eJournal of Tax Research

|

|

Home

| Databases

| WorldLII

| Search

| Feedback

eJournal of Tax Research |

|

David G. Dunbar[*]

In 2003 the Australian and NZ governments enacted legislation to permit trans-Tasman companies to allocate to their shareholders franking credits and imputation credits. This legislation is known as the pro rata allocation method, and was heralded as a major improvement in trans-Tasman taxation. This paper critically evaluates the claims which have been made by the Australian and NZ governments about the reduction in personal income tax which the pro rata allocation solution will deliver to individual share holders in a typical trans-Tasman company. The paper concludes that the benefits have been significantly over stated and that a more effective legislative solution would have been the streaming model. Accordingly the pro rata allocation solution is unlikely to discourage trans-Tasman companies from engaging in profit repatriation strategies to overcome the inherent tax inefficiency associated with the pro rata allocation solution.

On 19 February 2003 the Australian Treasurer and the New Zealand Minister of Finance announced a solution to a longstanding taxation problem known as triangular taxation:[1]

To resolve this problem, Australia and New Zealand will extend their imputation systems to include companies resident in the other country. Under this reform, Australian and New Zealand shareholders of trans-Tasman companies that choose to take up these reforms will be allocated imputation credits, representing New Zealand tax paid, and franking credits, representing Australian tax paid, in proportion to their ownership of the company. However, each country’s credits will be able to be claimed only by its residents.

The problem referred to in the quotation is known as the so-called triangular tax issue. In November 2003 legislation was passed by the New Zealand Parliament to give effect to the February 2003 announcement. The relevant provisions are contained in a number of different sections in the Income Tax Act 2004 (ITA 04)[2]. The corresponding provisions in the Australian Act (the ITAA97) are contained in Div 220.

As a result of the amendment Australian companies can now pay dividends with NZ imputation credits attached. This legislative solution is often referred to as the pro rata allocation (PRA) model.

The new rules allow Australian and NZ companies to elect into a regime, which allocates to their Australian and NZ shareholders franking and imputation credits in proportion to their ownership in the parent company. However the Australian franking credits can only be utilised by Australian shareholders and NZ resident shareholders can only use the imputation credits.

The November 2003 legislation reflects the analysis and assumptions contained in the March 2002 Discussion Document. [3]

Prior to November 2003 the trans-Tasman taxation treatment of a triangular investment by a New Zealand shareholder resulted in an effective tax rate of 57.3%. The Discussion Document claimed that the PRA solution would reduce the effective tax rate to 43.6%. If that claim is true, the effective tax rate would have been reduced by 24%. This article examines:

A triangular investment occurs when a shareholder resident in Australia or New Zealand invests in a company resident in the other jurisdiction that earns income and pays tax in the shareholder’s home jurisdiction. Prior to November 2003 whenever a shareholder received a dividend, they were unable to obtain a credit for tax that had already been paid in their home country. This meant that triangular income was being taxed twice, i.e. in the country in which it was earned and again in the hands of the shareholder. This was a major disincentive to trans-Tasman investment, which has led to the development of structures to overcome the problem of double taxation.

The following table demonstrates the taxation of a pre PRA trans-Tasman investment held by individual portfolio shareholders in publicly listed trans-Tasman companies. Columns (a) and (c) summarise the tax payable by an individual shareholder who invested in a public company that is a tax resident in the same country as the shareholder. In both cases the individual shareholder is taxed at the top marginal rate. The cash dividend is grossed up for the imputation/franking credit, which reduces the tax payable, by the shareholder.

Columns (b) and (d) illustrate the additional tax cost associated with an investment in a company that is a tax resident in the other jurisdiction. For the purposes of column (b) there is no Australian NRWT because the dividend is fully franked. In the case of column (d) the New Zealand Company receives a foreign shareholder tax credit (FITC) of $12, which reduces the company tax from $33 to $21. The New Zealand Company passes on the credit to its non-resident Australian individual shareholder that is used to pay New Zealand NRWT of $12. Finally the Australian individual shareholder claims a foreign tax credit of $12.

Table One: Summary of Previous Rules

|

|

A

|

B

|

C

|

D

|

|

Parent Company

|

NZ Co

NZ Individual Shareholder

$

|

Australian Co

NZ Individual Shareholder

$

|

Australian Co

Australian Individual Shareholder

$

|

NZ Co

Australian Individual Shareholder

$

|

|

Profit

|

100

|

100

|

100

|

100

|

|

Tax payable

|

(33)

|

(30)

|

(30)

|

(21)

|

|

Imputation / Franking credit

|

33

|

30

|

30

|

21

|

|

Withholding tax 15%

|

-

|

-

|

-

|

12

|

|

Cash dividend

|

67

|

70

|

70

|

67

|

|

Individual shareholder

|

|

|

|

|

|

Cash dividend

|

67

|

70

|

70

|

67

|

|

Gross up

|

33

|

-

|

30

|

12

|

|

Taxable income

|

100

|

70

|

100

|

79

|

|

Gross tax payable[4]

(39-48.5%)

|

(39)

(27)

|

(27)

(216)

|

(48.5)

(32)

|

(38)

(34)

|

|

Less NRWT credit

|

-

|

-

|

-

|

12

|

|

Less imputation franking credit

|

33

|

-

|

30

|

-

|

|

Net tax payable

|

(6)

|

(27)

|

(18.5)

|

(26)

|

|

After tax cash

|

61

|

43

|

51.5

|

41

|

|

Effective tax rate

|

39%

|

57%

|

48.5%

|

59%

|

The implications of Table One are obvious. A New Zealand individual shareholder paid 57% tax on Australian sourced dividends compared with 33% on a New Zealand dividend. The Australian individual shareholders paid 59% tax on New Zealand sourced dividends and 48.5% tax on Australian sourced dividends.

There are a number of important key points that are highlighted in this table which provide an insight into the legislative solution. The available franking credits and imputation credits are allocated according to the respective shareholding in each country. Secondly an individual shareholder can only utilise the imputation or franking credit applicable in the shareholder’s country of residence. The net effect of these two points is that there is an inevitable element of wastage which is measurable by ascertaining the percentage of individual shareholders who are resident in the other country.

The high rates of tax were comparable to the tax which was payable under the old classical system of taxing dividends that existed in both countries prior to introduction of full dividend imputation.

The bias against trans-Tasman equity does not exist in the case of a comparable debt financed investment. This is illustrated in Table Two.

Table Two: Summary of Current Rules

|

|

A

|

B

|

C

|

D

|

|

Parent Company

|

NZ Parent Co

NZ Bond Holder

|

Australian Parent Co

NZ Bond Holder

|

Australian Parent Co

Australian Bond Holder

|

NZ Parent Co

Australian Bond Holder

|

|

Profit before interest

|

100

|

100

|

100

|

100

|

|

Interest expense

|

(100)

|

(100)

|

(100)

|

(100)

|

|

Tax payable

|

Nil

|

Nil

|

Nil

|

Nil

|

|

NRWT 10%

|

-

|

10

|

-

|

10

|

|

Bond holder

|

|

|

|

|

|

Net interest

|

100

|

90

|

100

|

90

|

|

NRWT Gross up

|

-

|

10

|

-

|

10

|

|

Taxable income

|

100

|

100

|

100

|

100

|

|

Gross tax payable

|

(39)

|

(39)

|

(48.50)

|

(48.50)

|

|

Less NRWT credit

|

-

|

10

|

-

|

10

|

|

Net tax payable

|

(39)

|

(29)

|

(48.50)

|

(38.50)

|

|

After tax cash

|

61

|

61

|

51.50

|

51.50

|

In each of the four cases the borrowing company has reduced its taxable income to zero, so there is no company tax payable. Non-resident withholding tax (NRWT) of 10% is deducted from the gross interest in columns (b) and (d). In all four cases the tax paid equates to the bondholder’s marginal rate of tax. The enactment of the PRA solution has no impact on debt securities. The tax paid by an individual bondholder is the same for a domestic and a trans-Tasman debt instrument.

Table 1 assumes that individual shareholders own the parent company resident in the other jurisdiction. Secondly, there is only one operating subsidiary, which is taxed in the other jurisdiction. A more realistic scenario is illustrated in Diagram one, which formed the basis of the analysis, contained in the Discussion Document.[5]

Diagram One: A typical trans-Tasman corporate ownership structure:

The common theme which underlines Diagram one is the unique nature of trans-Tasman investment. Shareholders on both sides of the Tasman own a parent company. Secondly, the parent company owns an operating subsidiary on the other side of the Tasman. Thirdly, the operating subsidiary is paying full local corporate tax. Fourthly, the dividend paid by the subsidiary to its parent company is usually not effectively subject to non-resident withholding tax (NRWT). Finally, the dividend derived by both groups of shareholders does not contain a tax credit for the corporate tax paid by the operating subsidiary. Prior to the adoption of the PRA solution it was one of the ironies of the closer economic relations (CER) agreement that any “local” parent company that wished to become an Australasian player would reward its shareholders with a punitive tax bill, which was totally inconsistent with CER.

The seriousness of the pre PRA problem is illustrated by the case of a hypothetical New Zealand brewer who expands into Australia. Let us assume that Lager Limited is a company paying New Zealand Company tax at 33% and that it pays a fully imputed dividend to, inter alia, its individual New Zealand shareholders. Assume that Lager Limited is also producing beer for export into a highly competitive global market. The company identifies an opportunity in the Australian market. It merges with an established Australian beer manufacturer to exploit that opportunity. To fund the merger a new parent company (Super Lager) is formed which is listed on the Australian and New Zealand stock exchanges. As is so often the case, the parent company is based in Australia and the original New Zealand shareholders now hold shares in Super Lager. Despite the fact that the merger was fundamental to the long-term viability of both the pre-merger companies and despite the clear benefits to the respective national economies, the New Zealand shareholders were rewarded with an increased tax liability from 39% to 59%. This occurred despite the fact that the same amount of New Zealand company tax was still paid and the New Zealand shareholding remained intact. Clearly something was wrong with both countries’ tax systems.

The New Zealand resident shareholders would argue that local New Zealand tax should be able to be attached to dividends paid to resident individual New Zealand shareholders. There was a prima facie case for arguing that such an outcome is consistent with the objectives of New Zealand’s imputation system. It is important to note that the New Zealand shareholders were not asking for any credit to be given to them for the Australian company tax paid by Super Lager. Their case was based solely on the fact that there is local tax paid, there are local shareholders and there is no economically coherent reason for preventing those shareholders receiving an imputation credit for the local company tax.

The Discussion Document states that the PRA solution will reduce an individual New Zealand shareholder's effective tax rate by 24%.[6] This saving is based on the hypothetical group structure illustrated in Diagram One.

The shareholding of the hypothetical Australian parent company that was used in the Discussion Document disclosed that 50% of the parent company share capital is owned by individual Australian shareholders. Individual New Zealand shareholders hold the remaining 50%. That is not a typical trans-Tasman shareholding structure. Empirical evidence suggests that a more realistic shareholding is for the dominant group of trans-Tasman shareholders to own approximately 95% of the parent company share capital with the remaining 5% held by the other group of trans-Tasman shareholders

It would appear that a 50/50 shareholding was chosen because it fitted well with one of the key design features of the PRA solution. The available franking credits and imputation credits will be allocated equally to the two groups of trans-Tasman shareholders. The second unusual feature of the hypothetical example is the underlying income flows and the distribution policy of the parent company.

Diagram two includes: the tax payments, dividend flows, franking credits and imputation credits. For simplicity, the example assumes a 30% corporate tax rate in both Australia and New Zealand, rather than the actual rates of 30% and 33%, respectively. It should be noted that all diagrams are in Australian dollars and no currency adjustment has been applied in this diagram or in any other diagrams, tables, or graphs included in the paper.

Diagram Two: The Discussion Document Example of Tax Payments and Cash Flow

Prior to the adoption of the PRA solution, only the Australian franking credits were attached to the dividend paid by the Australian parent company to trans-Tasman shareholders. However, the New Zealand shareholders were unable to and still cannot utilise the $300 franking credits. Under the PRA solution, the New Zealand shareholders will for the first time be able to access their proportionate share of the imputation credits of $450 which is $225.

The Discussion Document refers to a 24% reduction in the effective tax rate of a New Zealand shareholder who has invested in a trans-Tasman company with the above ownership and income flows. That reduction is calculated in ‘Table Three’.

A significant point to note is that even under this optimal hypothetical company, the effective tax rate is not 39%. This is due to the fact that the dividend is not fully imputed and that follows from the fact that the percentage of profits distributed to the 50% New Zealand shareholders is significantly higher than the 37.5% profit generated from sources within New Zealand. Consequently the dividend is partly generated from Australian source income, which was subject to Australian and not New Zealand income tax. Accordingly the 50% New Zealand shareholders will only receive a partly imputed dividend whenever the percentage of the Australian parent company profit distributed (50%) exceeds the percentage of the parent company's income (37.5%), which is generated from sources within New Zealand.

Table Three: The Discussion Document Example of the Tax Savings

|

NZ Shareholder

|

Before reform $AU

|

Pro rata allocation $AU

|

|

Cash dividend

|

700

|

700

|

|

Imputation credits

|

Nil

|

225

|

|

Franking credit

|

Nil

|

300

|

|

Gross income

|

700

|

925

|

|

Tax due @ 39%

|

273

|

361

|

|

Less imputation credit

|

Nil

|

(225)

|

|

Franking credit

|

Nil

|

Nil

|

|

Tax payable

|

273

|

136

|

|

Net dividend

|

427

|

564

|

|

Effective tax rate

|

57.3%1

|

43.6%2

|

|

1. [273 + 300 (uncredited underlying corporate tax) /

1000]

2. [361 + 75 (uncredited underlying corporate tax) /

1000]

|

||

The professional advisers to trans-Tasman companies and the business community did not share the Minister’s euphoria. For example, the National Business Review reported:[7]

This is certainly not the breakthrough it is being portrayed as, Ernst & Young tax partner Michael Stanley said … only a very small minority of shareholders are going to be affected by this. For a real breakthrough there would have to be full recognition of the tax paid.

The problem, which Michael Stanley was alluding to, is the fact that the PRA method allocates the available imputation and franking credits according to the respective shareholding in each country. Secondly, the shareholder can only utilise the appropriate imputation or franking credit which in the case of an individual Australian shareholder is the franking credit but not the New Zealand sourced imputation credit. It therefore follows that a parent company with a small shareholder presence in the other jurisdiction would find it difficult to justify the compliance and administrative costs of implementing a regime, which only provided a small benefit to a minority group of non-resident shareholders. The only type of Trans-Tasman Company, which would derive a significant benefit from the PRA solution, is the hypothetical company described in the Discussion Document.[8]

The Discussion Document support of the PRA solution is based on a hypothetical trans-Tasman company with, inter alia, a 50% New Zealand and 50% Australian shareholding. However, the following Table demonstrates that the Discussion Document example is not a reliable indicator of a representative company.

Table Four: The Shareholding Composition of Trans-Tasman Companies

Source: Company Annual Reports

|

Company

|

Year Ending

|

New Zealand Shareholding

|

Australian Shareholding

|

|

Australian Gas Light Company

|

2003

|

1.66%

|

97.71%

|

|

AXA

|

2003

|

2.95%

|

97.05%

|

|

Goodman Fielder Wattie

|

2003

|

4.64%

|

94.86%

|

|

National Australia Bank

|

2002

|

0.64%

|

98.58%

|

|

Telstra

|

2002

|

0.50%

|

93.20%

|

|

The Warehouse Group*

|

2003

|

97.02%

|

2.47%

|

|

Tower*

|

2003

|

78.81%

|

20.64%

|

|

Westpac

|

2003

|

3.34%

|

95.15%

|

|

* A New Zealand company

|

|||

The New Zealand shareholding in this sample of Australian parent companies is less than 5%. In the case of Westpac, the approximately 95% Australian shareholders will gain no advantage from the PRA solution, and only approximately 4% of the total tax paid by the New Zealand group will be passed on as an imputation credit to the small minority of New Zealand shareholders. It is perhaps not surprising that as at 1 January 2005, no major trans-Tasman public company has announced that it will implement the PRA solution.

The following diagram illustrates the impact of the PRA solution on an Australian parent company, which is dominated by Australian individual shareholders. The Diagram is based on selected information taken from the Annual Report of Westpac Australia.[9]

The shareholding percentages, income mix and distribution were taken from the 2002 Concise Annual Report and the 2002 Financial Report. However, the combined total pre tax income of both the New Zealand and Australian and operating subsidiaries ($4,000) is based on the example used in the Discussion Document.

Diagram Three: The Pro Rata Allocation Regime

The total income of the two subsidiaries is $4,000. In Diagram Three, the New Zealand Subsidiary Company only contributes 15% (compared to 37.5%) of the income earned by the Australian Parent Company whereas the Australian Subsidiary Company contributes 85% of the income (compared to 62.5% in the example portrayed in the Discussion Document). The following Table illustrates the change in the effective tax rate, which a New Zealand shareholder would expect to derive from a company such as Westpac. The fall in the effective tax rate is from 57.3% to 52.5% (5%), which is only an 8% reduction in the effective tax rate. This is significantly less than the 24% benefit referred to in the Discussion Document. The difference between the respective results reflects the change in shareholding and the change in the underlying sources of income between this Example and the hypothetical example used in the Discussion Document.

Table Five: The Pro-Rata Allocation (Australian Parent)[10]

|

New Zealand shareholder

|

$AU

|

|

Australian shareholder

|

$AU

|

|

Cash dividend

|

84

|

|

Cash Dividend

|

1,596

|

|

Imputation credit

|

9

|

|

Imputation Credit

|

171

|

|

Franking credit

|

36

|

|

Franking credit

|

684

|

|

Taxable income

|

93

|

|

Taxable income

|

2,280

|

|

Tax due @ 39%

|

36

|

|

Tax due @ 48.5%

|

1,106

|

|

Less imputation credit

|

9

|

|

Less imputation credit

|

0

|

|

Less franking credit

|

0

|

|

Less franking credit

|

684

|

|

Tax payable

|

27

|

|

Tax payable

|

422

|

|

Net dividend

|

57

|

|

Net dividend

|

1,174

|

|

Effective tax rate

|

52.50%

|

|

Effective tax rate

|

48.50%

|

|

|

|

|

|

|

|

Pre-tax cash dividend

|

120

|

|

Pre-tax cash dividend

|

2,280

|

|

Company tax

|

36

|

|

Company tax

|

684

|

The Discussion Document acknowledges that, from an individual shareholder’s perspective, the pro rata allocation method does not provide the optimal solution [11] which will only occur if one of the alternative methods such as pro rata allocation is adopted.[12] This conclusion is based on the fact that only a proportion of the tax paid in each country is available to the resident shareholders of that country.

Secondly, the PRA solution will result in additional compliance costs for any company that elects to adopt the proposal. For example, the Australian parent company, described in Diagram three will be required to maintain an additional memorandum account which would track the imputation credits generated in New Zealand and the attachment of those credits to any dividend paid to its trans-Tasman shareholders.

Unless the pro rata allocation model provides significant additional benefits to individual Australian shareholders, the Australian parent company may have difficulty justifying the increased compliance costs. This could become an issue if there are alternative and more cost effective ways of achieving the desired benefits for shareholders.

The pro rata model is not the optimal tax solution. From a company and shareholder perspective, the streaming of tax credits would provide significant additional benefits that are not available under the pro rata allocation method. If this alternative were adopted, then the Australian parent company and its New Zealand subsidiary would attach imputation credits to any dividend distributed to the New Zealand resident shareholders. Those shareholders would not receive a proportion of the available franking credits. Accordingly, the streaming of credits model does not result in any wastage; that is to say, the misallocation of either imputation or franking credits.

There were three other alternatives, which both governments considered but rejected. They were:

Under this theoretical alternative, there are two possible solutions. The first would involve providing imputation/franking credits for the company tax paid in the other jurisdiction. The second method would involve extending the full benefits of, for example, imputation to individual shareholders resident in Australia. This would be done on a reciprocal basis.

In addition, compensation could be paid to the country that recognised the imputation credit from the country that received the company tax, which created the credit.

Under the pro rata revenue sharing solution, the New Zealand government would recognise, as a New Zealand imputation credit, a franking credit that was attached to a dividend derived by a New Zealand individual shareholder, and vice versa. Under this solution the New Zealand government, as the resident country, would bear the cost of recognising the Australian franking credit. Accordingly, compensation could become payable to the country that recognised the imputation credit (New Zealand) from the country that received the tax which generated the franking credit (Australia). If this feature did not form a part of this solution, it would mean that the cost of the franking credit would be borne by the country of residence (New Zealand).

At the end of each income year, there would be a wash-up calculation and payment. The two revenue authorities would calculate the total credits claimed by their respective taxpayers and one country would pay to the other the net balance. For example, if the New Zealand government had recognised $100m in Australian franking credits granted to New Zealand residents, and the Australian government had recognised $50m in New Zealand imputation credits granted to Australian residents, then the Australian government would pay to the New Zealand government $50m.

From the perspective of an individual New Zealand residence shareholder, this method would involve each country recognising the other country’s imputation credits as if they were its own, but in turn receiving compensation from the other government. Both governments rejected this theoretical solution because mutual recognition exceeds what was required to solve triangular taxation. One of the main conceptual concerns was that shareholders in either country would receive imputation credits, regardless of whether tax was paid in their respective home countries. “Neither government is willing, therefore, to pursue mutual recognition further at this stage.”[13]

This theoretical solution is similar to pro rata allocation except that the imputation credits are allocated in proportion to shareholdings of residents in each country and the amount of income earned in each country. Under the pro rata allocation solution, the credits do not reflect the sources of the underlying income of the parent company.

If the hypothetical parent company in Diagram three earned 50% of its income from sources in Australia and 50% of its income from its New Zealand subsidiary, the shareholders would receive 50% of a full Australian imputation credit and 50% of a full New Zealand imputation credit. The solution would be advantageous to the New Zealand individual resident shareholders who currently do not receive any of the New Zealand imputation credits. However, it would create a significant disadvantage to the resident Australian shareholders who currently receive a fully franked dividend from the Australian parent company. Accordingly, this theoretical solution was unlikely to find any support from an Australian parent company with a significant Australian individual shareholding.

Secondly, this method was rejected because it is inconsistent with the current imputation regimes of both countries, which provide that imputation/franking credits must be allocated across all shareholders. Thirdly, the present regimes do not recognise different sources of income that are contained in a dividend distribution.

Under this alternative, all tax paid by the hypothetical Australian parent company would be allocated to the Australian shareholders whereas the tax paid by the New Zealand subsidiary would be allocated solely to the New Zealand shareholders’ in the Australian parent company. From a trans-Tasman shareholders perspective, this is the optimal solution because it does not involve the wastage or misallocation of a proportion of the available imputation and franking credits and is therefore superior to the PRA pro rata solution. It would appear from the Discussion Document that both governments rejected this alternative because they did not wish to signal that the streaming of available credits should become more acceptable.[14] One of the main design features of both countries imputation regimes, which have not altered since their introduction, is the principle that credits must be allocated equally to all shareholders irrespective of their ability to utilise the credit. For example, a shareholder on a marginal rate of 19.5% who receives an imputation credit of $33 is not able to effectively utilise the surplus imputation credit, unless they have alternative sources of unimputed income.

A dividend will always be partially imputed (or franked) if the proportion of income derived in New Zealand (or Australia) is less than the percentage of profits the parent company distributes as a dividend. This finding is intuitive because when the income distribution policy exceeds the ratio of income earned in a particular jurisdiction, part of the dividend consists of income derived from the other country. This “other” income would have paid company tax in the other jurisdiction, which cannot be offset against the personal tax liability of a non-resident shareholder. Conversely, whenever the proportion of income earned in a particular jurisdiction is greater than the portion of income distributed, shareholders resident in that jurisdiction will receive fully imputed dividends.

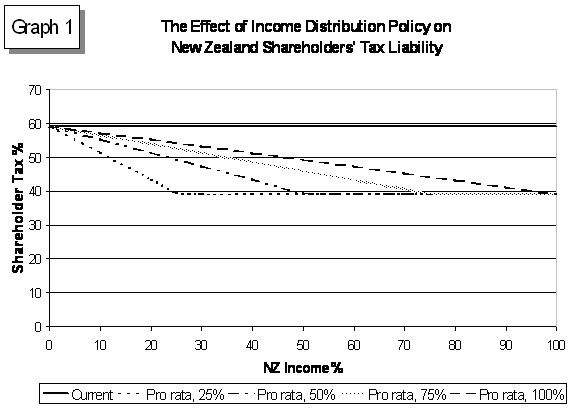

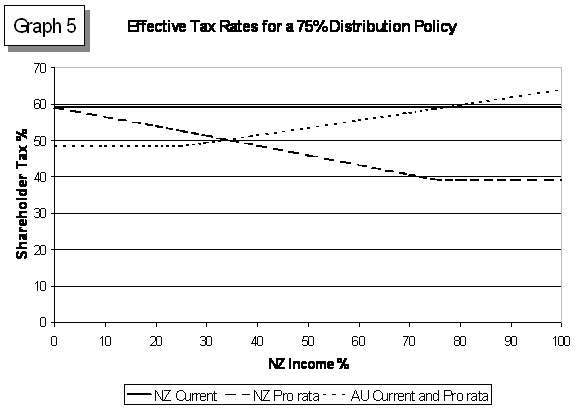

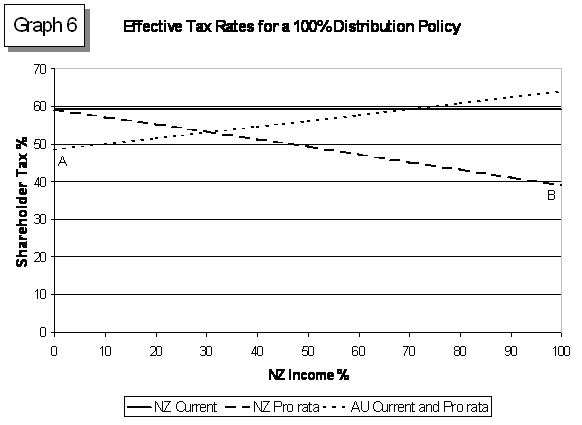

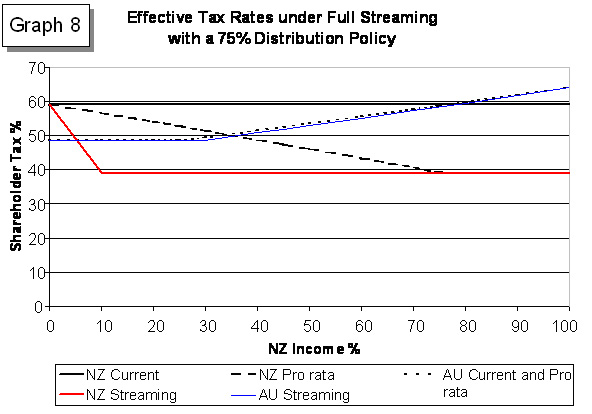

The graphs numbered one to six demonstrate the general principles of pro rata allocation. They show how a shareholders marginal tax rate changes as the distribution policy, and level of income earned in New Zealand are manipulated. For example, the curve representing “Pro rata, 25%” corresponds to the effective tax rates associated with a 25% dividend distribution policy. The graphs are based on an Australian parent company with a trans-Tasman shareholding of 95% Australians and 5% New Zealanders. Note however a change in the shareholding of either group does not alter the shareholder’s effective tax rate under pro rata allocation. The general rule ensures that only a change in the proportion of income earned in each country, or the distribution policy, will lead to a change in the effective marginal tax rate. Accordingly, under the pro rata allocation model it is assumed that shareholding mix was the same throughout the simulation.

Graph One portrays the effective tax rates of a New Zealand shareholder based on different levels of profit distribution. Whenever the proportion of income generated by the New Zealand subsidiary exceeds a particular level of income distribution, the effective tax rate becomes equal to the current marginal tax rate of the New Zealand shareholder (which is currently 39%). Full imputation is represented by the horizontal part of the line. In the case of a 25% distribution policy, a New Zealand shareholder's tax liability becomes 39% whenever the New Zealand subsidiary contributes more than 25% towards the parent company’s total income. Prior to reaching the point of full imputation, an additional tax liability is imposed on the New Zealand shareholder, which is portrayed by the sloped section of the line.

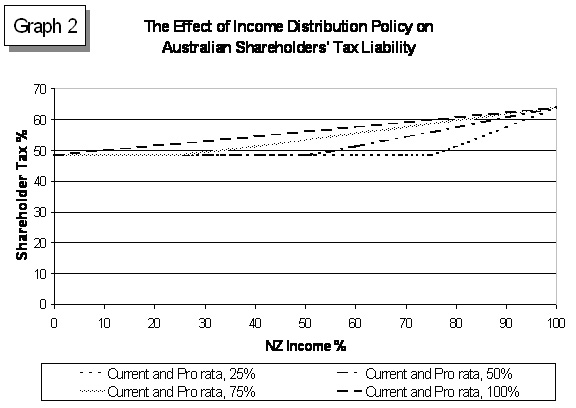

Graph Two is identical to Graph One except that it illustrates the impact of the PRA solution from the perspective of an Australian shareholder. Graph Two provides further evidence of the general theme of pro rata allocation. Australian shareholders will only receive limited tax relief when the proportion of income earned in Australia is less than the distribution policy. Modelling a distribution policy of 25% illustrates how the effective tax rate of an Australian shareholder is higher than their marginal tax rate whenever the level of New Zealand sourced income exceeds 75% of the total income derived by the parent company. This implies that the proportion of income earned in Australia is less than 25%.

Finally Graph Two emphasises that regardless of the distribution policy, the Australian shareholders marginal rates of tax are the same prior to and after the enactment of the PRA solution. The foreign tax credits attached to their dividend cannot be used to reduce their domestic tax liability. Constructing the graphs to reflect a New Zealand company would also demonstrate that a New Zealand shareholder’s tax rates under pro rata allocation reflect those under the current regime.

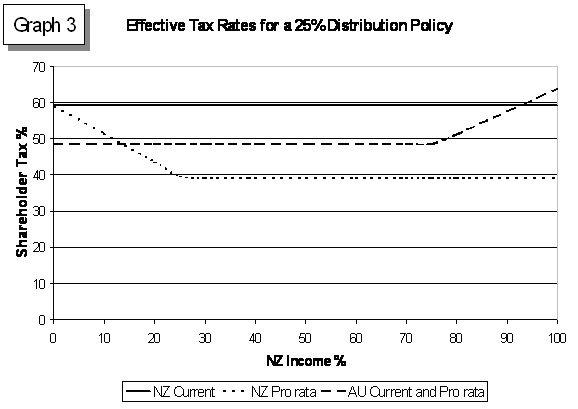

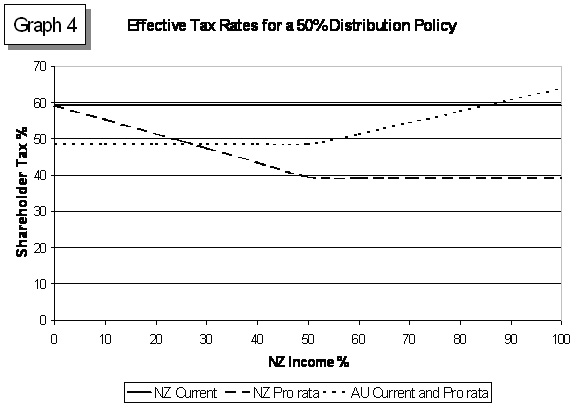

Graphs Three, Four, Five, and Six illustrate the effective tax rates for New Zealand and Australian shareholders of an Australian parent company. The only variable, which has been altered, is the percentage of the available profit, which is distributed. These four graphs will assist trans-Tasman companies to calculate the income and dividend payments, which would be necessary to provide their shareholders with a fully imputed dividend.

Graph Three demonstrates that a 25% distribution policy will provide fully imputed and franked dividends whenever the proportion of New Zealand income is between 25% and 75% of the parents company’s total income. However as the dividend is increased, the shareholders no longer receive a fully imputed dividend.

The only scenario when both groups of shareholders are able to receive fully imputed dividends is shown in Graph Four (which models a distribution policy of 50%). The only point where this occurs is at the 50% level of income distribution. Moving beyond a 50% distribution the four graphs illustrate that both full imputation and franking becomes a mutually exclusive event. It is not possible for both subsidiaries to be earning greater than 50% of total income. The 75% and 100% distribution graphs[15] highlight the mutual exclusivity principle.

The shareholding and income characteristics of the Australian parent company in Diagram Three do not correspond to the major trans-Tasman companies listed in Table Four. It appears to be more common occurrence for a company resident in one jurisdiction to have a minority group of shareholders in the other jurisdiction. Secondly, a significantly lower level of income is typically sourced from the foreign jurisdiction. The empirical evidence would suggest that the New Zealand subsidiary generating 37.5% of the Australian parent's total income is an unrealistic proportion.

The income of the Australian and New Zealand subsidiaries in Diagram Three is based on the Westpac example where 15% of the total group income was sourced from New Zealand. However the New Zealand shareholding was only 5%. Modelling an actual company’s shareholding and income characteristics produces an example that is more indicative of trans-Tasman commercial reality. The figures used in the Discussion Document are unlikely to accurately illustrate the benefits that large publicly owned trans-Tasman company would produce for their shareholders if they were to adopt the PRA solution.

A second unrealistic simplification contained in the main example used throughout the Discussion Document is the 100% distribution of each subsidiaries net income to the parent company. A full distribution of net income would be unusual in practice. Thirdly, subsidiaries that do pay a dividend to their parent company often to do so on an irregular basis.

The tax benefits calculated in this paper, before and after the enactment of the PRA solution, are materially different to the tax savings highlighted in the Discussion Document. This stark contrast can be traced to the respective differences in the income and shareholding characteristics of the parent company.

Unlike the Discussion Document, Table Five depicts a much more realistic tax saving of 4.85% for the New Zealand shareholders. The Discussion Document’s example of PRA creates a unrealistic perception of the PRA regime. The simplistic income mix in Diagram Two was directly responsible for the apparent tax savings which would occur once the proposal became law. This would not have been possible if a more commercially representative example had been used. However, that would have led to a less favourable impression of the benefits of the PRA solution.

The 50% income distribution assumption was another factor that enabled the Discussion Documents main example to produce a fully franked dividend for the Australian shareholders. If a distribution policy higher than 62.5% (the proportion of income sourced in Australia) were adopted, the Australian shareholder would no longer receive a fully imputed dividend. This could be the reason why a 50% distribution of profit was adopted in the Discussion Document because it was less than the ratio of income derived in Australia.

Graph Six (100% distribution policy) emphasises the negative effect that a high distribution policy can have on the marginal tax rates which occur under the PRA solution. At point “A”, Australian shareholders will only receive a fully franked dividend if the New Zealand subsidiary does not earn any income. The same thing occurs for the New Zealand shareholders modelled in Graph Six at point “B”. The New Zealand shareholders will receive a fully imputed dividend whenever the income of the parent company is generated entirely from its New Zealand subsidiary.

The ability to modify the effective tax rate of a trans-Tasman shareholder through the dependent variables of the PRA legislative solution can be used to create a particular outcome. The unrealistic profile of the group of companies, which formed the bases of the analysis in the Discussion Document significantly over stated the level of tax saving which would occur if one of the public companies disclosed in Table Four elected to implement the PRA solution. This is a serious concern because a company may be misled into adopting the PRA solution due to the unrealistic portrayal of the benefits of the PRA legislative solution.

One of the major criticisms of the PRA solution is that it will force an Australian parent company to allocate its available imputation and franking credits to individual shareholders that are unable to utilise them. Under the full streaming, alternative all tax paid by the hypothetical Australian Parent Company would be allocated to the Australian shareholders whereas the tax paid by the New Zealand Subsidiary Company would be allocated solely to the New Zealand shareholders. From a trans-Tasman shareholder’s perspective, this is the optimal solution because it does not involve the wastage or misallocation of a proportion of the available imputation and franking credits and is therefore superior to the pro rata solution. It would appear from the Discussion Document that both governments rejected this alternative because they did not wish to signal that the streaming of available credits should become more acceptable.[16] One of the core design features of both countries imputation regimes, which have not altered since their introduction, is the principle that credits must be allocated equally to all shareholders irrespective of their ability to utilise the credit. For example, a New Zealand shareholder on a marginal rate of 19.5% who receives an imputation credit at the maximum rate of $33 on a $67 cash dividend is not able to effectively utilise the surplus imputation credit, unless he/she has alternative sources of unimputed income.

Diagram Four is based on the profile of the same Australian parent company shown in Diagram Three (which was designed to demonstrate the actual tax saving associated with the PRA solution.) This will enable a valid comparison to be made between the two alternatives. The key difference is that the Australian shareholders no longer receive an imputation credit and the New Zealand shareholders no longer receive a franking credit. A second important difference is that the respective operating subsidiaries franking and imputation accounts now disclose a credit balance. In other words, there are surplus tax credits that are available even after the payment of a fully imputed dividend. There is no longer any wastage of domestic credits that are otherwise allocated to the Australian Parent Company’s non-resident shareholders.

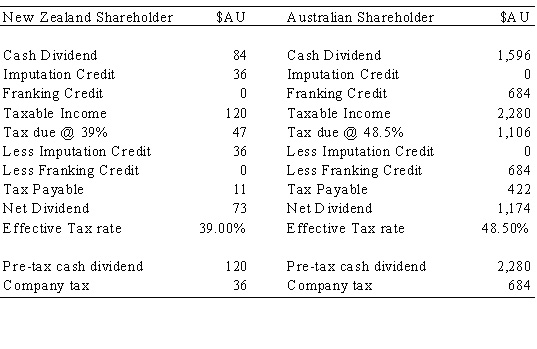

Table Six demonstrates the significant reduction in the effective tax rate associated with the full streaming option. Under this option, there is no improvement in the Australian shareholder’s after tax return. However, the full streaming option enables the New Zealand shareholders to receive a dividend with an effective tax rate that is comparable to an equivalent domestic investment. Double taxation is completely eliminated.

For a New Zealand shareholder Table Six demonstrates that their after-tax position has substantially improved. Full streaming enables the New Zealand shareholders to gain the benefit of the total amount of New Zealand company tax paid by the New Zealand subsidiary,[17] whereas PRA solution links the tax benefit to the shareholder’s ownership in the Australian Parent Company. The profile of the Australian Parent Company summarised in Diagram Four will completely eliminate double taxation, reducing the New Zealand tax rate to 39%. This amounts to a reduction of approximately 32% compared to the approximately 8% reduction associated with the PRA method.

Diagram Four: The Full Streaming Model

Table Six:The Full Streaming Model (Australian Parent)

|

New Zealand shareholder

|

$AU

|

|

Australian shareholder

|

$AU

|

|

Cash dividend

|

84

|

|

Cash Dividend

|

1,596

|

|

Imputation credit

|

36

|

|

Imputation Credit

|

0

|

|

Franking credit

|

0

|

|

Franking credit

|

684

|

|

Taxable income

|

120

|

|

Taxable income

|

2,280

|

|

Tax due @ 39%

|

47

|

|

Tax due @ 48.5%

|

1,106

|

|

Less imputation credit

|

36

|

|

Less imputation credit

|

0

|

|

Less franking credit

|

0

|

|

Less franking credit

|

684

|

|

Tax payable

|

11

|

|

Tax payable

|

422

|

|

Net dividend

|

73

|

|

Net dividend

|

1,174

|

|

Effective tax rate

|

39.00%

|

|

Effective tax rate

|

48.50%

|

|

|

|

|

|

|

|

Pre-tax cash dividend

|

120

|

|

Pre-tax cash dividend

|

2,280

|

|

Company tax

|

36

|

|

Company tax

|

684

|

The Discussion Document summarises[18] the three primary reasons why both governments have rejected the streaming alternative.

The perception that the streaming model provides tax benefits that are disproportionate to the individual shareholder’s interest in the company.

The perception that this alternative contained a fiscal risk because all of the available imputation credits could be used to reduce an individual shareholder’s New Zealand tax liability.

A concern that the adoption of the streaming model could be interpreted as a signal that streaming is now an acceptable strategy.

A careful examination of the history of both the Australian and New Zealand international tax regime and the underlying objectives of the imputation regime strongly suggests that there is very little merit (if any) in the governments’ concerns.

The governments’ concern was

Streaming would see all tax paid in New Zealand available to provide imputation credits solely to New Zealand shareholders. Such a model is contrary to Australia and New Zealand’s imputation rules as it provides tax benefits to shareholders disproportionate to their shareholding.[19]

This is not a substantial reason for rejecting the streaming model. Under the maximum imputation model an Australian Company is restricted by the amount of imputation credit that it can attach to the dividend. Based on the current New Zealand corporate tax rate of 33% imposed upon the New Zealand subsidiary company, the maximum imputation credit is 33/67, of the net dividend paid. It is not possible for the New Zealand shareholders to receive an imputation credit which exceeds the tax paid by the New Zealand operating subsidiary to the New Zealand revenue authority.

The only difference between the pro rata and streaming models is that the parent company has a choice under the streaming model of allocating either a franking or imputation credit to its respective shareholders. The objective of the streaming model is to eliminate the incidence of double taxation on income sourced from the country in which the shareholder is a tax resident. This laudable objective is entirely consistent with the objectives of the New Zealand and Australian imputation regimes, which were introduced to eliminate double taxation. The point that has been overlooked in the Discussion Document is that New Zealand corporate tax is imputed to New Zealand resident shareholders. There is no attempt under the full streaming approach to ensure that an individual New Zealand shareholder obtains a credit for Australian company tax in respect of income, which was not previously taxed in New Zealand.

The fiscal concerns of the governments are difficult to understand. The Discussion Document states that:

“Both governments, … are concerned about the fiscal risks of [the streaming] model, given that imputation credits would be allocated only to shareholders of countries in which the tax was paid. This means that most of the imputation credits allocated could be used to reduce the shareholder’s home country tax liabilities.”[20]

Both governments are incorrect in their understanding of the streaming model because streamed credits will offset a resident shareholder’s domestic tax liability only to the extent that underlying corporate tax was paid in that country. When viewed from this perspective it is difficult to see how the streaming model could ever pose a material threat to the New Zealand tax base. The streaming model merely alleviates the wastage of credits, which occur under the current imputation regime. The streaming model simply rectifies a deficiency in the current law, which is not putting the tax base at risk. Correcting an anomaly in the existing law will ensure that there is consistent treatment between a domestic investment and a triangular investment.

The third and final concern of both governments was that to allow streaming in the context of triangular taxation:

“might also signal that streaming of credits more generally is now acceptable. Both governments wish to avoid such a result, as it is still both countries policy that imputation credits should not be streamed and should be allocated across all shareholders.”[21]

It is clear that the streaming model is not inconsistent with the imputation regime. The report of the original committee, which considered the design parameters of the current imputation regime, noted that from an imputation policy perspective, there were no policy reasons to prevent the streaming of credits in the case of triangular taxation. [22] The committee rejected the streaming option because of their concern that it could undermine the CFC and FIF regimes. The Consultative Committee noted that from an imputation policy perspective there were no theoretical reasons to prevent, for example, National Australia Bank and Bank of New Zealand (NAB/BNZ) from passing imputation credits to its NZ resident individual shareholders. The Consultative Committee’s concern was that:[23]

“The imputation system and the international tax reforms need to be mutually consistent and reinforcing. A non-resident company can avoid the international tax regime by holding its non New Zealand interests through a non-resident subsidiary. This advantage would be counterbalanced in part if such a company were not able to pass imputation credits through to its New Zealand shareholders. For this reason, the Committee does not favour allowing non-resident companies to allocate credits to New Zealand resident shareholders.”

This passage clearly demonstrates the interrelationship between NZ’s international tax regime and the current imputation regime. The designers of both regimes correctly noted the interrelationship and that from a purely imputation perspective, there were no issues arising from the streaming of credits to alleviate triangular taxation.

Of greater concern are the significant changes in corporate ownership that have occurred since 1988. Lion Nathan and Goodman Fielder Wattie are no longer NZ resident companies and therefore the concerns about the impact of the CFC and FIF regime on these taxpayers no longer apply. The current anomaly merely reflects the historical imperative that Australian and New Zealand companies should not be in a position to stream imputation credits arising from New Zealand source income to domestic New Zealand shareholders. If that were to occur it could have provided those companies with an incentive to trap offshore income in a CFC, thereby avoiding the impact of those two regimes (which were also introduced at the time of imputation).[24]

There are a number of significant provisions in New Zealand domestic law that would prevent the inappropriate use of the streaming model thereby alleviating the above concerns:

The current imputation regime has numerous provisions that are designed to prevent streaming. The first is a restriction against attaching imputation credits to dividends that exceed the maximum imputation ratio (i.e. 33/67). This rule ensures that a company cannot attach imputation credits to a dividend that exceeds the company tax paid or payable in respect of funds in which the dividend was sourced Furthermore, the benchmark dividend rule ensures that the same imputation ratio (subject to a ratio change declaration) applies to all distributions.

A continuity of shareholding test. A company cannot carry forward and imputation credit balance where there is a greater than 33% change in shareholding. In other words, a company must maintain at least a 66% continuity of shareholding.

Specific rules that prohibit the trading of shares where a purpose (not being an incidental purpose) of the arrangement is to provide a tax advantage to any shareholder. Those provisions are designed to prevent shareholders from buying and selling shares to facilitate the passing of imputation credits to shareholders who are best able to utilise them.

The Australian legislation contains a number of similar provisions.

Finally there are a number of specific detailed rules which are as follows. The first is ITAA97 Subdiv 204-B dealing with dividend selection schemes; ITAA97 subdiv 204-D where Commissioner may deny an imputation benefit to a favoured member and determine that a franking debit arise for the paying company where franked dividends are streamed so that some members receive greater imputation benefits than others; the general anti avoidance rule relevant to franking credit trading and dividend streaming s177EA (applied in the context of dividend streaming in Electricity Supply Industry Superannuation (Qld) Ltd v FCT (2003) 53 ATR 120); and Division 208 which generally excludes an exempting entity from the normal gross up and tax offset when paying and receiving dividends. Exempting entities are entities 95% or more owned by non residents or tax exempts.

For all of these reasons it is difficult to see why the adoption of the streaming model would give rise to any genuine tax base maintenance issues. The existing rules in both jurisdictions are adequate to prevent the disproportionate allocation of credits.

However before leaving this subject there is a wider issue to briefly consider. The various table’s diagrams and graphs illustrate how sensitive an “optimal solution” is to the inter action of a number of variables which include:

The adoption of an unfettered dividend streaming regime will not necessarily provide a comprehensive solution for ALL Trans-Tasman companies. It would at best only provide an advantage to those companies whose exact corporate profile fitted in with the underlying assumptions contained in any legislative model which is ultimately chosen to replace the PRA “solution”. The comments of the Board of Taxations report to the Treasurer on the Review of Australia's International Taxation Arrangements and the Australian Treasury Discussion Paper (which formed part of the review) were a timely reminder of the general problems created by all imputation systems which often struggle to deal with foreign source income and foreign underlying tax and withholding tax. What may be a politically acceptable to the trans-Tasman problem is not necessarily the optimal solution to the wider problem of triangular taxation and nothing in this article should be taken as support for the adoption of either PRA, or full streaming beyond the narrow confines of the unique nature of Trans-Tasman investment.

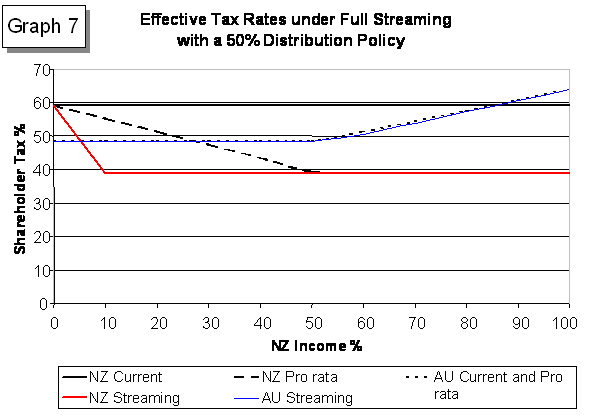

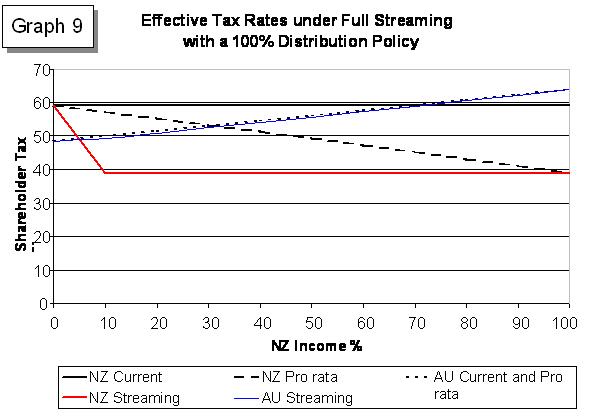

Graphs Seven to Nine highlight the differences between full streaming and PRA by using three, different levels of income distribution. These three graphs have used the same company profile.

The three graphs clearly demonstrate that New Zealand shareholders would receive a greater benefit under full streaming, whenever the proportion of income distributed increases. Full streaming allows all of the New Zealand tax paid to be made available to New Zealand shareholders. In the case of the Australian company shown in the graphs, provided that at least 10% of total income is sourced from New Zealand, the 5% of New Zealand shareholders are entitled to a fully imputed dividend, regardless of the distribution policy. Under PRA however, New Zealand shareholders are comparatively worse off when the proportion of income distributed increases.

The benefits for the Australian shareholders under full streaming are not as substantial, because they were receiving fully franked dividends under both the current and PRA solution. Full streaming does not create any additional tax benefits.

The combined effect of the waste of credits associated with the pro rata allocation solution and its complexity and compliance costs will limit its appeal. The Australian Parent Company in the hypothetical example considered in the Discussion Document has very few (if any) incentives to implement a solution which will only benefit its 50% New Zealand individual resident shareholders. There is no benefit to the Australian individual shareholders and there will be inevitable compliance costs arising from the PRA solution.

The rejection by both governments of the full streaming alternative is likely to see a continuation of ad hoc solutions which achieve the same underlying benefits associated with the full streaming option. Recent examples include:

This is NOT a comprehensive of profit repatriation strategies and I have only examined a selection to highlight the range of options that face trans-Tasman companies who are unable to deliver to their shareholders any meaningful tax benefits from the PRA solution. For example a dual listed company is an obvious option which has not been considered. A classic example of that strategy is the dual listing of BHP Billiton which has enabled franked dividends to be paid to Australian shareholders and unfranked dividends to be paid to United Kingdom shareholders.

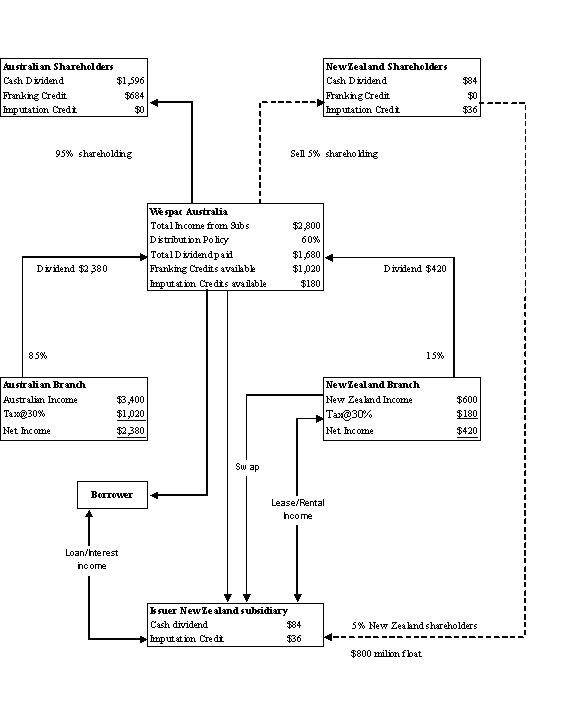

An obvious solution to triangular taxation is for an Australian Parent Company to incorporate a special purpose New Zealand subsidiary that pays a fully imputed dividend to the New Zealand shareholders. This solution would involve the New Zealand shareholders realising their investment in the Australian parent company and subscribing for shares in the ‘new’ New Zealand subsidiary. The most significant example of the strategy is the $A800m successful capital raising which was undertaken by Westpac in late 1999. Following the successful Westpac $A800m float, the ANZ Banking Group announced a similar proposal but it has yet to proceed to making a public offer.

As part of the capital raising exercise, Westpac obtained a binding product ruling from the Inland Revenue Department which stated that the proposal did not contravene the specific anti imputation streaming provisions contained in the Income Tax Act 1994 (ITA94) including the general anti avoidance provisions. The essential features of the proposal are described in BR Prd99/13.[25] The relationship between the parties is summarised in the following diagram, which has incorporated the actual shareholding, disclosed in the 2002 Annual Report. The combined income of the Australian branch and the New Zealand branch of $A4,000 is the same as the income flow used in the Discussion Document.

A key feature of the capital raising exercise is to enable the New Zealand issuer to earn taxable income and thereby generate imputation credits. The New Zealand issuer derived rental income from their ownership of a property portfolio which was leased to Westpac affiliates throughout New Zealand. The issuer also lent the funds raised from the float to another member of the New Zealand group, which generated gross interest income. Finally, a swap was entered into to ensure that the dividend payment to the New Zealand shareholders was based on the dividend paid by the Australian parent company to its Australian shareholders. The tax advantage arising from the structure was the creation of imputation credits for the New Zealand shareholders. The following Table shows the advantage for the New Zealand shareholders from investing in the New Zealand issuer (which is essentially the same as Table Four).

Diagram Five: The Westpac Solution to Triangular Taxation

Table Five: The Westpac Solution to Triangular Taxation

The Westpac solution effectively provides its New Zealand shareholders with all of the advantages of the full streaming option, which has been rejected by both the Australian and New Zealand Governments. Note that with the Westpac solution there is no inefficient allocation of the available tax credits. All of the transaction costs are effectively borne by the New Zealand shareholders who derive all of the taxation advantages.

In view of the high level of wastage associated with the PRA solution, there are very few (if any) taxation reasons why an Australian parent company would wish to fund its New Zealand subsidiary in a manner that created imputation credits. A more efficient solution is for the Australian Parent Company to finance the New Zealand operations in a manner that creates franking credits. A possible response to the rejection of the full streaming alternative is for Australian companies to refinance their New Zealand operations in the following tax effective way.

The following diagram summarises the New Zealand tax implications of a typical trans-Tasman group. The Australasian tax group consists of inter alia a New Zealand Holding Company and New Zealand Operating Company. Finance is provided via the Australian Parent Company subscribing for equity in the New Zealand Holding Company (NZHC). The NZHC lends the proceeds its wholly owned New Zealand Operating Company (NZOC). The NZOC pays interest (which is an allowable deduction) to NZHC (which is gross income). Finally, the NZOC remits the after tax income to the Australian Parent Company in the form of a dividend. The total New Zealand tax ($33) consists of $22.11 company tax and 11.82 NRWT (met via supplementary dividend).

Diagram Six: Current structure

The following more complex diagram is designed to reduce the amount New Zealand tax and create a corresponding increase in the dividend paid to the Australian parent company. Under a conventional funding arrangement, an after tax dividend of $67 is paid to the Australian parent company. Under the following rearrangement, the net after tax New Zealand sourced dividend is increased from $67 to $90.

For the purposes of illustration only the underlying assumption is that the structure will be used to refinance the existing NZ group. The concepts are equally applicable to financing an expansion of the NZ group associated with for example a merger or acquisition. The “anti avoidance” risks and implications have been ignored.

The initial rearrangement (steps 1 to 5) is designed to replace the NZ group’s original equity (which created the tax consequences described in section 7.2) with a more tax effective alternative.

-Step one: The Australian Parent Company subscribes for equity issued by the NZHC. The proceeds from that transaction are ultimately returned to the Australian Parent Company via, for example, a share repurchase of the original equity.

-Step two: The NZHC uses the proceeds from step one to finance the acquisition of a hybrid instrument issued by the NZ Branch of the Australian Finance Company. The transaction is undertaken by the NZ branch to avoid non-resident withholding tax (NRWT) that would otherwise be payable if the transaction was booked with the Australian Finance Company instead of its New Zealand branch. The hybrid instrument will be treated as debt for Australian tax purposes, and as equity for New Zealand tax purposes. Despite the recent Australian changes to the debt/equity boundaries it is still possible to create tax efficient hybrid instruments, which contain all of the tax attributes and advantages of for example the pre July 2001 “Section FC 1 Debentures”. The tax advantages associated with the hybrid instrument arise from the period cash flows described below and summarised in Table 6.

-Step three: The New Zealand branch of Australian Finance Company leads the proceeds (raised from issuing the hybrid instrument to NZHC) to the NZOC. For New Zealand tax purposes this is a transaction between two resident entities and therefore the non-resident withholding tax provisions are not applicable.

-Step four: The NZOC uses the loan finance to repay the original loan shown as step 2 in Diagram 6. From the NZOC perspective it has simply replaced its current creditor (NZHC) with a new creditor (the New Zealand branch of Australian Finance Company), which means that everything else been equal the new arrangement will have no impact on its current business activities.

-Step five: NZHC will use the loan repayment (from NZOC) to return the original equity obtained from the Australian Parent Company. One tax effective method of unwinding the original transaction would be for NZHC to repurchase the original shares from Australian Parent Company. Provided all the technical requirements contained in section CF 3(1)(b) of the ITA94 are satisfied, this transaction will not constitute a dividend and no NRWT would be payable.

Diagram Seven: Hybrid instruments

The New Zealand tax consequences associated with step 1-5 described in section 7.3 above are designed to reduce the current level of New Zealand company tax from $33.00 to zero. The only tax payable will be $10 Australian NRWT. Everything else has been equal; the Australian Parent Company will receive a dividend of $90 from the NZHC. This represents an increase of $23 or a 34% increase in the Australian Parent Company’s after tax return from its investment in the NZHC. The Australian Parent Company invest the additional $23 in a manner that will increase the franking credits, which can be distributed to, inter alia, its Australian shareholders.

(1) Periodic cash flow (a). NZOC plays interest to the New Zealand branch of Australian Finance Company. The interest is deductible to NZOC, and forms part of the New Zealand branch’s gross income. In other words, this transaction is tax neutral from a New Zealand perspective. Secondly, there are no NRWT implications because this transaction is between two New Zealand tax residents.

Table Six: The tax saving associated with a hybrid instrument

|

(a)

|

Interest NZOC to Aus Finance Co (NZ Branch)

|

|

100

|

|

|

- No liability to deduct NZ NRWT

|

-

|

|

|

|

- NET CASH PAID

|

|

100

|

|

|

|

|

|

|

(b)

|

Hybrid Aus Finance Co (NZ Branch) to NZHC

|

100

|

|

|

|

- Aust NRWT – interest

|

(10)

|

|

|

|

NET CASH

|

|

90

|

|

|

|

|

|

|

(c)

|

FDWP Relief s NG 7 (Hybrid)

|

|

|

|

|

- Net cash

|

90

|

|

|

|

- add Aust NRWT

|

10

|

|

|

|

- Gross dividend

|

100

|

|

|

|

- Foreign Dividend Withholding Payment (FDWP) 33%

|

33

|

|

|

|

Less Aust NRWT

|

(10)

|

|

|

|

Less Underlying Foreign Tax Credit (UFTC)

|

(Nil)

|

|

|

|

Net FDWP

|

23

|

|

|

|

S NH 7(1) Conduit Tax Relief (CTR)

|

(23)

|

|

|

|

NET FDWP

|

(Nil)

|

|

|

|

NET CASH RECEIVED

|

|

90

|

|

|

|

|

|

|

(d)

|

Dividend NZHC to Aus Parent Co

|

|

|

|

|

- Cash

|

90

|

|

|

|

FDWP credits

|

Nil

|

|

|

|

Section LGI conduit tax relief dividend

|

23

|

|

|

|

Gross dividend

|

123

|

|

|

|

NRWT 15%

|

*NIL

|

|

|

|

Net cash paid

|

|

* Sufficient imputation credits would be attached to the gross dividend of $123 to eliminate the amount of NRWT which would otherwise be payable, i.e. $61 of imputation credits will ensure a fully imputed dividend.

(2) Periodic cash flow (b)/(c). Australian Finance Company pays interest/dividend to the NZHC pursuant to the terms and conditions of the hybrid instrument. For Australian tax purposes, the transaction constitutes interest and therefore Australian NRWT (at 10%) is payable to the Australian Tax Office (ATO). This is the only tax leakage associated with all of the transactions. For New Zealand tax purposes, the payment is re-characterised as a dividend. In view of the subsequent payment by NZHC of a dividend to the Australian Parent Company the conduit tax relief (CTR) provisions apply. This is the key feature of the entire transaction which eliminates all of the New Zealand company tax and New Zealand NRWT associated with the original “plain vanilla” financing. However, it would be fair to say that the CTR provisions contained in the ITA94 were never meant to be used in this way.

(3) Periodic cash flow (d). The final transaction is the payment of a dividend by NZHC to Australian Parent Company. This transaction is linked to the periodic cash flow (b) / (c) because it is the second stage of the CTR. The original purpose of the CTR provisions were to reduce the amount of New Zealand company tax, and NRWT which is payable associated with International Paper (Inc)’s investment in Carter Holt Harvey Limited who in turn owned forestry investments in Chile and Canada. However, there is nothing in the CTR regime, which prevents the relief from New Zealand tax applying to trans-Tasman companies.

Table Six summarises the New Zealand tax consequences of the periodic cash flows described above in section 7.4. The main purpose of Table 6 is to demonstrate that the original after tax dividend of $67 (paid by NZHC to Australian Parent Company) has increased to $90, as discussed in section 7.4. This represents an increase of $23 or 34% in the after New Zealand tax return of the Australian Parent Company. This only occurs because the CTR regime effectively enables the New Zealand group to more efficiently utilise the underlying New Zealand company tax (imputation credits) paid by the NZOC associated with the commercial activities that were originally financed by the Australian Parent Company.

Prior to the enactment of the PRA solution there were no logical reasons why the hypothetical trans-Tasman group of companies outlined in the Discussion Document (and reproduced as Diagram One) would wish to pay New Zealand company tax. All of the imputation credits created by the New Zealand subsidiary were wasted because they could not be utilised by the any of the shareholders.

What then are the key behavioural implications of the recently enacted PRA solution? The answer depends on the interaction of two variables:

The profile of trans-Tasman companies outlined in Table Two suggest that the PRA solution will provide the New Zealand individual shareholder with a modest increase in their after tax dividend income. The dilution effect means that most of the New Zealand imputation credits will still continue to be wasted because they will be allocated to the Australian shareholders who cannot offset them against their Australian tax liability.

Accordingly, the PRA solution is unlikely to have a significant impact on the current range of trans-Tasman tax strategies utilised by the major trans-Tasman public companies. The PRA solution is likely to encourage the development of Westpac/ANZ ad hoc solutions, which in substance provide the same taxation benefits as the full streaming alternative.

Alternatively, Australian public companies may simply ignore the PRA solution to the detriment of their New Zealand shareholders.

[*] School of Accounting and Commercial Law, Victoria University of Wellington, New Zealand, david.dunbar@vuw.ac.nz

[1] http://www.taxpolicy.ird.govt.nz/news/archive. php year = 2003 at p, 2

[2] Refer to sections: ME 4, (1B), (1C), (2B),ME 5 (IA), (2A) for the relevant credits and debits to the Imputation Credit Account (ICA), section ME 1C for foreign currency conversion issues, sections FDA 1 – FDA 6 for grouping of company procedures, and sections ME 10 (1D) and (1C) for the rules governing trans-Tasman imputation groups.

[3] “Trans-Tasman triangular tax: An Australian and New Zealand government Discussion Document”, p 4, available at either: ATO-Triangular@ato.gov.au, or webmaster@ird.govt.nz.

[5] Op cit, footnote 2 p. 19.

[6] From 57.3% to 43.6%.

[7] Rob Hosking, “Tax specialists pour scorn on tax deal”, National Business Review, February 21, 2003 p. 5.

[8] Please refer to graphs:4,5, and 6, and the discussion which illustrates this principle based on different levels of distribution. Graph 4 plots the effective tax rates associated with a 50% distribution policy. Graph 5 plots the impact of a 75% distribution policy and graph 6 illustrates the effective tax rates associated with a 100% distribution policy. I concede that there are commercial and cash flow reasons why a company is unlikely to implement these levels of distribution.

[9] Shareholding statistics taken from Westpac Australia Concise Annual Report 2002. Income statistics taken from Westpac Financial Report 2002, Note 29, p. 114. Both documents are available online at http://www.westpac.gov.au.

[10] A surprising aspect of this table is that there is NO reduction in the effective tax rate for the Australian shareholders. This could be one of the reasons why no Australian public companies have implemented the PRA solution. A more detailed discussion and analysis of the reasons for this apparently unusual tax outcome is illustrated in graphs 2, & 3, and the accompanying discussion.

[11] See note 2 above at p 15 ( para.3.20), and p16 (para. 3.26 & 3.28).

[12] The Discussion Document contains a brief analysis of the pro rata allocation, streaming and apportionment options at p 14 – 17.

[13] Op cite, footnote 2 para 3.42 p.15.

[14] Ibid p16 para 3.27

[15] Graphs 5 and 6, respectively.

[16] See n 2, at P. 16, para 3.27

[17] Subject to the maximum imputation ratio.

[18] Pages 16-17, paragraphs 3.25-3.27.

[19] p.10, paragraph 3.25.

[20] p. 16, paragraph 3.26.

[21]P: 16,paragraph 3.27.

[22] The Report of the Consultative Committee on Full Imputation noted that from an imputation perspective there were no policy reasons to prevent the allocation of credits to NZ resident shareholders:

“Where a New Zealand company has an overseas corporate shareholder and New Zealand shareholders hold shares in that overseas company, the New Zealand shareholders would not be able to receive credits for New Zealand taxes paid by the New Zealand subsidiary. Some submissions argued that a non-resident company in these circumstances should be able to pass such credits through to its New Zealand shareholders”

[23]See n 14, pp 53-54.

[24] Report of the Consultative Committee on Full Imputation, (April 1988 at p. 53.

[25] BR Prd 99/13, Tax Information Bulletin, Vol 11:10 (November 1999) p. 7. This ruling was replaced with BR Prd 02/14, Tax Information Bulletin Vol 14:11 (November 2002) at p. 5.

AustLII:

Copyright Policy

|

Disclaimers

|

Privacy Policy

|

Feedback

URL: http://www.austlii.edu.au/au/journals/eJlTaxR/2005/9.html