier Science.

Gizycki (2001). The effect of Macroeconomic Conditions on Banks’ Risk and Profitability. RBA: System Stability Department. Paper No. 2001/06. http://www.rba.gov.au/PublicationsAndResearch/RDP/RDP2001-06.html

Hall, E. 2000. Four pillars leave banking shaky. Broadcast at 6:10pm on ABC Local Radio. 13 March. http://www.abc.net.au/pm/indexes/2000/pm_ archive_2000_Monday13March2000.htm

Jüttner, D.J. & Grischer, H. (2001). Profitability and Competition in Banking Markets: An Aggregative Cross Country Approach. 15 June. http://www.econ.mq.edu.au/staff/djjuttner/BankProfit1.pdf

Koskela, E. & Stenbacka, R. (2000). Agency Cost of Debt and Lending Market Competition: A Re-Examination. Bank of Finland, Discussion Paper No. 12/2000. 10 February. www.bof.fi/eng/6_julkaisut/6.1_SPn_julkaisut/6.1.5_keskustelualoitteita/0012 ek.pdf

Laker, J. (2005). Emerging Issues in the Prudential Landscape. APRA: Australian Association of Permanent Building Societies Directors’ Forum, Queensland, 12 May. www.apra.gov.au/Speeches/loader.cfm?url=/commonspot/security/getfile.cfm&PageID=8685

Laker, J. 2004, The Australian Banking System - Building on Strength. Proceedings from the Business Banking Conference. Sydney, APRA. Retrieved June 19, 2006, from www.apra.gov.au/Speeches/loader.cfm?url=/commonspot/security/get

life.cfm&PageID=7904

Macfarlane, I. (2004). Monetary Policy & Fiscal Stability. RBA, Talk to CEDA Annual Dinner, Melbourne, 16 November.http://www.rba.gov.au/Speeches/2004/sp_ gov_161104.html

Melnik, A. & Shy, O. (2005). Credit Quality, Regulation and Competition in the Loan Market. 3 March. http://econ.haifa.ac.il/~ozshy/papers/loan26.pdf

Moullakis, J. (2006). Risk appetite grows in race for loans. Australian Financial Review, Business. 11 February. http://global.factiva.com/aa/default

Saunders, A. & Cornet, M. M. (2006). Financial Institutions Management: A Risk Management Approach, 5th edition, McGraw-Hill, New York.

Sykes, T. (1998). Australia’s Banking History. The Australian Financial Review. The Australian Broadcasting Corporation. http://www.abc.net.au/money/currency /features/ feat3.htm

Ullmer, M. 1997. Credit risk in banking. Bank Supervision Department Reserve Bank of Australia, Alken Press Pty Ltd.

Analysis of Variance

|

Source

|

SS

|

df

|

MS

|

|

Model

|

14.9723587

|

18

|

0.831797708

|

|

Residual

|

36.7864042

|

139

|

0.2645039

|

|

Total

|

51.758763

|

157

|

0.329673649

|

Number of Obs. = 158

F (18, 139) = 3.14

Prob > F = 0.0001

R-Squared = 0.2893

Adj. R-Squared = 0.1972

Root MSE = 0.514442

FGLS Estimation Results for Credit Risk

|

Credit risk

|

Coefficient

|

Standard Error

|

Z Statistic

|

P >

|

|

Interest rate spread |

0.1294992 |

0.0240725 |

5.38 |

0.000 |

|

% change in no. of ADIs |

0.0227433 |

0.0069636 |

3.27 |

0.001 |

|

Constant |

0.3121332 |

0.0711121 |

4.39 |

0.000 |

Analysis of Variance

|

Source

|

SS

|

df

|

MS

|

|

Model

|

3.62593901

|

18

|

0.201441056

|

|

Residual

|

31.9960854

|

158

|

0.20250687

|

|

Total

|

35.6220244

|

176

|

0.202397866

|

Number of Obs. = 177

F (18, 139) = 0.99

Prob > F = 0.4686

R-Squared = 0.1018

Adj. R-Squared = -0.0005

Root MSE = 0.450008

FGLS Estimation Results for ROA

|

ROA

|

Coefficient

|

Standard Error

|

Z Statistic

|

P >

|

|

Interest rate spread |

-0.010935 |

0.0167468 |

-0.65 |

0.515 |

|

% change in no. of ADIs |

-0.0214881 |

0.0060087 |

-3.58 |

0.000 |

|

Constant |

0.7916821 |

0.0524379 |

15.10 |

0.000 |

[1] For further details refer to the Appendix.

AustLII:

Copyright Policy

|

Disclaimers

|

Privacy Policy

|

Feedback

URL: http://www.austlii.edu.au/au/journals/JlLawFinMgmt/2007/9.html