Commonwealth Consolidated Acts Commonwealth Consolidated Acts

Commonwealth Consolidated Acts Commonwealth Consolidated Acts(1) There are these consequences (in most cases) if you can obtain a roll - over when your ownership of a * CGT asset (the original asset ) ends and you * acquire one or more CGT assets (the new assets ) in a situation covered by this Division.

(1A) A * car, motor cycle or similar vehicle must not be one of the new assets.

(2) A * capital gain or a * capital loss you make from the original asset is disregarded.

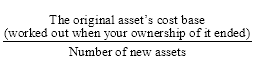

(3) If you * acquired the original asset on or after 20 September 1985, the first element of each new asset's * cost base is:

The first element of each new asset's * reduced cost base is worked out similarly.

Note 1: In some cases the amount you paid to acquire the new asset also forms part of the first element: see Subdivision 124 - D (about strata title conversion).

Note 2: There are modifications to the consequences in Subdivision 124 - B (about compulsory acquisition, loss or destruction), Subdivision 124 - C (about statutory licences), Subdivision 124 - J (about Crown leases) and Subdivision 124 - L (about prospecting and mining).

Note 3: No other elements of the cost base of the new asset are affected by the roll - over.

Note 4: There are special indexation rules for roll - overs: see Division 114.

Note 5: The reduced cost base may be modified for a roll - over happening after a demerger: see section 125 - 170.

(4) If you * acquired the original asset before 20 September 1985, you are taken to have acquired each new asset before that day.

Note: A capital gain or loss you make from a CGT asset you acquired before 20 September 1985 is generally disregarded: see Division 104. This exemption is removed in some situations: see Division 149.

(5) However, subsection (4) is taken never to have applied to a * share to which subsection 104 - 195(6) applies (CGT event J4).